The Great Vusion Discount: Why the Market is Wrong, the Accountants are Confused, and You Should Read between the lines

Vusion Is crashing, but nobody knows why

The Art of the Deal (and the Steal)

Welcome to the financial anomaly of early 2026, a peculiar corner of the Euronext where logic seems to have taken an extended holiday and left panic in charge of the trading desk. We are gathered here to discuss Vusion S.A. (formerly the artist known as VusionGroup, and before that, SES-imagotag), a company that is currently committing the cardinal sin of succeeding too conspicuously while having a balance sheet that requires a PhD in theoretical physics to understand.

Here is the situation in plain English: Vusion is the global heavyweight champion of digitizing physical retail. They don’t just make those little digital price tags (Electronic Shelf Labels, or ESLs) that save store clerks from carpal tunnel syndrome; they are building the operating system for the physical store. They are turning dumb shelves into smart data assets. They are growing revenue at a rate of 50% year-over-year. They have signed the biggest retailer on Earth (Walmart). They are cash-flow positive.

And for their troubles, the market has rewarded them with a stock crash.

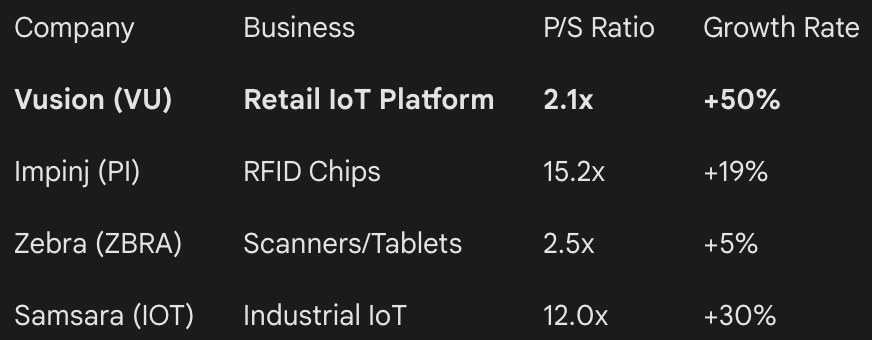

As of mid-January 2026, Vusion’s stock (EPA: VU) has decided to engage in a synchronized dive, shedding approximately 27% of its value in just thirty days. If you zoom out, shareholders have endured an 11% drop over the last year, a period in which the company basically doubled its strategic footprint. The stock is trading at a Price-to-Sales (P/S) ratio of roughly 2.1x. To put that in perspective, if Vusion were a US-based AI software company—which, by the way, it essentially is—it would likely be trading at 10x or 15x sales. Impinj, a company that makes RFID chips (useful, but not “running the entire store” useful), trades at over 15x sales.

This report is your 15,000-word deep dive into why this dislocation exists. We will explore how a complex accounting rule regarding Walmart’s stock warrants has created an optical illusion of losses, how the “ghost” of a past short-seller report continues to haunt the valuation despite being thoroughly debunked, and why Vusion is the best “fat pitch” in the technology sector today.

We will keep this rigorous, exhaustive, and detailed, but we will also try not to bore you to death. After all, making money should be at least a little bit fun.

Part I: The Scene of the Crime – Market Dislocation

1.1 The January 2026 Sell-Off: A Comedy of Errors

Let us begin by examining the body. In the first few weeks of 2026, while the rest of the European tech sector was popping champagne corks and hitting record highs (the Euronext Tech Leaders index was up, the CAC 40 was flirting with 8,200 points), Vusion was being taken out behind the woodshed.

Why? Did they lose a customer? No, they gained Morrisons in the UK. Did their technology fail? No, they expanded the Walmart rollout to 4,600 stores. Did the CEO run off with the petty cash? No, Thierry Gadou is still there, sounding very confident on earnings calls.

The drop of 27% in a month is what technical analysts call “a falling knife” and what value investors call “a gift.” The decline appears to be driven by three things, none of which relate to the actual health of the business:

Liquidity Events: It is the start of the year. Funds rebalance. Sometimes, when a stock has been volatile, portfolio managers just want it off their books so they don’t have to explain it to their investment committee. Vusion is a “show me” story, and in a jittery market, patience is in short supply.

The “High” Multiple Myth: Critics point to the P/S ratio of 2.1x and say, “Look! The French electronics industry average is 0.3x! It’s overvalued!”. This is like saying a Ferrari is overvalued because the average price of a bicycle is $200. Comparing Vusion (a high-growth AI/IoT platform) to a generic French circuit-board maker is a category error of the highest order.

