The Constellation Nobody Talks About

Lumine Group is down 58% from its peak while its cash machine just posted the best year in company history. Here's why the market is confusing an accounting cleanup with a broken thesis.

0. The Story

In 2013, a software developer turned telecom entrepreneur named David Nyland walked into the offices of Constellation Software the most celebrated capital allocation machine in Canadian history with a pitch: give me a mandate and some capital, and I’ll build a vertical market software empire in the telecom and media niche. Constellation said yes. What followed was a decade-long apprenticeship inside one of the greatest compounders ever built, during which Nyland’s team quietly assembled a portfolio of 28 companies across 30+ countries, mostly businesses that telecom operators had been relying on for 20 years and couldn’t imagine living without. In early 2023, Constellation handed Nyland the keys to the car and spun the whole thing out as an independent public company. The Lumine Group era had officially begun.

Fast forward to today and the stock is down 58% from its peak. It was trading at $55 CAD a year ago. As of April 4, 2026, it sits at $23 CAD, with a 52-week low of $17.77. The underlying business, meanwhile, just delivered its best year ever revenue up 15%, operating income up 31%, and free cash flow available to shareholders up a staggering 153%. That kind of disconnect between the business and the stock price is usually noise. But it’s worth digging to understand whether the market has spotted something real, or whether this is one of those rare moments where a high-quality compounder gets mispriced because the fear is louder than the facts.

That’s exactly why we’re doing this now.

1. The Machine

A. The Simple Explanation

Let me paint you a picture. It’s 2003. A mid-size telecom operator in South Africa say, a regional mobile carrier needs software to handle subscriber billing. They hire a small boutique software shop that builds them a custom billing system. The integration takes two years. Every customer record, every payment workflow, every regulatory reporting module is wired into this platform. The software is ugly. The interface looks like it was designed by someone who peaked during the Windows XP era. But it works, perfectly, every time, for 20 years straight.

Now imagine someone offers to sell that telecom a shiny new cloud-native billing system. The demo is beautiful. The vendor promises 40% efficiency gains. The IT team is excited. And then the CFO runs the numbers: the migration would cost $12 million in engineering time, carry a 30% risk of data corruption, and require 18 months of parallel running. The answer is no. It will always be no. The new software never gets bought, not because it isn’t better, but because the old software is too embedded to remove.

This is what Lumine buys. The average business unit in Lumine’s portfolio was 21 years old when it was acquired, and customer retention rates run into decades. Lumine doesn’t buy great software. It buys infrastructure. And infrastructure doesn’t get replaced it gets maintained, managed, and milked for cash, forever.

The business model itself is almost offensively simple: find these sleeping giants of telecom and media software, buy them from retiring founders or distracted corporates at 3–5x EBITDA, plug them into the Constellation operating playbook, improve their margins, and use the resulting cash flow to buy the next one. The companies are never sold. The founders often stay on. The products keep running. Repeat for 30 years.

B. The Moat : Three Layers That Stack

Most businesses have one moat. Lumine has three that reinforce each other, and understanding all three is the real alpha here.

Moat #1: Switching costs so high they’re structurally permanent. The businesses Lumine owns don’t just have high switching costs they have switching costs of a kind that make the concept of churn almost theoretical. BSS (Business Support Systems) is software that manages telecom operators’ billing, customer service, order fulfillment, and product offerings. OSS (Operational Support Systems) manages the network itself real-time monitoring, traffic routing, fault detection. These aren’t productivity tools. These are the nervous system of a telecom. Replacing them is roughly equivalent to a hospital replacing its patient records system mid-operation. It is technically possible. Nobody does it voluntarily. Large-scale BSS renewals can cost hundreds of millions of dollars, making exit from existing vendors practically impossible.

The result: Lumine’s recurring revenue runs at 94%, which isn’t a metric, it’s a confession from customers that they’re not going anywhere.

Moat #2: The Constellation DNA. This is the one most people underappreciate. Lumine didn’t invent its operating model it inherited it from the most successful VMS acquirer in history. Mark Leonard built what one analyst calls “fractal decentralization” a system where capital allocation is itself decentralized to individual platforms, each running the same playbook at smaller scale. Substack Lumine is exactly that: a platform-within-a-platform, running the Constellation operating system with a defined niche mandate. The institutional knowledge that comes with this lineage is impossible to replicate. You can’t just decide to run this model. Constellation maintains a proprietary database of roughly 100,000 potential acquisition targets, where business managers with software backgrounds not finance professionals nurture relationships for years before approaching a seller. Lumine has been building the same kind of proprietary pipeline in its niche since 2013. That’s 12 years of relationship-building with telecom software founders who have never heard of most private equity firms. That pipeline is a moat in itself.

