[Portfolio] Brookfield Corporation Q1 2026

Same machine, better price, new catalysts. The discount just got wider and the reasons for it just got thinner.

Back in early 2026, I wrote about Brookfield’s record-breaking FY 2025 results $6.0 billion in distributable earnings, $112 billion raised, and a stock trading at a ~31% discount to management’s stated intrinsic value of $68. The thesis was simple: a world-class capital machine compounding at 15%+, mispriced because it’s too complex for most investors to bother with.

Three months later, the Q1 2026 results are in. The machine is still running. The discount has actually widened.

Let’s update the numbers.

If you want the original articles you can find them here :

1. What Just Happened (Q1 Snapshot)

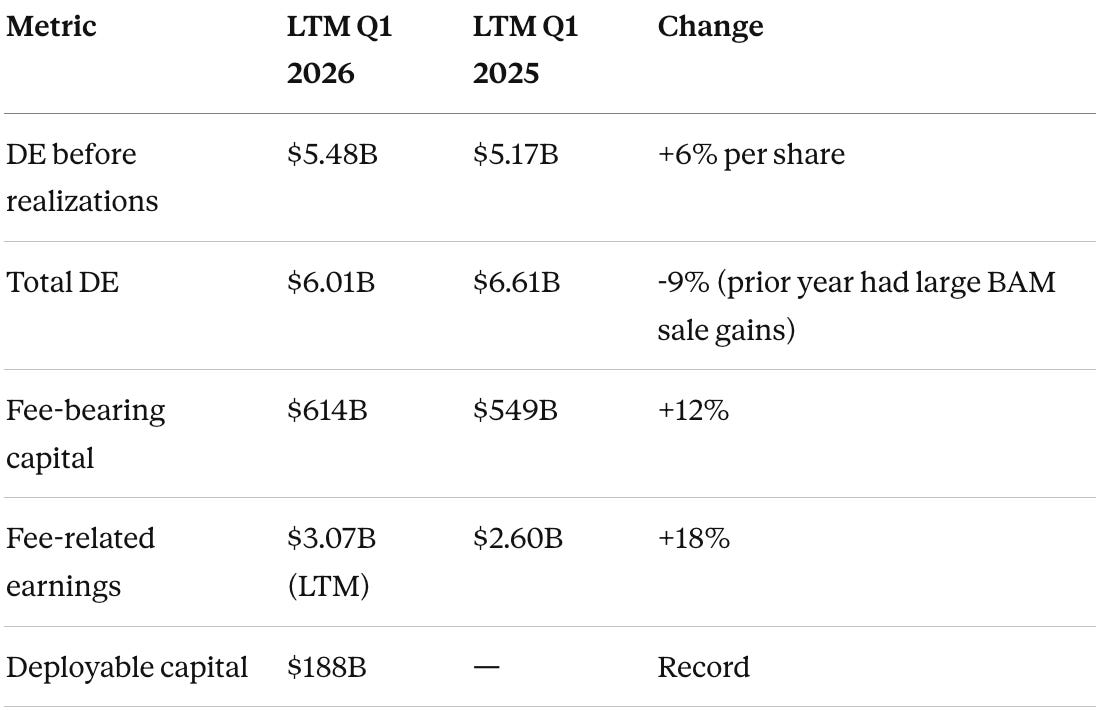

Brookfield reported $1.55 billion ($0.66/share) in Distributable Earnings for Q1 2026—essentially flat versus Q1 2025’s $1.549 billion. But the headline masks the important detail: DE before realizations grew 7% year-over-year, from $1.301 billion to $1.393 billion. The recurring earnings engine is getting stronger.

For the last twelve months (LTM) ended March 31, 2026:

The drop in total LTM DE is a simple prior-year comp issue: Q1 2025 included ~$1 billion in one-time disposition gains from the sale of a portion of BN’s stake in BAM (used to fund the AEL insurance acquisition). Strip that out and the underlying business is growing cleanly.

2. The Three Engines: Where Things Stand

Engine #1: Asset Management

This remains the crown jewel and it’s accelerating.

Fee-bearing capital hit $614 billion, up 12% year-over-year. Fee-related earnings grew 18% over the LTM to $3.07 billion. Year-to-date fundraising is already $67 billion (including $21 billion in Q1 alone), boosted by a $40 billion insurance mandate from Just Group—which Brookfield just closed the acquisition of. The seventh vintage flagship private equity fund is in its first close, targeting essential services and industrial businesses—what management calls “hard assets” for a cycle where everyone wants exactly that.

