VusionGroup (VU.PA) — FY 2025 Earnings

Hardware planted the seeds. The software harvest has begun.

0. THE SCOREBOARD

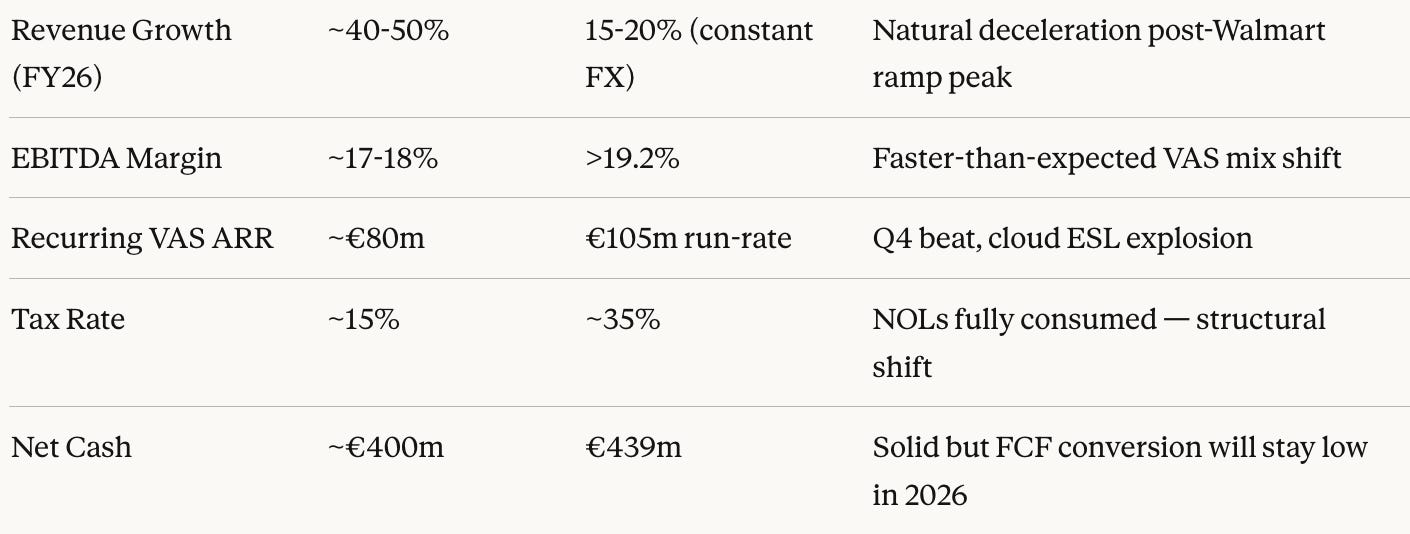

Vusion delivered a genuine blowout year: adjusted revenue of €1,527m smashed through its own €1.5bn target (+51% YoY), EBITDA of €277m grew +73% with margin expanding 230bps to 18.2%, and net income nearly doubled to €99m adjusted. For 2026, management guided 15-20% revenue growth at constant FX/tariffs with another 100bps+ of EBITDA margin expansion solid but a meaningful step-down from the hyper growth of 2025. Gut read: exceptional year that confirms and accelerates the thesis, with the 2026 guidance reset being the only thing bears can point to.

1. THE THESIS CHECK

A. The Original Thesis I published in 2024 Vusion is the picks-and-shovels play on physical retail digitalization. The three pillars:

(1) ESL hardware creates a massive sticky installed base that unlocks a high-margin software/services layer over time,

(2) the Walmart deal proves the model at scale and becomes the reference case that pulls in every other global retailer, and

(3) the shift from one-time hardware revenue to recurring VAS (Value-Added Services) SaaS fundamentally re-rates the business.

B. Green Lights 🟢

VAS revenue doubled in a single year to €211m (14% of sales vs. 10% in 2024) this is the most important number in the whole release. The software flywheel is spinning. Recurring VAS specifically hit €83m (+45%) with an annualized Q4 run-rate of €105m. The company crossed the €100m ARR threshold in Q4 a psychological milestone that signals a real SaaS business is forming inside what was once a hardware company.