Moat #3: The Carve-Out Expertise. Here’s the one that nobody talks about enough. The spin-outs of Topicus and Lumine weren’t done for optics they were deliberate moves to preserve strategic focus, and critically, to create separate acquisition currencies for deals that Constellation’s own scale made uneconomical. What this means in practice is that Lumine has developed a very specific specialty: buying orphaned software divisions from large telecom vendors who no longer want to run software businesses. In 2024 alone, Lumine completed the carve-out of Nokia’s Device Management and Service Management Platform businesses for up to €185 million, then bought cloud-native 5G assets from Casa Systems out of Chapter 11 effectively acquiring distressed telecom software assets while their original owners were in financial distress. This is not a skill you develop overnight. Nokia trusted Lumine with 500 employees and thousands of global customers because Lumine had already done a previous carve-out with Nokia and earned that trust. This is a compounding institutional advantage, not a repeatable commodity deal.

C. The ROIC Story

Lumine targets a hurdle rate of 20–25% ROIC on acquisitions, based on NOPAT. Their historical portfolio of companies achieved a 27% average ROIC over two years before the spinoff. That’s not aspirational it’s historical. And there’s a reason this is possible when it’s nearly impossible for most acquirers.

The businesses Lumine buys are structurally beautiful from a working capital perspective. Software companies, especially older subscription-based ones, often collect annual licenses upfront. That means customers are effectively providing Lumine with free float cash-in-hand before a single dollar of service is delivered. This negative working capital profile (a concept Topicus’s analysts have flagged as one of the most underrated features of VMS businesses) means Lumine’s acquisitions are frequently self-financing within the first year. Add to that the margin expansion that comes from applying the Constellation playbook disciplined R&D spending, rationalized sales costs, shared back-office functions and you get acquisitions that generate their initial invested capital back in 3–5 years.

The catch, and this matters: ROIC tends to decrease as deal size increases. Lumine’s sweet spot was historically $10–15M deals. As they’ve moved into $185M (Nokia) and $258M (Synchronoss) territory, maintaining that 20-25% hurdle becomes harder. The small-deal machine still runs they’re acquiring at roughly 2–3 deals per year at small sizes alongside the larger carve-outs but the mix is shifting, and the math gets tighter at scale.

D. The WideOrbit Deep Dive The Hidden Crown Jewel

Most analysis of Lumine treats WideOrbit as a line item. It deserves its own section.

WideOrbit was founded in 1999 by Eric Mathewson after he realized the buying and selling of media advertising was shockingly manual and fragmented. By the time Lumine acquired it in early 2023, it had become the system of record for over 5,000 TV and radio stations, processing more than $35 billion in advertising revenue annually.

Put that number in perspective: $35 billion. The entire U.S. local TV advertising market generates roughly $23–24 billion per year. WideOrbit processes more than that because it also handles national networks, cable, and radio. WideOrbit’s WO Traffic platform is used by broadcast station groups to manage more than 90% of U.S. local TV ad revenue.

90% market share in the traffic management layer of U.S. local TV. This is a monopoly with a product name almost nobody has ever heard of. Every time a local TV station sells an ad slot for a car dealership, a law firm, a political campaign the technical infrastructure routing that transaction almost certainly runs through WideOrbit software. The broadcaster can’t function without it. Switching would mean rebuilding the entire revenue operations stack from scratch.

WideOrbit’s CTO has recently described how the company is now building AI agents to handle broadcast advertising’s most time-consuming workflow: makegoods the process of rescheduling commercials that didn’t air as planned, which traditionally consumed enormous amounts of manual labor. This isn’t AI risk. This is AI opportunity. WideOrbit is using AI to sell more productivity to the same captive customers who are already paying for the base platform. Think of it as the Jibbitz on the Croc the core platform is irreplaceable, and AI just lets you sell add-ons at high margin to customers who have nowhere else to go.

E. The Risks Don’t Skip This

Risk 1: Organic growth is almost zero, and occasionally negative. This is the real bear case and it deserves honest treatment. Q4 2025 showed just 1% organic growth after FX adjustments and prior quarters showed negative organic growth. The entire revenue growth story is acquisitive. If Lumine misses a year of deals because prices spike, credit markets tighten, or the Nokia-style carve-out pipeline dries up revenue growth stops. The business still generates cash, but the compounder thesis requires continuous reinvestment at high ROIC, and that requires deal flow. This is genuinely the Achilles heel.

