This Company's Entire Business Model Is Built Around Borrowers Who Can't Repay No, it's not a scam.

Propel Holdings Knows 50% of Its Borrowers Won't Pay Back. That's the Whole Plan. Here's why a business built on defaults might be the most rational trade on the TSX right now

0. THE STORY

Propel Holdings was born from a simple, uncomfortable truth: roughly 40% of Americans can’t get a loan from a bank. Not because they’re deadbeats but because a decades-old algorithm called FICO was never designed with them in mind. The typical Propel customer is an older millennial or younger Gen X, aged 35 to 54, with average credit limits between $2,000 and $3,000. These are nurses, warehouse workers, gig drivers people with jobs and income, invisible to the traditional financial system. Propel’s pitch: let AI figure out what FICO can’t.

The current drama is juicy. Q4 2025 net income dropped 49% year-over-year to $5.9 million, spooking the market. PRL stock fell roughly 42% from its six-month highs. But here’s the twist: the full year was a record revenue increased 31% to $589.8 million for fiscal 2025. The Q4 hit was mostly accounting timing: you provision for loan losses upfront (hit to earnings now), but collect the revenue over the life of the loan (profit later). It’s like a restaurant being penalized for buying ingredients before serving dinner.

Why analyze Propel right now? Because 8 out of 8 covering analysts rate it a Strong Buy, with an average 12-month price target of CAD $30.16 against a stock sitting near CAD $24. The market is pricing in a permanent deterioration; analysts think it’s temporary noise. One of them is right, and figuring out which one is worth your time.

1. THE MACHINE

The Simple Explanation

Think of Propel like a really smart pawn broker who figured out that the reason most pawn brokers go bust isn’t the customers it’s the bad scoring system. Banks use FICO like a bouncer with a single rule: “no entry if you’ve ever been broke.” Propel built a smarter bouncer. Its AI platform analyzes over 5,000 data points per applicant to get a holistic view of financial health, looking at cash flow patterns, employment stability, and pay-cycle timing rather than ancient credit history. It processes 60,000+ applications per day and delivers decisions in seconds. Then it lends money at high interest rates to borrowers who have few alternatives, and it keeps getting better at predicting who will actually pay back.

The Moat

The moat here is subtle but real it’s a data flywheel. With each loan screened and data inputted, the AI gets stronger. This is the core compounding asset: more loans → more repayment data → sharper models → lower charge-offs → higher profitability → ability to lend more. After 14 years of data accumulation and over $2 billion in credit facilitated, replicating that dataset is genuinely hard for a new entrant.

There are also switching costs on the borrower side Propel has “graduation programs” where good customers move to lower rates and higher limits over time, creating loyalty in a segment that normally has none. And then there’s the licensing moat: Propel received regulatory approval to launch Propel Bank in December 2025, which is not easy to replicate and opens up completely new product categories.

The ROIC Story

This is where it gets interesting for compounders. Annualized adjusted Return on Equity was 27% for the full year 2025, and management is targeting 28%+ adjusted ROE for 2026. That’s excellent it means the business can grow without constantly diluting shareholders. Crucially, the new FreshLine product launched with $210 million in forward-flow commitments from third-party investors, meaning Propel generates fee revenue while the credit risk sits largely off its own balance sheet. This Lending-as-a-Service pivot is the most important structural shift to understand: they’re moving from “lender who takes risk” to “platform that earns fees,” which is a dramatically higher-quality business model.

The Risks

Let’s be direct here because the risks are real and not to be waved away. Credit losses are very high around 50% of the loan book compared to banks’ average of 0.7–1%.That’s not a typo. This is the business model: you charge 100%+ APR on small loans to risky borrowers, and you lose a lot of them, but you win enough to make money. It works in a good economy. In a recession, delinquencies spike and the whole machine can seize up.

Regulatory risk is significant. The CFPB has historically targeted exactly this type of lender high-rate consumer credit to financially vulnerable people. One bad administration decision or a state-level rate cap could eliminate entire revenue streams overnight. And the AI moat, while real, is not impenetrable: low barriers to AI entry mean a well-funded competitor with access to similar data could theoretically catch up. Finally, the macro sensitivity is severe. This is not a business you want to hold through a deep recession.