Cloud IoT installed base exploded from 152m to 375m ESLs (+147%) this is the future revenue engine. Every connected ESL is a subscription opportunity, a data point, and a barrier to switching. Doubling the installed base in one year is extraordinary.

The Walmart proof point is now undeniable. Americas & APAC revenue grew +115% to €1.1bn. Walmart’s own earnings cited store-fulfilled delivery growing 50%+ exactly the use case that EdgeSense enables. The reference customer is thriving, which makes every sales conversation globally easier.

Margin expansion is structural, not cyclical. EBITDA margin of 18.2% (+230bps) was driven by three simultaneous forces: R&D investment lowering hardware costs, scale economies in manufacturing, and the VAS mix improvement. Operating leverage is kicking in opex grew 43% while revenue grew 51%.

The Carrefour deal (announced February 18, 2026, just before this release) is the first major European full-platform deployment covering EdgeSense + VusionCloud + Captana simultaneously. This is the blueprint for what Walmart demonstrated in the US, now replicated in Europe’s second-largest retailer. The bull case is replicating the Walmart playbook across the global retail base.

C. Yellow Flags 🟡

Free Cash Flow of €56m looks weak relative to €277m of EBITDA. The FCF/EBITDA conversion is just 20%. Management correctly explains this is due to the unwinding of Walmart downpayments and the final investment in manufacturing lines both known and flagged. But in 2026 this headwind continues (”consumption of downpayments will continue in 2026”), so FCF will again lag EBITDA significantly. Worth tracking closely.

EMEA revenue fell -16% to €415m (and -25% in Q4 specifically). Management frames this as a planned completion of a major European customer rollout. The Carrefour deal and growing European order intake support a 2026 EMEA recovery, but until the numbers actually turn positive, this remains a watch item.

Order intake growth slowed to just +5% (€1.7bn vs. €1.6bn in 2024). After +71% growth in 2024, this deceleration deserves attention. Management argues existing customer VAS expansion is not fully reflected in order metrics, and European intake is growing but a 5% order book growth feeding 15-20% revenue growth guidance implies significant revenue recognition from existing backlog.

The 2026 guidance is framed “at constant exchange rates and tariffs” a caveat management had to add explicitly given EUR/USD volatility. The USD weakened against EUR during 2025, costing €53m of revenue on a constant-FX basis. The tariff language is new and directly references the risk that US tariff policy could affect their Vietnam/Mexico manufacturing footprint.

D. Red Flags 🔴

Customer concentration is the elephant in the room. Americas & APAC was 73% of 2025 revenue, driven overwhelmingly by Walmart. The press release explicitly states Walmart’s production lines in Vietnam and Mexico “are all operational.” Any disruption to Walmart’s rollout appetite, or tariff-driven cost pressures on that supply chain, is an outsized risk with no near-term diversification buffer large enough to compensate. The documents do not disclose what % of revenue Walmart specifically represents worth pressing on the next call.

The tax line is a new and permanent headwind. The Group “had utilized all of its tax loss carry forwards” at end 2024, meaning the full €53.4m tax expense in 2025 is now structural. In 2024 the tax line was just €2.2m on IFRS and €10m adjusted. This is a 5x increase in the tax burden that will persist the EPS growth rate going forward will be materially lower than EBITDA growth rate absent margin expansion to compensate.

Non-recurring/non-cash charges grew +22% to €29m, mostly IFRS2 stock comp (€31m). As the company scales headcount and grants more performance shares, this line will grow. It’s below the EBITDA line but it is real dilution.

E. Thesis Verdict: ⚡ Thesis Strengthening

The VAS flywheel, the Walmart proof point, and the Carrefour announcement together represent a step-change in the quality of the business not just the size. The ARR crossing €100m, the cloud installed base nearly tripling, and the first pan-European full-platform win are all things that make the 3-5 year bull case more compelling than it was 12 months ago. The growth deceleration to 15-20% for 2026 is the natural consequence of an enormous 2025 base and should not be confused with a thesis crack.

