The Stock Everyone Calls "The Costco of Latin America" And Why That's Dangerous

PriceSmart built a monopoly in 12 countries and no one noticed. Now everyone has noticed, and the price shows it.

0. The Story

Most people have never heard of Sol Price. That’s a shame, because he’s arguably the most influential retailer of the 20th century that nobody talks about. Price founded FedMart in 1954, then launched Price Club in 1976 in San Diego and it was from that blueprint that Sam Walton built Sam’s Club, and Jim Sinegal built Costco. Sol Price invented the membership warehouse club as we know it. When Price Club eventually merged with Costco in 1993, the Price family negotiated something remarkable into the deal: they kept the international rights. The non-US markets. The ones everyone considered too small, too risky, too poor to bother with. That turned out to be one of the great unheralded deals in retail history.

PriceSmart was incorporated in 1994 from those international assets, and opened its first club in Panama City in 1996 when the conventional wisdom was that Central America and the Caribbean were too developing, too risky, too fragmented for a warehouse club model. The Price family disagreed. They believed there was a solid, aspirational middle class across these markets that wanted access to quality American brands at fair prices brands they either couldn’t get locally, or could only get at extortionate import markups. They were right. Today, PriceSmart operates 56 warehouse clubs across 12 countries and one U.S. territory, generates $5.27 billion in annual revenue, and has over two million membership accounts representing almost four million cardholders.

Here’s the current drama: after years of being the quiet compounder nobody watched, PSMT has had a violent re-rating. The stock recently traded near all-time highs, with the multiple expanding well above its historical average, driven by renewed investor excitement around the Chile expansion and accelerating membership metrics. But the January 2026 earnings call introduced a note of caution the stock sold off on a marginal EPS miss versus stretched consensus, even though the underlying business delivered 9.9% revenue growth. The market now has a very specific question to answer: has PriceSmart structurally become a better, faster-growing business or has it simply become an expensive version of a good one? That’s what we’re here to figure out.

1. The Machine

Here’s the genius of the warehouse club model, explained in one paragraph: you charge people money just to walk in the door. That upfront membership fee $45 for a standard card, $90 for Platinum covers a massive chunk of your operating costs before a single product is sold. So when you sell merchandise, you can price it at wafer-thin margins and still run a profitable business. The merchandise basically sells at cost. The profit comes from the membership. This is why PriceSmart’s membership fees, which are only 1.7% of net merchandise sales, account for a stunning 36.8% of total operating income. Read that again. A tiny line on the income statement provides more than a third of the company’s entire profit. That’s not a quirk it’s the whole architecture of the business.

What makes PriceSmart’s version of this model interesting is the context in which it operates. In the US, if you’re a Costco member and you’re unhappy, you can go to Sam’s Club or BJ’s. In Panama City, in Kingston Jamaica, in San José Costa Rica PriceSmart is the only game in town. There is no warehouse club alternative. That monopoly-by-default status changes the pricing power and renewal rate dynamics significantly.

The Moat: Deeper Than It Looks

The first-mover advantage is real but it’s also the most obvious part of the story. Let me dig one level deeper.

PriceSmart’s clubs are typically between 30,000 and 75,000 square feet and stock approximately 2,500 items. That sounds small. Costco warehouses run 147,000 square feet with ~3,700 SKUs. But here’s the insight that most people miss: PriceSmart’s sales per item per week per location are $671 higher than Sam’s Club at $550, BJ’s at $225, and Cost-U-Less at $169.They’re doing more volume per SKU than almost any comparable retailer, in a smaller building, in a developing market. The model is insanely capital-efficient on a per-product basis because the SKU discipline is extreme. When you only carry 2,500 products, every single one of them has to earn its shelf space. The buyer has incredible leverage with suppliers, similar to how Costco’s buyers manage fewer than 200 SKUs each which means they know the cost structure of every product better than the suppliers themselves.

The switching cost angle is also underappreciated. The Platinum membership, now at $90/year with a 2% cashback on most purchases, is explicitly designed to lock in the highest-value members through financial incentives and it’s working. Platinum membership accounts jumped from 12.3% to 17.9% of the total base in a single year. The 2% cashback creates a feedback loop: the more you spend at PriceSmart, the more your membership is worth, the less rational it is to cancel. It’s the same psychology that makes Amazon Prime subscribers spend so much more than non Prime members you’ve already paid the fee, so you want to extract maximum value from it.