2. THE NUMBERS

(All figures in USD unless noted; stock price in CAD)

Current Valuation

Price: ~CAD $24.10

Market Cap: ~CAD $950M (~USD $680M)

Enterprise Value: ~USD $960M (adding ~USD $307M debt, subtracting ~USD $28M cash)

Profitability Snapshot (FY2025)

Revenue (TTM): USD $589.8M (+31% YoY) record

Net Income (TTM): USD $59.5M (+28% YoY) record

Adjusted EBITDA: USD $130.3M

Operating Margin: ~20% (on an adjusted basis)

Note: For financial companies, we focus on earnings, not free cash flow

Valuation Metrics

P/E (TTM): ~11.2x

Forward P/E: ~6.3x (based on 2026 guidance)

Historical P/E range: essentially not comparable pre-profitability; since becoming consistently profitable (2022 onward), the stock has traded between ~10x and ~25x earnings

Earnings Yield (TTM): ~9%

vs 10Y US Treasury (~4.4%): Propel offers a +4.6% spread over risk-free

vs S&P 500 Earnings Yield (~4.1%): Propel offers a +4.9% premium substantial

At a forward PE of 6.3x, forward earnings yield is ~16% almost 4x the S&P 500

Shareholder Returns

Dividend yield: ~4.8% (following the 10th consecutive dividend hike, announced February 2026)

Buyback: NCIB announced November 2025 buyback yield estimated ~1-2%

Total Shareholder Yield: ~6–7%

Quality Indicators

Debt/Equity: 117.9% elevated, typical for a lending business

Interest Coverage: 3.5x (EBIT / Interest Expense) adequate but not comfortable

The debt/equity ratio has fallen from 613% to 117.9% over the past 5 years dramatic deleveraging as the business matured

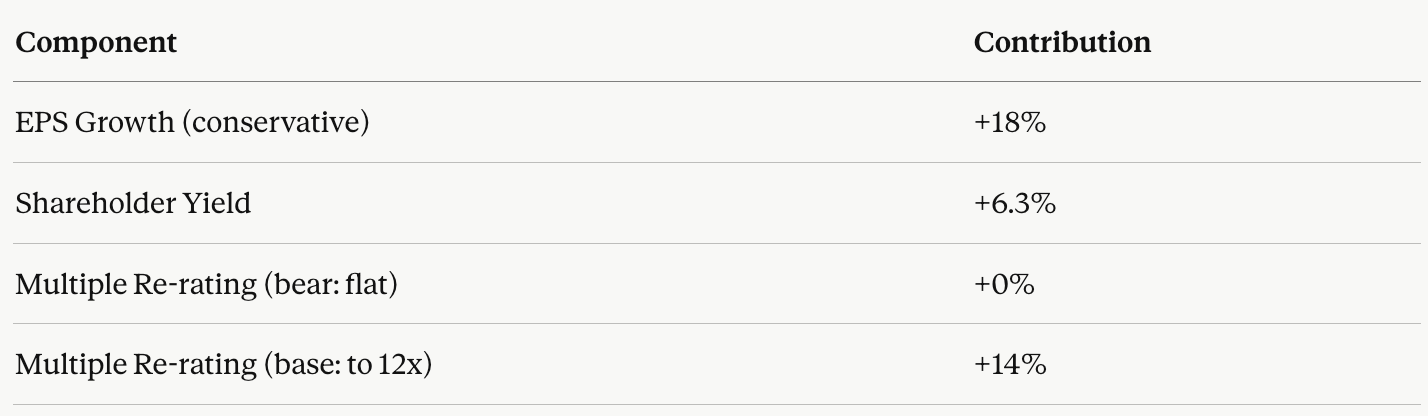

3. THE NAPKIN MATH

A. Growth Driver (EPS Growth)

Management guided for net income of $70–90 million in 2026, representing ~34% growth at the midpoint over 2025. That’s aggressive; let’s be conservative and cut it in half:

Revenue Growth: ~20% annually (vs 31% in 2025, 44% in H1 2025)

Margin slightly expanding as LaaS scales

Minimal share count dilution (NCIB active)

Conservative EPS Growth: ~18% per year

B. Shareholder Yield

Dividend: ~4.8%

Buybacks: ~1.5%

Total: ~6.3%

C. Valuation Drag/Boost

Current forward P/E is ~6.3x. If you assume the market eventually rewards a business growing 18%+ with a more reasonable 12x P/E (still cheap by any standard):

(12/6.3)^(1/5) - 1 = +14% per year tailwind from multiple re-rating alone

If the market stays permanently skeptical and P/E stays at 6.3x: +0% from multiple, but you still get the earnings growth and yield.