2. THE NUMBERS THAT MATTER

A. P&L Highlights (Adjusted basis)

Revenue: €1,527m (+51% YoY). H2 was stronger than H1 (€877m vs €649m), driven by Q4 of €522m (+46% YoY) the biggest quarter in company history.

Variable Cost Margin: €472m, 30.9% of revenue (+160bps YoY). This is the gross profit proxy the business is generating more per euro of hardware shipped as VAS mix improves and manufacturing costs fall.

EBITDA: €277m, 18.2% margin (+230bps). Grew at 73%, far outpacing 51% revenue growth operating leverage is real.

EBIT: €164m adjusted, 10.7% margin (+290bps). D&A jumped +47% to €84m due to Walmart-related production line amortization and EdgeSense development capitalization this drag continues.

Net Income: €99m adjusted (+85% YoY), €84m IFRS (vs. -€29m loss in 2024 on IFRS basis a complete turnaround).

B. The Cash Machine Check

Operating Free Cash Flow: €212m (+84% YoY) this is the right metric to watch. It’s calculated before working capital swings and before customer-financed capex, and it grew at essentially the same pace as EBITDA. Clean signal.

Free Cash Flow (reported): €56m (vs. €391m in 2024). The collapse is entirely explained: (1) -€25.7m working capital swing as Walmart downpayments are consumed (was +€397m last year), and (2) €53m in taxes (was €5m). Both were flagged. FCF/EBITDA conversion: ~20% low, but deliberately so and expected to improve as the Walmart downpayment drag diminishes post-2026.

FCF vs. Net Income: FCF (€56m) < Net Income (€84m IFRS / €99m adjusted). This is worth watching but is entirely explained by the working capital normalization and tax ramp, not by earnings quality issues.

C. Business-Specific KPIs

Recurring VAS ARR: €105m (annualized Q4 run-rate), up from effectively ~€57m annualized at end 2024. This is the SaaS metric that will drive valuation re-rating over time.

Cloud ESL Installed Base: 375m (+147% YoY from 152m). Each connected ESL represents a subscription opportunity. This is the moat metric.

VAS as % of Revenue: 14% (vs. 10% in 2024). The direction of travel is clear; the target trajectory toward 20%+ defines the medium-term margin story.

Order Intake: €1.703bn (+5%). Healthy absolute level but decelerating growth needs watching.

D. Balance Sheet

Net Cash: €439m (up €46m from €393m). The company is debt-light with €42m of debt vs. €481m of cash + financial assets. No leverage concern whatsoever. This balance sheet is the M&A optionality and the moat vs. smaller competitors.

Upcoming share buyback of €30m announced signaling management confidence but modest relative to the balance sheet.

E. Shareholder Returns

Dividend: €0.90 proposed (vs. €0.60 in 2024, vs. €0.30 in 2023) third consecutive growth at +50%. Still tiny in absolute terms (~€30m total payout), consistent with a growth company prioritizing reinvestment. Share buyback of €30m imminent. Total capital return ~€60m modest relative to the €439m net cash position.

3. MANAGEMENT SAYS vs. REALITY

A. Guidance Breakdown

2026 Revenue: +15% to +20% at constant FX/tariffs. On the 2025 adjusted base of €1,527m, this implies €1,756m-€1,832m. At spot EUR/USD rates (the EUR strengthened in 2025), actual reported euros could be materially lower this is not a small caveat.

VAS: ~40% growth (implying ~€295m, with recurring component accelerating toward €120m+ ARR).

EBITDA Margin: >100bps improvement, implying >19.2% adjusted continued but more modest expansion.

The translation: this is honest guidance. They’re not sandbagging dramatically, but they’re also not promising a repeat of 51% growth. The “at constant FX and tariffs” qualifier is load-bearing if EUR/USD stays around 1.08, there’s a ~3-4% reported revenue headwind baked in that the guidance excludes.

B. The Language Audit

CEO Gadou: “The transformation of retail is entering a new era that will place physical stores at the heart of the omnichannel strategies of retailers, as demonstrated by Walmart’s extraordinary success.” → Translation: We are riding Walmart’s coattails smartly and making it our reference case for every new conversation globally. The framing of Walmart’s success as validating Vusion’s platform rather than creating a dependency risk is deliberate and worth scrutinizing.

