Terry Smith's Fundsmith Q4 2025: The "English Warren Buffett" Is Losing His Touch

Fund Performance 2025: +0.9% | MSCI World Index: +12.8% | 5th Consecutive Year of Underperformance

The Setup: A Quality Investing Icon in Crisis

Terry Smith—the man who turned £10,000 into £71,000 over 15 years—just delivered his 5th consecutive year of underperformance. The fund returned just 0.9% in 2025, compared to 12.8% for the MSCI World Index.

His investors could have earned more in a savings account.

The “English Warren Buffett” mantra of “buy good companies, don’t overpay, do nothing” is starting to look less like genius and more like dogma. Let’s dissect what went wrong, what he’s doing about it, and whether his strategy is broken—or just out of favor.

1. The Q4 2025 Portfolio: What He Owns (And What Changed)

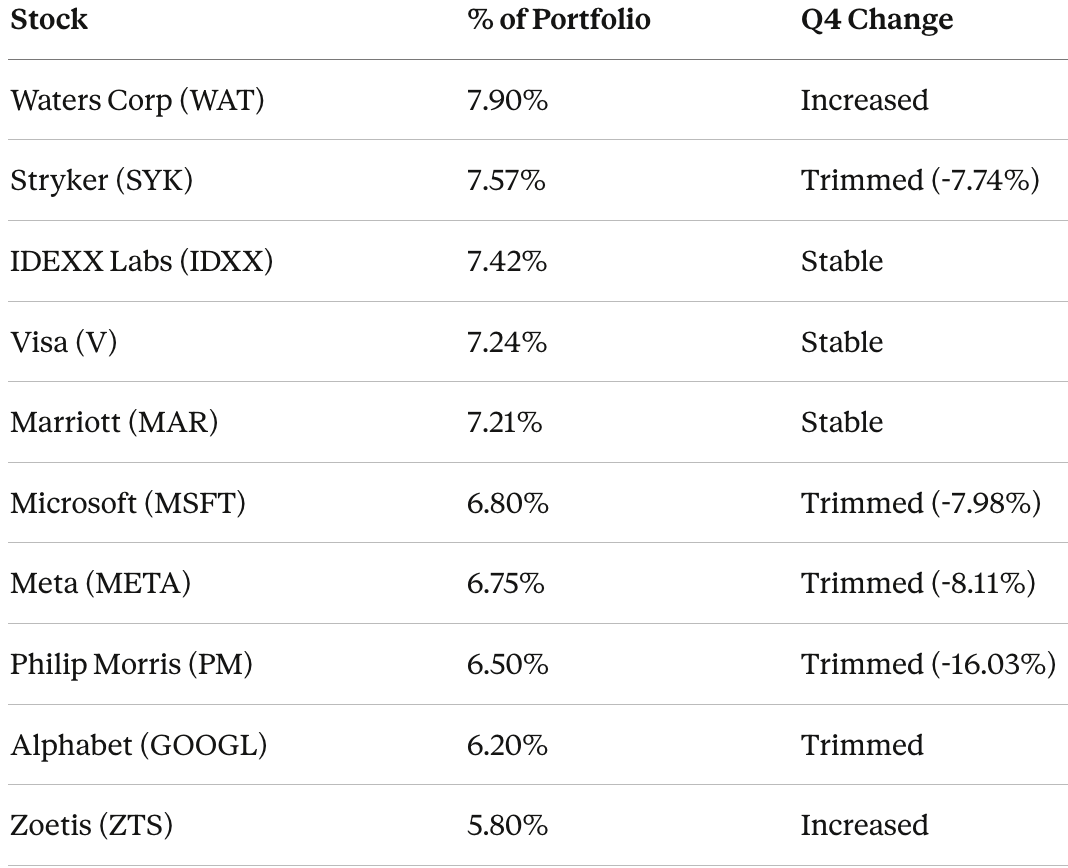

Top 10 Holdings (as of Dec 31, 2025):

Portfolio Stats:

Total Holdings: 37 stocks (down from 39 in Q3)

Portfolio Value: $17.1 billion

Top 5 Concentration: 38.3%

Turnover: 3.2% (extremely low)

2. What He Did in Q4 2025: The Moves

🔴 Major Trims (Profit-Taking or Panic?):

Philip Morris (PM): -16.03% (largest reduction)

Narrative: Smith is taking profits after PM’s run-up, but this is also his most defensible holding in a recession. Cutting it aggressively signals he’s not positioned for a downturn.