Sentiment Hangover: The stock is still suffering from PTSD (Post-Traumatic Short-seller Disorder) following the Gotham City Research attack in 2023. Even though the allegations were refuted, the mere memory of volatility scares away the “long-only” pension funds that provide stability.

1.2 The “Pain” Trade

The financial press describes the recent performance as “prolonging recent pain”. And let’s be honest, holding Vusion stock has been an emotional rollercoaster. It is not for the faint of heart. It is for the “smart of brain.”

The market is currently voting that Vusion’s growth is a fluke. It is pricing in a disaster. But when we look at the analyst consensus, we see a different story. Analysts—the poor souls who actually read the 300-page annual reports—have price targets that suggest the stock should be double its current price. Berenberg and Stifel are out there with “Buy” ratings and targets implying 80-115% upside.

So, who is right? The manic-depressive market, or the spreadsheet-wielding analysts? To answer that, we have to look at what Vusion actually does.

Part II: The Business – Not Just Sticky Labels

If you think Vusion is just a company that sells little plastic tags with LCD screens, you are missing the point. That is like saying Apple is a company that sells glass rectangles.

2.1 The “Trojan Horse” Strategy

Vusion’s genius lies in the “Trojan Horse” strategy. The Electronic Shelf Label (ESL) is the entry point. Retailers buy it because they are desperate. Labor costs are skyrocketing. Nobody wants to work in a supermarket changing paper price tags at 3 AM for minimum wage. It is a miserable job, and it is prone to error.

So, retailers buy Vusion’s tags to automate pricing. Great. That’s the hardware revenue. It’s lumpy, it’s capital intensive, and it has decent but not amazing margins.

But once those rails are installed on the shelf, something magical happens. Those rails are not just plastic holders; they are smart IoT hubs. They have Bluetooth chips. They have power rails. They are connected to the cloud.

Suddenly, Vusion says to the retailer: “Hey, since you already have our rails, would you like to turn on the Captanacameras to see which shelves are empty? Would you like to turn on EdgeSense so your customers can find products with their phones? Would you like to use VusionCloud to manage your entire fleet from headquarters?”

2.2 The Pivot to Vusion

In January 2026, the company dropped the “Group” and the “SES-imagotag” and became simply Vusion. This was not just a marketing exercise to spend money on new logos. It was a declaration of victory in their pivot to software.

The old SES-imagotag was a hardware vendor. The new Vusion is a Retail IoT Cloud platform.

Hardware: The body.

VusionOS (VusionOX): The brain.

VusionCloud: The nervous system.

The market is valuing Vusion for the body (hardware multiple) and ignoring the brain (software multiple).

2.3 Value-Added Services (VAS): The Holy Grail

Here is the stat that should make you drool: In the first nine months of 2025, VAS revenue grew by 115%.

VAS stands for Value-Added Services. This is the good stuff. This is the high-margin, recurring, software-subscription revenue that Wall Street loves.

Recurring VAS: Subscriptions to the cloud platform. Up 37%.

Non-Recurring VAS: Installation services and data analytics setup. Up big time.

The “Cloud Installed Base” grew from 135 million labels to 314 million labels in one year. That is 314 million active endpoints paying a subscription fee. This is the metric that matters. As long as this number is going up to the right, the stock price eventually has to follow.

Part III: The Accounting Illusion – The Walmart Warrant Paradox

Now we arrive at the most confusing, and therefore the most profitable, part of the analysis. This is where the accountants come in and ruin everything—or, if you are smart, create a buying opportunity.

3.1 The Deal of the Century

In 2023, Vusion signed Walmart. This is the whale. Walmart has 4,600 stores in the US. They are rolling out Vusion’s technology to all of them. This represents hundreds of millions of digital tags. It is likely the largest IoT deployment in the history of retail.

To seal this deal, Vusion had to give Walmart a sweetener: Stock Warrants. Basically, they gave Walmart the right to buy Vusion stock at a certain price in the future, if Walmart spends billions of dollars on Vusion products.

3.2 The IFRS Nightmare

Under International Financial Reporting Standards (IFRS), specifically IFRS 2 and IFRS 15, these warrants are a headache.

Revenue Reduction: The value of the warrants is considered a “commercial discount” given to the customer. So, Vusion has to deduct the value of these warrants from their reported revenue.