On EMEA: “a business climate less favorable than expected in the second half of 2025” this is management finally admitting the H2 EMEA miss was not entirely planned. They soften it quickly by pointing to strong European order intake in H2, but the word “unexpected” slipping in there is notable.

On 2026: “maintaining a very strong balance sheet and a surplus net cash position at year-end (excluding acquisitions)” the parenthetical is doing a lot of work. They are explicitly telegraphing that M&A is on the agenda and that they want optionality. Given the Ubica Robotics stake (11.9% minority in a robotics company for €7m) and the Yagora data analytics acquisition, a larger deal in AI/robotics/computer vision is on the roadmap.

C. The Question They Dodged

The question nobody asked (or got a straight answer to) that matters most: what is Walmart specifically as a percentage of 2025 revenue, and what is the contractual commitment for 2026 and beyond? The company discloses that Walmart must reach $3 billion in cumulative spending to trigger full warrant amortization, but nowhere does it say where Walmart is today on that $3bn journey. Given that Americas/APAC revenue was €1.1bn in 2025 (~$1.1bn+), Walmart must represent the majority of that. The lack of explicit Walmart revenue disclosure is the single biggest information gap. Worth pressing at Q1 2026.

D. Management Credibility Score: 🟢 Delivered

They guided “around €1.5bn” in adjusted revenue and hit €1,527m. EBITDA margin guidance was for improvement; delivered +230bps. They flagged the FCF decline in advance. Every major commitment was met or exceeded. This management team has now delivered against guidance multiple times in a row on a volatile, hypergrowth trajectory. Credit where it’s due.

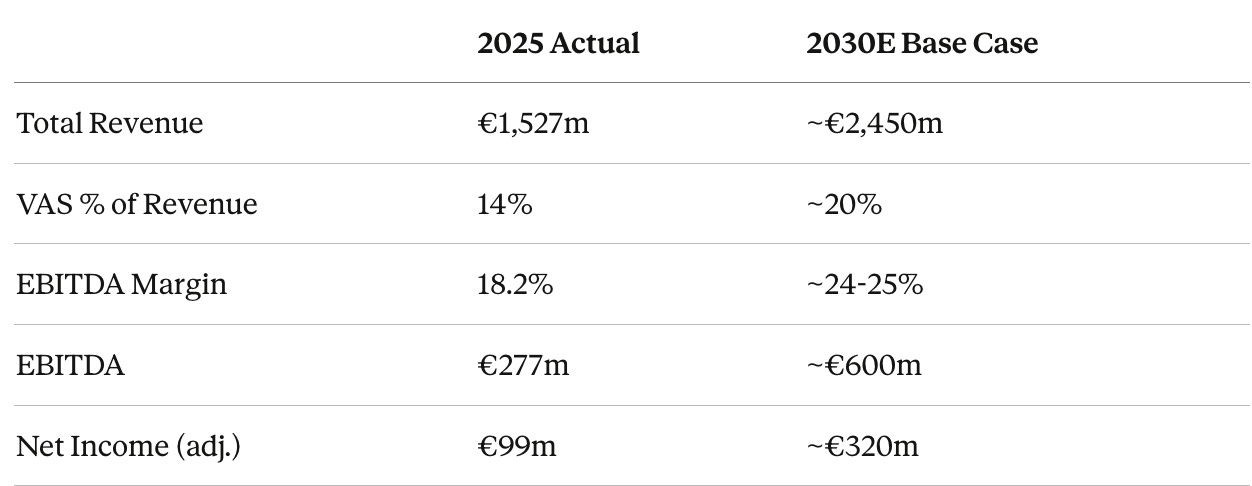

4. THE NAPKIN MATH UPDATE

A. What Changed in the Model (2025 vs 2026 guidance)

B. Revised Return Estimate

The 15-20% top-line growth guidance for 2026, combined with >100bps margin expansion and the Carrefour/DM/European pipeline, suggests the earnings growth rate is structurally in the 20-30% range for the next 3-5 years — driven by VAS mix improvement even as hardware growth moderates. The tax normalization is a one-time step-down in EPS growth that is now fully absorbed. The 5-year bull case still looks like 20%+ annualized EPS growth, which at a reasonable growth premium multiple implies meaningful upside from here.