Risk 2: The Synchronoss integration. Synchronoss was Lumine’s first-ever public company acquisition at an enterprise value of $258 million, it’s by far the largest deal in company history. The prior average deal was around $12–15 million. Integrating a public-company-scale business with global Tier-1 telecom operator customers, hundreds of employees, and the cultural complexity of a NASDAQ-listed entity is an entirely different animal. Lumine’s “autonomous operations” playbook works brilliantly for small, founder-led businesses. Whether it scales to a business this size is an open empirical question.

Risk 3: The telecom industry is structurally challenged. The telecom sector faces genuine disruption 5G network virtualization, cloud-native OSS/BSS stacks from hyperscalers, and AI-driven automation are all evolving, and Lumine’s customers are often the older, smaller, more financially constrained operators least equipped to navigate that disruption. If customers shrink, get acquired, or go bankrupt, Lumine’s revenue base erodes. The bull case says the software survives regardless of who owns the telecom. The bear case says a consolidating telecom industry means fewer customers paying fewer bills.

Risk 4: The governance structure. Constellation retains a single “super-voting share” in Lumine, giving CSU permanent control over strategic direction despite not owning a majority of common shares. This isn’t necessarily bad CSU’s track record is impeccable but minority shareholders are structurally reliant on the parent acting in everyone’s interest. Always worth remembering.

2. The Numbers

All figures in USD unless specified. Stock price and market cap in CAD.

Current valuation (April 4, 2026):

LMN trades at CAD $23.00, with a 52-week range of CAD $17.77–$55.00.

Market cap approximately CAD $5.9B (~USD $4.3B).

Enterprise value roughly ~USD $4.1B after netting out $232M in cash against modest debt (D/E at 21%).

Profitability snapshot (FY 2025, USD):

Revenue: $765.7M (+15% YoY). Operating income: $275.7M (+31% YoY). Net income: $118.8M (vs. a $258.9M net loss in 2024). Cash from operations: $236.5M (+106% YoY). FCFA2S: $217M (+153% YoY).

A word on that net income swing. The 2024 “loss” was entirely accounting noise: when Lumine spun out, it issued preferred and special shares to WideOrbit’s founders and Constellation. These converted mandatorily into common shares in March 2024, triggering an ~$87M accrued dividend obligation that was paid in shares, not cash, and showed up as an enormous non-cash GAAP charge in 2024. Post-conversion, the capital structure is now completely clean no preferred, no special shares, no non-cash distortions. Investors can now track the business purely through FCFA2S. This is not a small point. The entire reason FCFA2S exploded 153% in 2025 isn’t because the business went from bad to great in one year, it’s because a structural accounting fiction that was masking real cash generation got removed. The cash was always there. Now you can see it.

Valuation metrics:

EV/FCFA2S: ~19x (USD $4.1B EV / $217M FCFA2S) the cleanest multiple for this machine

Forward P/E: ~24x (analyst estimates)

FCF yield on market cap: ~3.7% (USD ~$217M / ~$4.3B USD market cap adjusted)

Operating margin: 36% in 2025 vs. ~26% in 2022 10 points of margin expansion in 3 years (see chart)

EBITDA margin: ~39% (CAD terms, per TradingView)

Versus risk-free assets:

10-year Canadian government bond: ~3.3%

S&P 500 earnings yield: ~4.5%

LMN FCF yield: ~3.7% below the S&P, above the risk-free rate

At face value this looks uninspiring. But this comparison ignores the reinvestment engine. A business yielding 3.7% in FCF that then compounds that FCF at 20–25% ROIC through acquisitions is a fundamentally different animal than a bond yielding 3.3%. The bond returns 3.3% forever. LMN’s FCF pool grows with each deployment.

Shareholder return structure:

Dividend yield: 0%

Buyback yield: 0%

Total shareholder yield: 0%

This is intentional and correct. Every dollar returned to shareholders via dividends or buybacks is a dollar not compounding at 20–25% ROIC. The only way this structure makes sense to reject is if you believe management can’t find deals at acceptable returns which is the real bear thesis, stripped down to its core.