Microsoft (MSFT): -7.98%

Narrative: Trimming MSFT after it became a top holding. But here’s the problem: he’s selling the onemega-cap tech stock that’s actually generating ROI on its AI capex. Meanwhile, Julian Robbins (Fundsmith’s Head of Research) warned that Big Tech capex went from $64B in 2018 to $210B in 2024, with forecasts of $281B by 2026. Smith is spooked by the spending, but he’s cutting the winner (MSFT) while avoiding the bubble stock (NVDA).

Meta (META): -8.11%

Narrative: Meta was his best performer in 2024, yet he’s trimming it. This is peak “sell your winners, hold your losers” behavior. Meta is printing cash ($65B FCF annually), buying back shares aggressively, and trading at 22x P/E. Why trim?

Stryker (SYK): -7.74%

Narrative: Medical devices are recession-proof and non-cyclical. Stryker has a 20-year track record of 10%+ EPS growth. Trimming this is bizarre unless he’s desperate for cash to redeploy elsewhere.

🟢 Additions (Where’s He Putting Money?):

Waters Corp (WAT): Now 7.90% (top holding)

What it is: Lab equipment maker (liquid chromatography systems)

Waver Take: This is peak Terry Smith—boring, high-margin (20%+ operating margin), sticky customers (pharma/biotech labs). But it’s also tiny ($12B market cap) and cyclical. If pharma R&D spending slows, Waters gets crushed.

Zoetis (ZTS): Increased stake

What it is: Animal health (pet meds, livestock vaccines)

Waver Take: Defensible moat (pets are recession-proof), but trading at 35x P/E. This is expensive even by Smith’s standards.

Intuit (INTU): New position (Q1 2025, still held in Q4)

What it is: QuickBooks, TurboTax

Waver Take: Great business, but he’s late to the party. Intuit trades at 30x P/E and growth is slowing (10% revenue growth vs. 15-20% historically).

🔴 Full Exits:

PepsiCo (PEP): Sold completely in Q1 2025

Waver Take: PEP is the definition of a Terry Smith stock—boring, defensive, high ROE, dividend aristocrat. Selling it signals he’s abandoning his own playbook.

Apple (AAPL): Sold in 2024

Rationale (per Smith): “We bought Apple at half its current rating and sold it when the rating doubled during a period where sales grew by zero over two years.”

Waver Take: This is the only smart move he made. Apple is dead money (0% revenue growth for 2 years, trading at 30x P/E). But he should have sold 2 years ago.

3. The Narrative: What’s Terry Smith Thinking?

Smith’s 2026 annual letter reveals three core concerns:

Concern #1: Index Fund Bubble

Smith warned that “more than 50% of US equity fund assets are now in index trackers” and quoted John Bogle (founder of Vanguard) saying this “will lead to distortions because they’re invested without consideration of quality or valuation.”

By the end of 2025, the top 10 constituents of the S&P 500 accounted for 39% of the market value and 50% of the annual return.

Waver Take: He’s right. Passive investing has created a self-fulfilling prophecy where the Mag 7 (Apple, Microsoft, Alphabet, Amazon, Meta, Tesla, Nvidia) get bid up regardless of fundamentals. But his solution is wrong: instead of owning the best of the Mag 7 (MSFT, META), he’s trimming them and hiding in Waters Corp and Zoetis. This is fighting the Fed AND the market.

Concern #2: AI Capex Insanity

Julian Robbins noted that Big Tech capex is forecast to hit $281 billion by 2026, up from $64 billion in 2018. Smith is terrified that this spending won’t generate returns.

Waver Take: He’s partially right. Most AI capex will be wasted (see: Meta’s $15B metaverse bonfire). But he’s throwing the baby out with the bathwater. Microsoft is the one company actually monetizing AI (Copilot, Azure AI, GitHub Copilot). By trimming MSFT, he’s avoiding the winner to dodge the losers.