C. The Valuation Reality Check

Specific P/E and forward multiples are not calculable without the current share price, which is not disclosed in the provided documents. What is clear: the business just re-rated qualitatively. A company with €105m ARR growing 45%+, 375m cloud-connected devices, net cash of €439m, and Walmart + Carrefour as anchors is structurally a different business than the hardware ESL company from 3 years ago. Any valuation using pure hardware multiples is now wrong.

4B. THE ESL INSTALLED BASE MODEL : BOTTOM-UP REVENUE SIMULATION

This section attempts to quantify what the installed base trajectory means for recurring VAS revenue, independently of any pricing expansion assumptions. All figures at constant €0.22/ESL/year, the current realized rate.

The Cross-Check That Validates the Model

Before projecting forward, the calibration: Vusion reported €83m of recurring VAS ARR at end-2025 on 375m cloud-connected ESLs. That’s €0.221/ESL/year. Our model anchors on this exact figure. No assumptions, just current reality extrapolated.

The TAM: How Many ESLs Exist in the World?

The global addressable universe for ESLs is large format retail: supermarkets, hypermarkets, DIY stores, electronics chains, pharmacy chains. Convenience stores (<500m²) and pure e-commerce are excluded.

A conservative bottom-up estimate across the major global chains:

At current penetration (375m / 2,200m): Vusion has digitized roughly 17% of addressable ESL slots globally and the overwhelming majority of that is Walmart. The ex-Walmart penetration rate is probably below 5%. The runway is enormous.

The Competition Reality Check: Why 60% Market Share Is a Fantasy

The naive extrapolation would project Vusion capturing 50-60% of this TAM. That’s wrong for a simple reason: Hanshow (Chinese, state-backed, aggressive on hardware pricing), Pricer (European incumbent, 30-year track record), and Solum/Samsung (distribution relationships in Asia) are real competitors that will take meaningful share in their home markets. B2B tech leaders with genuine switching costs and 5+ year head starts rarely exceed 25-35% of a global TAM when facing credible competition, see Samsara in fleet IoT (~18% after 8 years), ServiceNow in ITSM (~30% after 15 years).

The bear case assumes Hanshow wins Asia, Pricer defends Europe’s mid-market, and Vusion lands at ~12% global share. The base case assumes Vusion’s software ecosystem which Hanshow cannot replicate quickly drives a 25% global share outcome. The bull case gets to 35% if Retail Media (Engage) becomes a genuine network effect moat that competitors can’t match.

The Revenue Simulation Base Case (25% TAM, €0.22/ESL/year constant)

CAGR of recurring VAS revenue (2025→2030): ~32% at flat pricing.

The installed base at 1.5bn ESLs in 2030 represents ~25% of the global TAM. That’s the base case. The bear case (12% TAM = 264m ESLs) generates ~€58m ARR — roughly where Vusion is today. The bull case (35% TAM = 770m additional ESLs from today) generates €465m ARR by 2030.

The Pricing Optionality Nobody Is Modeling

The €0.22/ESL/year figure is the floor, not the ceiling. Every comparable IoT subscription business has demonstrated pricing power as the software layer matures:

Samsara (fleet IoT): started at ~$15/vehicle/month, now averages $25-30 as AI features were added

Axon Evidence (bodycam cloud): started as almost free, now the core profit driver at ~$80/officer/year

Veeva Vault: CRM entry price becomes €10x revenue per seat once the full platform is deployed

Vusion’s equivalent trajectory: €0.22 today → €0.50 by 2028 as EdgeSense analytics, Captana AI, and Retail Media attribution become table stakes that retailers pay for explicitly. At €0.50/ESL/year on 1.1bn ESLs (2028E installed base), recurring VAS ARR alone is €550m without adding a single new store.

This is the number the market isn’t pricing. At all.