Quality indicators:

Debt/Equity: 21% conservative, especially post-Synchronoss

Operating margin trajectory: 22% (2020) → 36% (2025) relentless structural improvement

Revenue CAGR since 2020: ~58% (from ~$80M to $766M) though heavily acquisition-driven

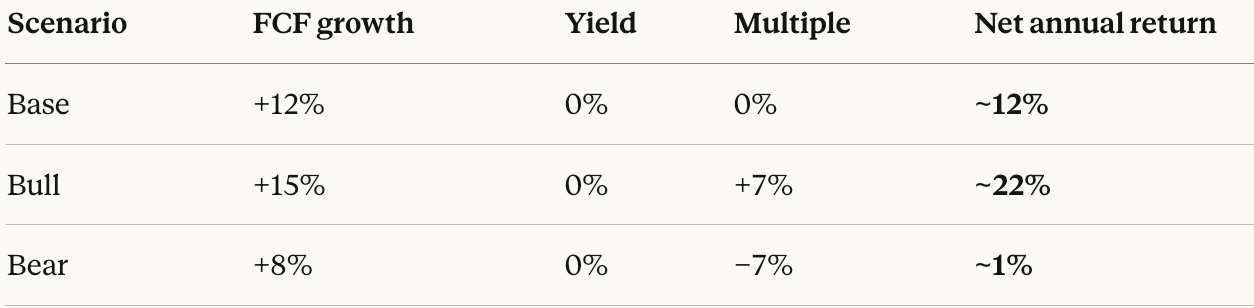

3. The Napkin Math

Let’s build the 5-year return scenario from scratch, showing the work.

Step A: FCF/earnings growth estimate.

The engine has two cylinders: organic and acquisitive. Organic is essentially 0–2% (being generous given recent history). Acquisitive growth depends on how much capital Lumine deploys and at what ROIC. With $217M of FCFA2S in 2025 and a $310M credit facility available, Lumine can deploy $300–400M per year into acquisitions. At a 20% after-tax ROIC, that’s $60–80M of incremental annual earnings power per year of deployment. Over five years, assuming deal flow stays consistent and Synchronoss integrates cleanly, you can build to a mid-teens FCFA2S CAGR without much heroism. Being conservative:

Organic contribution: ~1%

Acquisitive contribution: ~10% (roughly ~2 deals/year at $50M avg. enterprise value + one larger deal every other year)

Operational margin improvement: ~2%

Total FCF/earnings growth: ~12–13% per year

Step B: Shareholder yield.

0%. Full stop. Everything goes into M&A. No dividends, no buybacks, no yield at all.

Step C: Multiple expansion or contraction.

This is where the real uncertainty lives. At peak ($55 CAD), LMN was trading at roughly 40–50x FCFA2S premium “baby Constellation” pricing baked in. At $23 CAD, it sits at approximately 19–20x FCFA2S. The Constellation family has historically traded at 25–35x FCFA2S when operating well. What happens over 5 years depends entirely on whether the market regains its confidence in the model:

Base case: Multiple stays flat around 20x as organic growth concerns persist → 0% annual impact

Bull case: Synchronoss integrates cleanly, organic stabilizes at +2%, multiple re-rates to 28x → (28/20)^(1/5) − 1 ≈ +7% per year tailwind

Bear case: Organic worsens, M&A deal quality deteriorates, multiple contracts to 14x → (14/20)^(1/5) − 1 ≈ −7% per year headwind

Step D: The Final Equation:

The base case at ~12% is slightly better than the S&P 500 historical average of ~10%. The asymmetry is interesting: the bull and bear cases are not equally probable. The mechanism for bull case realization (Synchronoss integration + organic stabilization + multiple re-rating) is a clear sequence of trackable events. The bear case requires a structural deterioration in deal flow that hasn’t appeared yet. This isn’t a 50/50 coin flip.

4. My Proprietary Insight

The Three Things The Market Is Getting Wrong Simultaneously

Insight #1: The “AI will kill VMS” panic is inverted for Lumine specifically.

The market spent 2025 pricing in the death of vertical market software via AI disruption. The logic is: ChatGPT-like tools will replace legacy enterprise software with flexible AI agents that are cheaper and better. This thesis is reasonable for horizontal enterprise software generic CRMs, basic ERP, productivity tools. It is nearly backwards for what Lumine owns.

David Nyland himself described in his semi-annual letter how AI is already a core capability leading to concrete product innovations, such as Openwave’s “AI Smart Assistant.” The Crocs-and-Jibbitz analogy from the CEO of Chapters Group (a similar VMS acquirer in Germany) is brilliant here: Lumine owns the “shoe” the robust, irreplaceable BSS/OSS core that 20-year customer relationships are built on and AI lets them produce the “Jibbitz” faster and cheaper. AI doesn’t replace the shoe. AI is new Jibbitz. Every AI automation module WideOrbit builds goes on top of the existing traffic management platform that 89% of U.S. local TV broadcasters are already paying for. The platform stickiness doesn’t decrease. The revenue per customer increases.