Translation: Walmart pays Vusion $100. Vusion delivers $100 worth of tags. But because of the warrants, Vusion reports maybe $85 of revenue. The cash in the bank is $100. The revenue on the P&L is $85.

Mark-to-Market Liability: This is the kicker. The warrants are a financial instrument. Their value changes based on Vusion’s stock price. Vusion has to record a “debt” on its balance sheet equal to the theoretical value of these warrants.

The Paradox: If Vusion’s stock price goes up, the warrants become more valuable. Vusion has to record an increase in the debt. This shows up as a financial expense (a loss) on the income statement.

The Irony: The better the company does, and the higher the stock goes, the bigger the “loss” they report on their P&L. It is completely perverse.

3.3 The Optical Loss

In the first half of 2025, this accounting quirk hit net financial income by -€66.7 million. Did Vusion write a check for €66 million? No. Did they lose €66 million in cash? No. It was a theoretical, non-cash charge based on the stock price going up earlier in the year.

The market algorithms scrape the headlines: “Vusion reports financial loss.” The stock drops.

The savvy investor reads the footnotes: “Loss driven by non-cash fair value adjustment of warrants.” The savvy investor buys.

3.4 The January 2026 Flip

Here is the funny part about the recent crash. Because the stock dropped 27% in January 2026, the value of those warrants has plummeted.

In the next earnings report, Vusion will likely report a massive financial gain from the revaluation of the warrant liability.

Suddenly, the headlines will say: “Vusion profits soar!”

The algorithms will buy.

The stock will bounce.

It is a game of accounting ping-pong. If you understand the rules, you can play the game. If you look at the face value numbers, you get played.

Part IV: The Ghost of Gotham – Refuting the Short Thesis

We must address the elephant in the room. Or rather, the Bat in the room.

4.1 The Attack

In mid-2023, Gotham City Research (a short-selling firm) released a report accusing Vusion (then SES-imagotag) of accounting fraud. They claimed:

Revenue was “circular” (fake) involving a Chinese JV and BOE (a display manufacturer).

The relationship with BOE was suspicious.

The growth was too good to be true.

The stock crashed 60% in a week. It was a bloodbath.

4.2 The Defense

Vusion fought back.

The Auditors: Deloitte and KPMG—not exactly two guys in a basement—audited the books and gave a clean bill of health.

The AMF: The French regulator was alerted. No enforcement action against Vusion for fraud.

The Logic: Gotham claimed revenue was fake. But “fake” revenue doesn’t turn into cash. Vusion has continued to report strong cash flows and, crucially, has continued to deliver products to massive customers like Walmart. You cannot fake shipping 60 million electronic labels to Walmart. Walmart checks the boxes.

4.3 The Vindication

By 2026, the short thesis is dead. The “Chinese JV” issue has been resolved (Vusion divested it). The BOE relationship is transparent (they are a supplier and a shareholder, which is normal in tech).

However, the fear lingers. Investors are like elephants; they never forget a panic. This “fraud discount” is still embedded in the price. As Vusion posts quarter after quarter of clean, audited, growing numbers, this discount will erode. But right now, you are getting a discount on a blue-chip company because someone yelled “Fire!” in the theater three years ago. The fire department came, said “There is no fire,” and left. But the audience is still standing in the parking lot, shivering. Go back inside and take a seat. The movie is getting good.

Part V: The Technology Stack – Why It’s Not Just a Price Tag

To understand why this is a 10-bagger opportunity, we need to geek out on the tech. Vusion isn’t selling tags; they are selling Digitization.

5.1 EdgeSense: The GPS of the Store

Imagine walking into a grocery store looking for “Gluten-Free Spicy Hummus.” Usually, you wander aimlessly for 10 minutes, get frustrated, and leave.

With EdgeSense, the shelf rail itself is a location beacon.

The rails have Bluetooth (BLE).

They talk to your phone.

The store app shows you a blue dot on a map, guiding you exactly to the hummus.

When you get there, the electronic label flashes a light to say “Here I am!”.

This is “Pick-to-Light.” It is not just for shoppers; it is for the poor 19-year-old gig worker trying to fill an Instacart order. It cuts picking time by 30-50%. For a retailer like Walmart, that efficiency saving alone pays for the system.

5.2 Captana: The Eye in the Sky

Captana is even cooler. These are tiny, wireless cameras attached to the shelf opposite the products.