The 2030 Valuation Implied by This Model

Taking the base case numbers through to a full P&L:

At 20x EBITDA (appropriate for a business with ~20% software mix, growing 12-15% topline, margins expanding): EV of €12bn, or ~€717/share.

At 30x P/E on €320m net income: €9.6bn market cap, or ~€574/share.

The range of €574-717/share from today’s ~€120 implies a CAGR of ~35-42% for the equity holder over 5 years, not because of multiple expansion alone, but because of the mechanical compounding of installed base growth × margin expansion × gradual pricing normalization.

The downside scenario (Hanshow wins, Walmart slows, no pricing power): hardware alone is worth €80-90/share. The asymmetry is real.

5. MY PROPRIETARY INSIGHT

The Hidden Trend Nobody’s Talking About: The Non-Recurring VAS Mix Is Masking the True SaaS Story

Everyone is focused on the headline VAS doubling. But the more interesting signal is inside VAS. Non-recurring VAS grew +166% to €128m in 2025, while recurring VAS grew “only” +45% to €83m. On the surface, this looks like a software company still selling mostly one-time services.

Here’s what that actually means: the non-recurring VAS (installation services, Captana cameras, Retail Media hardware) is the seed. Every camera, every Engage screen, every installation contract planted in 2025 becomes a subscription in 2026 and 2027. The non-recurring VAS line is the leading indicator for future recurring VAS. In 2024, recurring was €57m and non-recurring was €48m (roughly 1:1 ratio). In 2025, non-recurring surged to €128m while recurring caught up to €83m. The implied future recurring contribution from the 2025 non-recurring pipeline, if it converts at even a 30% annual subscription attach rate, is €35-40m of incremental ARR per year layered on top of the existing base. Vusion’s ARR at end of 2026 could plausibly be €140-160m, a number the market isn’t pricing because everyone’s looking at the reported €83m figure.

The 150,000 AI cameras to be deployed in 2026 (from a “significant enhancement” of Captana) are the most important number in the outlook section. Each camera is recurring revenue. Watch the Captana installation pace in Q1 2026 data, it will tell you everything about the 2027 ARR trajectory.

The Setup for Q1 2026: The single metric to watch when Q1 2026 sales are released on April 21 is the EMEA revenue trajectory. If EMEA returns to growth (which order intake supports), it will confirm the geographic diversification thesis and reduce the binary Walmart concentration risk. If EMEA is still declining, the 15-20% group growth target gets a lot harder with Americas/APAC carrying the whole load.

6. MY TAKE

A. Sleep Score: 8/10

The ARR crossing €100m, the Carrefour deal, and the demonstrated operating leverage all add a meaningful level of confidence. The Walmart concentration and the FCF conversion lag are the two things keeping it from a 9.

B. The Bull Case (Updated)

The Walmart-to-Carrefour playbook is now proven repeatable, one year after Walmart, Europe’s second-largest retailer signs a full-platform deal. The pipeline of 350+ retail groups globally, combined with a cloud installed base that tripled in one year, creates a compounding dynamic: more ESLs → more cloud subscriptions → more data → better AI products → more premium pricing → higher margins. The €105m ARR is just the beginning of a business that could be doing €400-500m ARR by 2028. Additionally, Retail Media (the “Engage” product) just signed its first contracts, this is the highest-margin, most scalable revenue line in the company’s history if it lands.

C. The Bear Case (Updated)

Walmart represents an uncomfortable majority of current revenue from an unknown but almost certainly dominant position. Any slowdown in Walmart’s store digitalization program whether from tariffs affecting Vietnam/Mexico manufacturing, capital allocation shifts at Walmart, or completion of the core rollout, would create a massive revenue air pocket. The 2026 guidance “at constant FX and tariffs” is a window into management’s own anxiety about these risks. Additionally, the D&A line (+47% in 2025) is growing faster than most people model, and as EdgeSense development costs continue to amortize, this will be a persistent drag between EBITDA and actual net income.

D. The One-Liner

The machine just delivered a year that would make most tech CEOs cry with envy and then management had the discipline to guide conservatively rather than promise another 51%. That’s a feature, not a bug.