Concern #3: Novo Nordisk Disaster

Novo Nordisk was “the biggest detractor to the fund in 2025, contributing a 3 percentage point loss overall.” Smith said the company “parlayed a market-leading position in what is probably the most exciting drug development for about three decades into a secondary position.”

Waver Take: This is where Smith’s “buy and hold” philosophy breaks down. Novo had one job—dominate the GLP-1 weight-loss drug market with Wegovy. Instead, Eli Lilly ate their lunch with Zepbound (better drug, better supply chain). Smith held on way too long, watching a 30% drawdown turn into a -20% position. This isn’t “patience”—it’s stubbornness.

4. The Strategy: Is It Still Working?

Terry Smith’s 3-Step Formula:

Buy good companies (high ROE, high margins, pricing power)

Don’t overpay (reasonable valuations)

Do nothing (low turnover, long holding periods)

Does the Math Still Work?

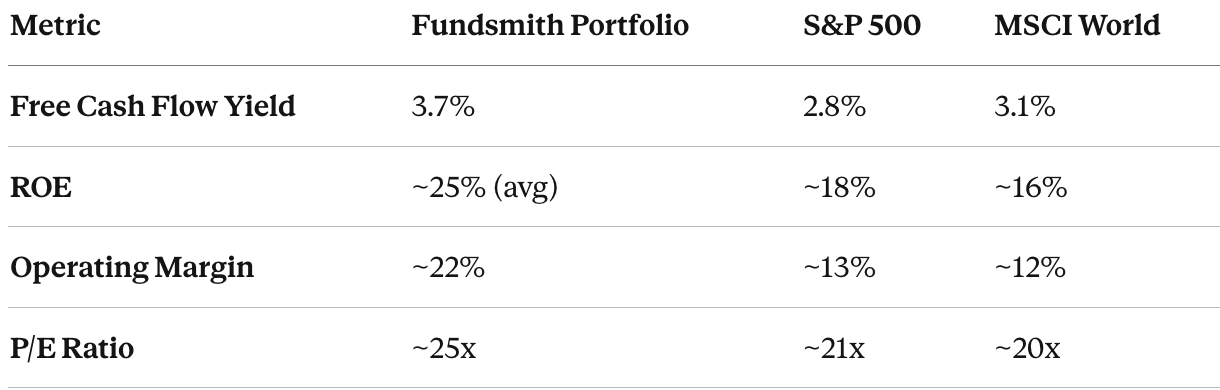

Waver Take: The quality is still there. Smith owns better businesses than the index. But he’s overpaying for that quality. His portfolio trades at a 25% premium to the S&P 500 (25x P/E vs. 21x), yet it’s delivering inferior returns.

5. The Problems: What’s Broken?

Problem #1: Stubbornness Disguised as Patience

Smith’s strategy is “only invest in good companies, try not to overpay, and do nothing.” Portfolio turnover was just 3.2% last year.

Waver Take: There’s a difference between patience and paralysis. Holding Novo Nordisk through a -30% drawdown isn’t discipline it’s denial. Great investors (Buffett, Druckenmiller, Ackman) aren’t afraid to admit mistakes and cut losses. Smith is.

Problem #2: Fighting the Mag 7 Tide

Smith sold Apple and Amazon. He never owned Nvidia or Tesla. He’s trimming Microsoft and Meta.

Waver Take: The Mag 7 aren’t just “expensive tech stocks.” They’re monopolies with:

40%+ net margins (vs. 10% for the S&P 500)

$500B+ annual FCF (combined)

Network effects that make them more valuable as they scale

Smith is betting against the most dominant business models in history because they’re “overvalued.” But as Keynes said: The market can stay irrational longer than you can stay solvent.

Problem #3: Lack of Diversification in Mega-Caps

Smith’s largest holding (Waters Corp) is a $12 billion market cap company. His top 10 are all $50-500B market cap.

Waver Take: He’s avoiding the Mag 7 because they’re “too big” and “distorting the index.” But the Mag 7 are the economy now. They generate 35% of S&P 500 earnings. By underweighting them, Smith is betting against the U.S. economy.

Problem #4: Expensive “Quality”

Smith’s portfolio trades at 25x P/E with 10% growth (on average). That’s a PEG ratio of 2.5x.