Then there’s the private label angle, which is where things get really interesting from a structural perspective. Private label sold under the Member’s Selection® brand now represents 28.1% of total merchandise sales. To put this in context: Kirkland Signature, Costco’s legendary private label, also accounts for about 28% of total sales. PriceSmart is at Kirkland-level private label penetration — with a fraction of the resources, in markets where local consumers are arguably even more price-sensitive and brand-conscious. Private label products carry structurally higher margins than national brands. This isn’t a trivial observation: it means every percentage point of private label penetration that PriceSmart adds is a quiet margin expansion that doesn’t show up in the top-line growth story.

The ROIC Story: Good, But Not Great

Let’s be honest here, because this is where the Costco comparison flatters PriceSmart unfairly. PriceSmart’s ROIC runs at roughly 11–13% depending on methodology respectable, clearly above the cost of capital, but nowhere near Costco’s ~26%. The reason for the gap is structural. Costco basically prints cash — vendors finance its inventory for free because Costco sells product so fast it collects cash from members before it has to pay its suppliers. Its payables-to-inventory ratio exceeds 100%. PriceSmart can’t replicate this in markets with less efficient supply chains, more complex customs environments, and currency risk embedded in every import shipment. Building a club in Kingston, Jamaica involves logistics complexity that simply doesn’t exist in Phoenix, Arizona.

The other drag is trapped cash. As of August 2025, $59.7 million in cash was trapped in Trinidad alone due to USD illiquidity money PriceSmart earned but can’t repatriate. This is a real cost of doing business in these markets that doesn’t appear in any P/E ratio but absolutely affects the quality of earnings.

The Risks: Four Things That Could Ruin the Story

The remittance time bomb: This is the risk that almost no retail analyst is modeling properly. Several of PriceSmart’s core markets Honduras, El Salvador, Guatemala, Nicaragua have remittance inflows representing 20–25% of GDP. These are countries where a significant share of consumer purchasing power comes from family members working in the United States and sending money home. A new 1% US tax on remittances has been in discussion since early 2026. Management said they’ve seen no slowdown yet, but that’s exactly what a lagging indicator looks like. A 10% reduction in remittance flows to Honduras doesn’t just hurt one club it structurally reduces the spending power of the middle-class consumer that PriceSmart’s entire Central America segment is built on.

Amazon and Mercado Libre coming for the category: PriceSmart’s digital channel grew 29.4% in Q1 2026 impressive but starting from a small base of around 6% of sales. Mercado Libre is the more immediate threat than Amazon in these markets. It has been building logistics infrastructure aggressively across Latin America, and its penetration in Colombia and Central America is growing faster than most investors realize. The warehouse club model’s core value proposition “come to us and buy in bulk at low prices” is only durable as long as the friction of not going is lower than the convenience of staying home. That equation changes gradually, then suddenly.

New management navigating a perfect storm: David Price (son of founder Robert Price) took over as CEO in 2024, with Gualberto Hernandez stepping in as new CFO. Leadership transitions at any company carry execution risk but navigating one simultaneously with a major market expansion (Chile), a major technology implementation cycle (RELEX inventory management, ELERA POS, new distribution centers in Panama, Guatemala, and imminently Trinidad and Dominican Republic), and a fresh all-time-high valuation is a lot to ask of a new leadership team in their first full earnings cycle.

The FX treadmill: Operating in 12+ currency regimes is a constant drag that never goes away. Currency fluctuations negatively impacted net merchandise sales by approximately $36.8 million, or 0.8%, in fiscal 2025 and that was a relatively mild year. Any significant strengthening of the USD (which is exactly what you get in a risk-off environment or during a US economic boom) directly compresses PriceSmart’s reported results.