D. The Final Equation

Bear Case 5Y Return: ~24% annually Base Case 5Y Return: ~38% annually

Even in the bear case no multiple expansion, economy stays tough the math is hard to ignore. The S&P 500 historically delivers ~10% per year. You’re getting 2–4x that if the business just survives and executes.

4. MY PROPRIETARY INSIGHT

Here’s the thing nobody talks about: Propel is quietly transforming its business model in real time, and the market is still pricing it like the old version.

The old Propel: lend money to risky borrowers, collect high interest, write off the ones who don’t pay, repeat. Capital-intensive, cyclical, scary in downturns.

The new Propel: build an AI-powered credit intelligence platform, let other people’s capital fund the loans, collect platform fees. Management expects Lending-as-a-Service to deliver triple-digit growth and approach 10% of total revenue by Q4 2026. That’s a fundamentally different margin and risk profile and it trades at an entirely different multiple in every comparable fintech.

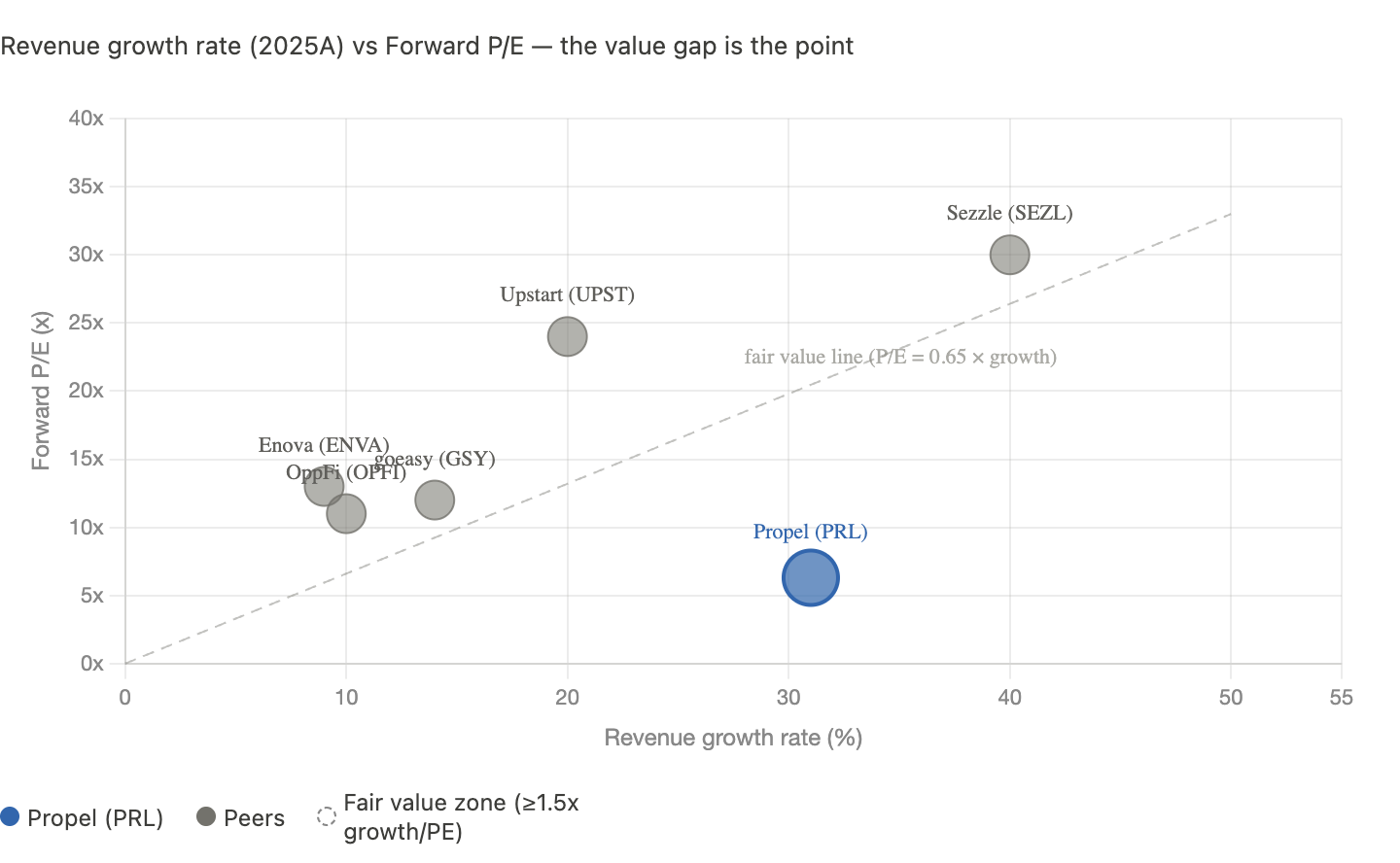

The market is valuing Propel at 6.3x forward earnings. Upstart Holdings which does a similar “AI underwrites loans, bank partners hold them” model has traded at 30–60x. Even discounting for Propel’s smaller scale and Canadian listing, the gap is absurd if the LaaS pivot succeeds.

Here’s my proprietary comparison: when you plot Propel against its nearest comps on the axis that actually matters growth rate vs. valuation multiple the picture becomes embarrassing.

The dashed line is the “fair value” reference a stock growing at 31% would reasonably deserve a P/E somewhere around 20x. Propel is at 6.3x. The entire peer group sits above the line. Propel is the one anomaly sitting far below it.

There’s a historical pattern worth flagging: every time Propel has traded below 10x trailing earnings since becoming profitable in 2022-2023, it has subsequently re-rated significantly higher. We’re currently at ~11x trailing, ~6x forward. The last time forward earnings were this cheap was early 2023, and the stock nearly tripled over the following 14 months before the latest selloff.