There’s also a counterintuitive second-order effect: BSS/OSS market consolidation is actually bad for telecom operators, who face fewer vendor choices and higher switching costs as the sector concentrates. Lumine operates in an environment where the structural forces are actively making its customers more captive over time. The market read this as a headwind. It is structurally a tailwind.

Insight #2: The 153% FCFA2S jump is real, not a fluke.

When a metric jumps 153% in one year, the first instinct is: “this is a distortion, find the accounting gimmick.” In this case, it’s actually three legitimate improvements compounding simultaneously, which is rarer and more durable than it looks:

First, the preferred share conversion in March 2024 removed ~$87M of annual cash obligations (dividends on the preferred and special shares) from the FCFA2S calculation. This is structural and permanent. Second, the Nokia Motive and Casa Systems Axyom.Core acquisitions in 2024 added revenue and operating income that only hit a full year of FCFA2S contribution in 2025. Acquisitions always look cheap in Year 2 vs. Year 1. Third, the operating leverage on a fixed-cost base: as Lumine’s revenue grew from $668M to $766M, operating income grew disproportionately from $210M to $276M a 31% operating income gain on a 15% revenue gain. That’s margin expansion compounding on a larger base. None of these three drivers is going away.

Insight #3: The WideOrbit valuation alone is probably worth more than the current stock price implies.

Here’s the napkin math the market seems to have forgotten. WideOrbit, when Lumine acquired it in early 2023, was generating approximately $167M in annual revenue. Two years of Constellation-playbook margin improvement later, assume it’s generating $180–190M in revenue at an operating margin of 35–40% (consistent with mature VMS businesses under this model). That’s ~$65–75M in operating income from WideOrbit alone. Apply a 20x multiple to that conservative for a business with 90% U.S. local TV market share and effectively 100% recurring revenue and you get $1.3–1.5B in implied value for WideOrbit alone.

The current market cap sits at CAD $5.9B (~USD $4.3B). So you’re paying roughly $2.8B for everything Lumine owns that isn’t WideOrbit — the 30+ other portfolio companies, the Nokia/Motive carve-out assets, the Axyom.Core 5G platform, the Synchronoss personal cloud business, and the institutional M&A infrastructure built over 12 years. At the current price, the market is valuing all of that at roughly $2.8B. That feels like a lot of value to get for free.

5. My Take

Sleep Well at Night Score: 6.5/10

The business is 9/10. The valuation overhang from organic growth anxiety, deal execution risk on Synchronoss, and the VMS-sentiment hangover knock it down to 6.5. I sleep fine most nights, but that Synchronoss integration sits in the back of my mind.

What Excites Me:

The preferred share conversion is the most important event in Lumine’s public history that nobody talks about. You went from a business where $258M of net losses hid $217M of real cash generation to a clean, transparent FCF machine. The first year of “real” financials was 2025. The market hasn’t fully absorbed this.

WideOrbit is a hidden monopoly. Managing more than 90% of U.S. local TV ad revenue through your software and processing over $35 billion in annual advertising transactions is the kind of market position that would attract a $5B+ valuation on its own in a bull market. Right now it’s being valued implicitly at something like $1.3B as part of a discounted conglomerate. At some point, someone notices.

The spin-out structure gives Lumine a unique acquisition currency it can offer sellers Lumine stock as rollover equity, creating instant multiple arbitrage between what Lumine trades at and what it pays for acquisitions. As the stock recovers from its selloff, this currency becomes more powerful. A recovering stock price is an acquisition advantage for Lumine in a way it isn’t for most companies.

What Worries Me:

The organic growth line needs to turn. Right now it’s 0–1%. If it goes negative on a sustained basis because telecom customers consolidate, cut budgets, or churn out of some of the smaller legacy businesses the acquisition machine is running to stand still rather than compound. The businesses age, and aging software businesses eventually lose customers to greener solutions. That clock is always ticking.

Synchronoss is uncharted territory. The integration of a formerly public company is a different complexity class than Lumine’s typical $12M founder-led acquisition , and the “autonomous operations” playbook that works brilliantly for small businesses hasn’t been tested at this scale. If the first large public-company acquisition stumbles, it could reset the market’s confidence in the model for years.

The valuation still prices in some optimism. At 19–20x FCFA2S, Lumine isn’t screamingly cheap it’s reasonably valued if the model continues to execute. There’s no margin of safety if execution falters.

The One-Liner:

Baby Constellation at its cheapest price in two years, the plumbing is world-class, the preferred-share accounting fog has finally lifted, and the market is confusing a structural re-rating with a value trap. This is one to watch very closely into the next earnings call on April 30th.