2. The Numbers

Current Valuation

Price: ~$146 | Market Cap: ~$4.5B | Enterprise Value: ~$4.6B (conservative balance sheet, light net debt)

Profitability Snapshot

Revenue (FY2025): $5.27B

Net Income: $147.9M

Membership Income: $85.6M (growing 13.7% YoY)

Operating Margin: ~4.4%

Net Margin: 2.8%

Operating Cash Flow: $261.3M

Free Cash Flow: ~$125–140M after capex

Digital Sales: $306.7M (6% of net merchandise sales, up 21.6% YoY)

Valuation Metrics

P/E (TTM): ~31x | Forward P/E: ~26.6x

5-Year Historical Average P/E: ~22x

Earnings Yield: ~3.2%

S&P 500 Earnings Yield: ~3.49%

10Y US Treasury: ~4.18%

The interpretation here is important and most retail write-ups skip it: PSMT’s earnings yield is actually below the risk-free rate and roughly in line with the broader market. You are not being compensated with a yield premium for taking on emerging-market currency risk, remittance dependency, and a valuation above historical norms. That’s what “priced for perfection” means in real numbers, not just as a cliché.

Shareholder Returns

Dividend Yield: ~0.92% | Annual dividend: $1.40/share (raised 11.1%)

Buyback Yield: essentially zero no active program

Total Shareholder Yield: ~1%

Quality Indicators

Debt/Equity: ~25.5% (clean balance sheet)

Membership income as % of operating income: ~36.8% (up from 35.8% in 2023) this ratio trending up is a very good sign; it means the high-margin recurring revenue is growing faster than the commodity merchandise business

12-month renewal rate: 88.8% remarkable for any subscription business

3. The Napkin Math

A. EPS Growth: ~8% annually

Revenue has compounded at roughly 7–9% for the past several years. With 3–4 new clubs per year, mid-single-digit comp sales growth, Chile on deck, and private label expansion providing quiet margin lift, 8% EPS growth is a reasonable central case — not heroic, not pessimistic. Share count reduction is essentially zero: there’s no buyback program. Margin expansion from the RELEX/ELERA tech investments is a wildcard that could push this to 9–10%, but treat it as optionality rather than base case.

B. Shareholder Yield: ~1%

Dividend: ~1%. Buybacks: ~0%. That’s your total cash return from the business. Compared to Costco, which runs buybacks plus occasional special dividends for a total shareholder yield closer to 2.5–3%, this is a meaningful gap. PriceSmart is a growth story, not a capital return story which means the entire investment thesis depends on the growth materializing.

C. The Valuation Impact: -6.6% per year (the honest math)

Current P/E: ~31x

5-Year Historical Average P/E: ~22x

Multiple contraction math: (22/31)^(1/5) - 1 = -6.6% per year headwind

This is the number that almost every bull case quietly sweeps under the rug. If P/E simply normalizes back to where PSMT spent most of the past five years, it erases the majority of your annual return. This isn’t a bear case it’s a reversion to historical means.

D. The Final Equation

Against the S&P 500’s ~10% historical annual return and a risk-free rate of ~4.2%, a 2.4% expected return on a position with emerging market risk, currency exposure, and a management transition is not a compelling proposition at current prices.

The bull case requires believing the re-rating is permanent that Chile, Platinum membership acceleration, and tech-driven margin expansion justify a new, higher structural P/E. In that scenario: P/E stays flat at 31x, EPS compounds at 10%, and you’d earn roughly 11% annually. Achievable? Yes. Likely enough to bet on at all-time highs? That’s the question.