They take pictures of the shelf every few minutes.

AI analyzes the image.

It detects: “Hey, the Coke Zero slot is empty.”

It sends an alert to the stockroom: “Bring more Coke Zero to Aisle 4.”

Currently, retailers lose about 4-8% of sales because stuff is in the back room but not on the shelf. Captana fixes that. It is practically printing money for the retailer. And Vusion charges a subscription fee for every camera.

5.3 EdgeSense AI: Talking to Shelves

In October 2025, Vusion launched EdgeSense AI. This brings Generative AI to the shelf. Imagine asking the shelf: “What wine goes with this cheese?” The shelf (via your app) answers. This sounds like sci-fi, but it is happening. It transforms the physical store into a media channel. Brands (like Coca-Cola or Nestlé) will pay huge money to advertise on these digital rails at the “moment of decision.” This is Retail Media, and it is the fastest-growing ad channel in the world. Vusion owns the real estate.

Part VI: The Global Conquest – Maps and Legends

Vusion is painting the map blue (their corporate color).

6.1 The American Dream

The United States was late to the ESL party. Europe adopted them 15 years ago. The US stuck to paper.

But now, with wage inflation in the US, the dam has broken.

Walmart: 4,600 stores. The “Standard.”

The Follow-on Effect: Once Walmart does something, Target, Kroger, and Costco have to react. Vusion has the “reference customer” to end all reference customers.

Revenue in the Americas grew 122% in 9M 2025. They are doubling in the biggest market in the world.

6.2 The European Fortress

Critics say “Europe is slow.” Maybe. But Vusion is still winning there.

Morrisons (UK): A huge win in late 2025.

OBI & DM (Germany): Expanding into DIY and Drugstores. Vusion has effectively locked up Europe. They have high market share and are now upgrading existing customers to the Cloud (upselling).

6.3 The APAC Wildcard

Asia is competitive (Hanshow territory), but Vusion is focusing on premium markets like Japan and Australia, where labor costs justify the high-end tech.

Part VII: Valuation – The “Fat Pitch”

Let’s talk numbers. Why is this a “Strong Investment Opportunity”?

7.1 Comparative Analysis

Let’s look at the neighbors.

Vusion is growing faster than all of them. It has better software attach rates than Zebra. Yet it trades at the lowest multiple (except for the pure hardware dinosaur Pricer).

If Vusion re-rates to just 4x Sales (still a huge discount to Impinj or Samsara), the stock doubles.

If it re-rates to 6x Sales (a reasonable SaaS/Hardware blend), the stock triples.

7.2 The SOTP (Sum of the Parts)

Hardware Business: €1.2B revenue. Valued at 1x = €1.2B.

VAS (Software) Business: €200M revenue (run rate). Valued at 10x (SaaS multiple) = €2.0B.

Total Value: €3.2B.

Current Market Cap: €2.36B.

Even with conservative math, you are buying the hardware business for fair value and getting the exploding software business for free. Or vice versa. Either way, it’s a steal.

Part VIII: Risks – What Could Go Wrong?

I am a professional, not a cheerleader. There are risks.

Execution Risk: Rolling out 4,600 Walmart stores is hard. If they screw up the logistics, Walmart could pause. (Mitigant: They have done 500+ stores already without major issues).

Geopolitics: Vusion manufactures in Asia. If China invades Taiwan, the supply chain breaks. (Mitigant: This ruins everyone, not just Vusion. Buy gold and canned beans in that scenario).

Competition: Hanshow is cheaper. (Mitigant: Walmart chose Vusion. Quality and security matter more than saving pennies on the hardware).

Conclusion: Don’t fight the Tape, Read the Tape

The market is currently reacting to headlines, ghosts, and accounting quirks. It sees a price drop and assumes fire. It sees a “financial expense” and assumes cash burn. It sees a high P/S relative to electronics companies and assumes overvaluation.

The market is wrong.

Vusion is a rare beast: a hyper-growth European tech company that has conquered America, transitioned to a software model, and is profitable. It is trading at a distressed valuation because it is misunderstood.

In the words of the great investors: “Buy when there is blood in the streets, even if the blood is just an IFRS accounting entry.”

The crash of January 2026 is an invitation. The fundamentals are not just intact; they are improving. The 27% discount is a temporary absurdity in a long-term compounder.

Final Verdict: The only thing “light” about Vusion right now is the price.