Compare to:

Microsoft: 30x P/E, 15% growth (PEG = 2.0x)

Meta: 22x P/E, 20% growth (PEG = 1.1x)

Visa: 28x P/E, 12% growth (PEG = 2.3x)

Waver Take: He’s paying more for slower growth than the Mag 7. This is value destruction, not value creation.

6. The Verdict: Is Terry Smith Washed?

The “Sleep Well at Night” Score: 6/10

Why It’s a 6 (Not a 10):

⚠️ 5 years of underperformance: Not a fluke. This is a structural problem.

⚠️ Stubborn refusal to adapt: The world changed (AI, passive investing, Mag 7 dominance). Smith didn’t.

⚠️ Expensive portfolio: Paying 25x P/E for 10% growth is bad math.

⚠️ Novo Nordisk disaster: A -3% hit to the fund from one stock proves the portfolio isn’t as diversified as he claims.

Why It’s Not a 0:

✅ Long-term track record: Since inception (Nov 2010), Fundsmith returned 612.9% vs. 467.6% for the benchmark. That’s still 2.6% annualized alpha over 15 years.

✅ Quality businesses: He owns great companies (Visa, MSFT, Stryker, IDEXX). The strategy is sound—the execution is flawed.

✅ Low fees: 1% annual fee, 3.2% turnover. He’s not churning the portfolio to generate commissions.

7. The Waver Take: What Should He Do?

Option 1: Embrace the Mag 7 (Selectively)

Stop fighting the tide. Own the best of the Mag 7:

Microsoft: AI monetization, Azure dominance, 15% growth

Meta: 22x P/E, $65B FCF, aggressive buybacks

Alphabet: Search monopoly, YouTube cash cow, 18x P/E

Avoid: Nvidia (too expensive), Tesla (Elon risk), Amazon (razor-thin margins).

Option 2: Cut the Losers

Novo Nordisk: Sell. Eli Lilly won the GLP-1 war.

Philip Morris: Hold, but stop trimming. This is your recession hedge.

Waters Corp: Trim. Too small, too cyclical for a 7.9% position.

Option 3: Add Real Inflation Hedges

Smith’s portfolio has zero exposure to:

Energy (oil, nat gas)

Materials (copper, steel)

Financials (banks, insurance)

If inflation re-accelerates or we get a recession, his portfolio gets destroyed.

8. The One-Liner

“A 15-year track record of excellence, undone by 5 years of stubbornness. Terry Smith’s refusal to adapt to a Mag 7-dominated world is turning quality investing into a value trap.”

9. Should You Still Invest in Fundsmith?

At Current Levels:

If you’re NEW to Fundsmith: PASS. You can replicate his portfolio with an S&P 500 ETF + a quality factor tilt and pay 0.1% fees instead of 1%. There’s no edge here.

If you OWN Fundsmith: HOLD, but on thin ice. Give him 2 more years. If he underperforms again in 2026-2027, cut your losses. The 15-year track record is impressive, but 5 years of underperformance is too long to ignore.

What to Watch:

Does he stop trimming MSFT and META? If he keeps selling winners, the strategy is broken.

Does he add Mag 7 exposure? If he refuses to own the dominant companies, he’ll keep underperforming.

Does he admit Novo was a mistake? If he doubles down, run.

10. The Bottom Line

Terry Smith built Fundsmith on a simple, elegant strategy: own great businesses, don’t overpay, do nothing.

But the world changed:

Passive investing broke valuation discipline

AI created a capex arms race

The Mag 7 became 35% of the S&P 500

Smith didn’t adapt. He’s still fighting 2015’s battles in 2026.

The result? 5 consecutive years of underperformance, culminating in a +0.9% return in 2025 when cash paid 4.5%.

For Waver Capital readers: If you want quality investing done right, look at:

Fundsmith’s holdings (Visa, MSFT, Stryker) → Buy them individually

Quality factor ETFs (QUAL, JQUA) → Same strategy, 0.1% fees

Active managers who adapted (Li Lu, Chuck Akre, Nick Sleep disciples)

Terry Smith is still a smart guy. But right now, his fund is a 6/10—good enough to not panic sell, but not good enough to recommend.