4. My Proprietary Insight

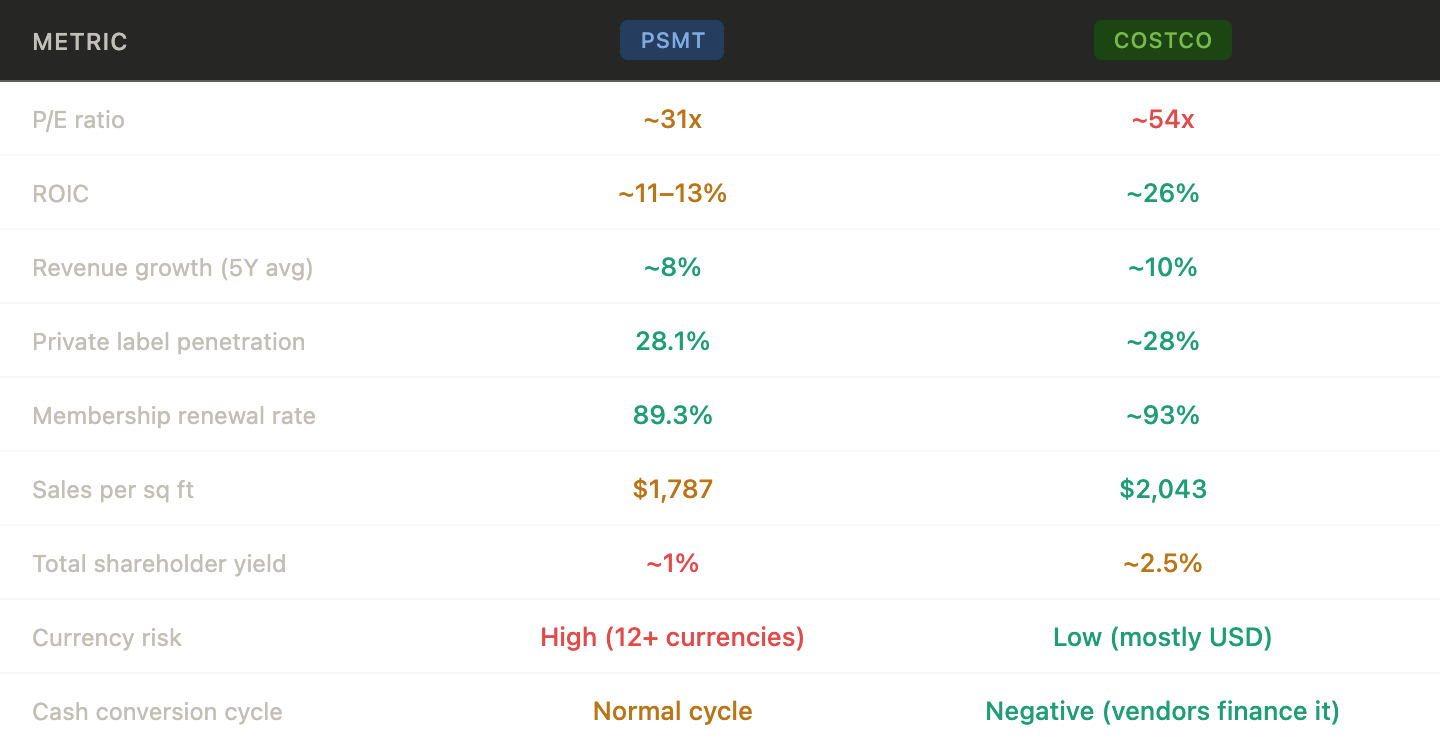

The Costco Comparison Is Flattering And Actively Misleading

Here’s what that table is really telling you. The surface level metrics that bulls love to point to private label penetration, renewal rates are genuinely comparable to Costco. That’s impressive for a $4.5B company operating in Guatemala and Trinidad. But the structural advantages that make Costco worth 54x earnings simply don’t exist at PriceSmart. Costco runs a negative working capital cycle it collects cash from members and sells inventory so fast that its suppliers effectively give it a free loan. PriceSmart operates a normal working capital cycle with trapped cash on top of it. Costco’s ROIC is double PriceSmart’s because Costco barely needs capital to grow it generates so much cash internally that it funds expansion, pays dividends, and buys back roughly 1–2% of its shares per year. PriceSmart needs to keep deploying capital to build new clubs in markets where repatriating that capital is sometimes literally impossible.

At 31x P/E, the market is assigning PriceSmart roughly 58% of Costco’s multiple while PriceSmart delivers roughly 42–50% of Costco’s ROIC. The relationship is actually fairly priced at those levels, which is precisely the problem: there is no obvious bargain here relative to the benchmark.