The contrarian take the market is missing: the Q4 miss wasn’t a sign of deterioration it was a sign of accelerating growth. You provision now for the loans you originate now. Late-quarter origination growth, particularly in December, required upfront provisioning under IFRS accounting, while the associated revenue will be recognized over future periods. A company that didn’t grow wouldn’t have this problem. The market punished Propel for investing aggressively in its own future.

5. MY TAKE

Sleep Well at Night Score: 5.5/10

This is not a 9/10 sleeper. It’s a high-conviction, higher-volatility situation. The business quality is genuinely improving, but the macro environment adds real uncertainty.

What Excites Me

The LaaS pivot is a hidden re-rating catalyst. If Lending-as-a-Service hits 10% of revenue by year-end and continues scaling, Propel deserves to trade like a software platform, not a subprime lender. That multiple difference alone is worth 100%+ in the stock.

Ten consecutive dividend increases, now yielding nearly 5% on a company still growing revenue at 30%+ that combination is genuinely rare. You’re being paid to wait.

Propel Bank adds a completely new chapter to the story. Regulatory approval to launch Propel Bank came in December 2025, and the long-term implications cheaper cost of funds, deposit products, expanded lending capacity — are not priced in at all at current levels.

What Worries Me

The macro timing is terrible. Tariffs, slowing consumer spending, and potential U.S. recession risk are exactly the conditions that cause near-prime borrowers to miss payments. The concern is that this stock works great in a good economy, but not so much when the economy turns and that turn may already be starting.

Credit loss rates of ~50% of the loan book are a feature, not a bug until they’re not. There’s limited margin for error if charge-offs spike 10-15% above model assumptions.

Institutional participation is thin. Very limited institutional participation means the stock can move violently on small order flow. That cuts both ways it’s why the discount exists, and why volatility can be stomach-churning.

The One-Liner

A rare fintech trading at utility-company multiples while quietly building a platform business the market is looking at last quarter’s loan losses and missing next year’s fee income.