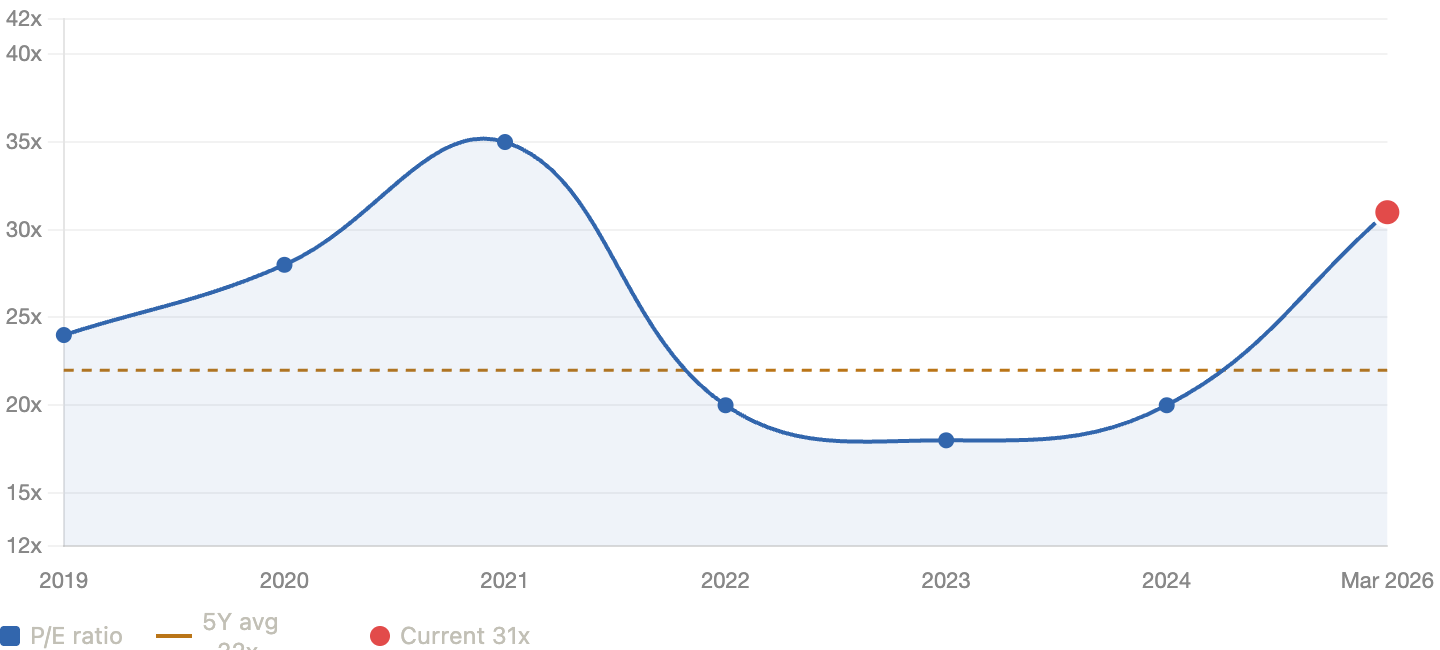

The P/E History: What The Chart Tells You

The chart makes the valuation story viscerally clear. PSMT spent 2022–2024 trading between 18–20x P/E a level that historically has been an excellent entry point, and one that offered a reasonable earnings yield versus treasuries. The stock has now traded up to 31x, matching and slightly exceeding the COVID era peak multiple from 2021. That 2021 peak unwound painfully: the stock re-rated back to 18x by 2022–2023. The question is whether 2026’s re-rating has better fundamental justification than 2021’s did. The honest answer: partially yes (Chile, Platinum, tech stack maturation), but not entirely.

The Chile Opportunity: The Detail Nobody Is Pricing Correctly

Chile is the wealthiest country in Latin America, with a GDP per capita of $17,067 in 2024. About 45% of Chile’s 19.5 million residents are middle class a concentration that maps almost perfectly onto PriceSmart’s target member demographic.Retail sales in Chile have been growing at 6–8% year-over-year through 2025, with electronics and household goods leading the expansion. And crucially: there is currently no warehouse club operating in Chile. Not one. Costco has explored the market and decided not to enter. Sam’s Club is US-only. The field is completely open.

Now here’s the detail everyone misses. Chile is not just a bigger version of PriceSmart’s existing markets. The Chilean retail market is valued at $27.16 billion and projected to reach $45.5 billion by 2034 at a 5.9% CAGR. That is a market nearly five times the size of, say, Costa Rica, in a single country. A successful 5-club rollout in Santiago and surrounding metro areas could add 3–5% to PriceSmart’s annual revenue within three years of opening and these would be clubs operating in a higher-income consumer environment where Platinum membership uptake and private label adoption rates could exceed anything PriceSmart has seen in its existing footprint. Chile’s consumers are more sophisticated, more digitally engaged, and higher-income than the average PriceSmart market. That means potentially better unit economics per club something that could structurally shift the ROIC story that I criticized earlier.

The counterfactual worth stressing: Colombia was also considered a risky bet when PriceSmart entered in 2011. Today, Colombia is PriceSmart’s largest single-country segment outside Central America. PriceSmart opened in Bogotá, expanded to seven locations across the country, and made it work despite currency volatility and political risk. Chile has better fundamentals than Colombia did at entry on virtually every metric: higher GDP per capita, stronger institutions, lower inflation, a more mature consumer base, and greater FX stability. If the playbook repeats and there’s no structural reason it shouldn’t Chile is the most important catalyst in PSMT’s story for the next five years.

The Hidden Margin Engine: Membership Economics Getting Quietly Better

Here’s the stat that should stop you in your tracks: in 2023, membership income represented 35.8% of PriceSmart’s total operating income. By 2025, that figure had risen to 36.8% and the trend is accelerating as Platinum members grow as a share of the base. Why does this matter? Because membership income is essentially 100% margin. It costs almost nothing incremental to renew a member. Every dollar of membership growth flows almost directly to the bottom line, while merchandise revenue requires inventory, logistics, and store labor to generate each dollar. As Platinum members grow from 17.9% to, say, 25% of the base over the next three years, the operating leverage embedded in PriceSmart’s model starts to look meaningfully different than what the historical margin profile suggests. This is the margin expansion story hiding inside the growth story and it’s not captured in any simple revenue growth estimate.

5. My Take

Sleep Well at Night Score: 6/10

The business itself is a 9/10 durable, dominant in its niche, recurring revenue, loyal members, no serious competitive threat on the horizon in its existing markets. The price is a 4/10 at current levels. Average them and you get a 6. That’s a business worth watching very closely, not necessarily owning aggressively today.

What Excites Me

Chile is legitimately transformational if executed. A first-mover entering Latin America’s wealthiest consumer market with no warehouse club competition, a highly educated urban middle class, and retail sales growing at 6–8% annually is the kind of opportunity that can redefine a company’s growth trajectory. Colombia proved the playbook works in an unfamiliar market. Chile is a better market than Colombia was at entry.

The Platinum membership flywheel is accelerating faster than consensus models. Going from 12.3% to 17.9% of the membership base in a single year is extraordinary and Platinum members spend more, renew at higher rates, and generate almost entirely incremental margin. This is the quiet compounder within the compounder.

The technology investment cycle is ending. RELEX for demand planning, ELERA for POS, new distribution centers rolling out across multi-club markets all of this has been a capex drag in 2024–2025. In 2026–2027, these investments should start showing up as cost savings, better inventory turns, and margin expansion rather than expenses.

What Worries Me

The remittance tax is the underappreciated macro risk. Markets like Honduras (remittances = ~25% of GDP) and El Salvador (~24% of GDP) are central to PriceSmart’s Central America segment. A structural reduction in consumer purchasing power in those markets from a sustained policy change is not in any analyst’s model and would directly hit the comp sales that underpin the growth narrative.

At 31x P/E, the market is pricing in everything going right simultaneously: Chile works, Platinum accelerates, tech delivers margin, macro cooperates. Even one of those “ands” failing to materialize over a 5-year period creates meaningful multiple compression.

Insider selling at all-time highs with zero insider buying over the past six months including the President/COO and CFO is the kind of signal worth filing away, even if insider activity is an imperfect indicator.

The One-Liner

A genuinely world-class business model operating in a category it invented, with Chile as a potentially transformational bet but the stock has already priced in the good news. Worth owning on your watchlist and revisiting seriously if it pulls back toward 22–24x.