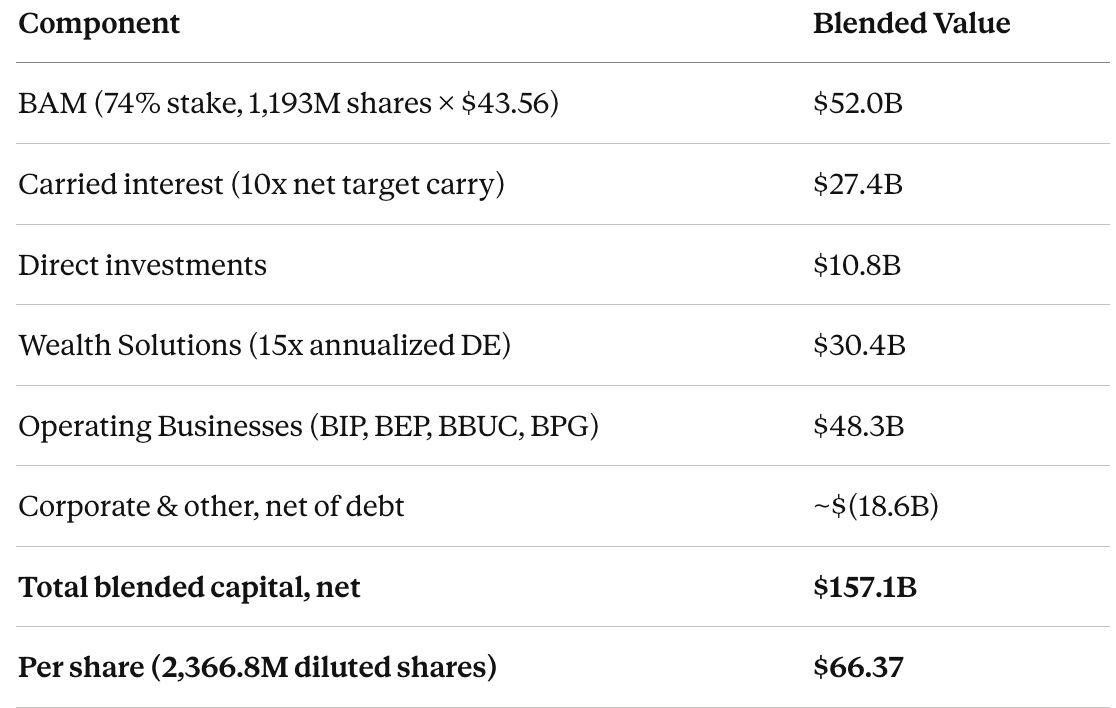

The asset management business now generates $1.953 billion in annualized DE at Brookfield’s share. At a 10x multiple on $2.7 billion net target carried interest, the carried interest component alone is worth $27.4 billion. Add to that the market value of BN’s 74% stake in BAM (1,193 million shares × $43.56/share = ~$52 billion at quarter-end), and asset management capital on a blended basis is ~$96.6 billion.

One new detail worth watching: Brookfield is quietly building a technology investment portfolio ($2.3 billion of balance sheet capital) that includes ~$1 billion in SpaceX shares, ~$500 million committed to Figure (humanoid robotics), a joint venture with OpenAI called The Deployment Company, and half ownership of Pinegrove Capital (a venture secondaries platform). These are still small relative to the overall business but reflect the “Watch, Learn, Invest” playbook that Bruce Flatt describes in this quarter’s shareholder letter early bets on secular trends before they become consensus.

Engine #2: Wealth Solutions (Insurance Float)

DE was $430 million for the quarter and $1.671 billion for the LTM growing but still building. The bigger news is what happened after quarter-end: Brookfield completed the acquisition of Just Group, a UK pension risk transfer platform. This added $40 billion to the insurance asset base, bringing total insurance assets to $180 billion.

Annualized cash flow is now $2.028 billion (including Just Group), supporting a $30 billion valuation at management’s 15x multiple. Return on equity is 15%, holding steady.

The gross spread remains intact at 2.24%: earning 5.77% on invested assets, paying 3.53% in cost of funds. Simple math: at $180 billion in assets, that spread generates ~$4 billion gross before operating costs. The Berkshire-playbook-with-real-assets analogy from my previous piece is even more apt now.

One strategic move worth flagging: Brookfield has announced the combination of BN and BNT (the Brookfield Wealth Solutions paired security). Shareholder votes are scheduled for July 16, 2026. The rationale is capital efficiency the combined entity unlocks roughly $145 billion of permanent capital to support the insurance business’s continued scaling. The company is also evaluating similar simplifications for its listed infrastructure and energy vehicles. Simpler structure = lower complexity discount = potential multiple expansion.

Engine #3: Operating Businesses

This is the quietest engine and intentionally so. DE was $360 million for Q1 ($1.536 billion LTM), down from $426 million in Q1 2025 due largely to reduced real estate distributions (BPG went from $215 million to $120 million quarterly). Infrastructure (BIP: +6% YoY) and Energy (BEP: +7% YoY) both grew.

The real estate fundamentals, however, remain solid: super core office occupancy at 96%, core plus at 95%, and net rents on new office leases running 15% above expiring levels. During Q1, Brookfield refinanced Two Manhattan West with a $1.9 billion non-recourse mortgage at 5.53%, repaid the prior $1.5 billion mortgage, and pocketed $400 million in net cash while keeping the building. That’s the asset recycling flywheel at work.

Monetization activity in Q1: $17 billion of asset sales, substantially all at or above carrying values. Accumulated unrealized carried interest stands at $11.8 billion (net $7.9 billion after costs). Management continues to guide toward $6 billion of carried interest realizations over the next three years.

3. The Updated Napkin Math

Management’s blended intrinsic value per share, as of March 31, 2026: $66.37 (down from $68.08 at year-end, primarily due to BAM’s share price declining from $52.39 to $43.56 during a volatile market quarter).

The components:

BN shares were repurchased at an average of $41 year-to-date management’s own characterization is a ~40% discount to intrinsic value. That’s not a marketing claim; it’s backed by the sum-of-the-parts math above. $470 million of BN shares and $575 million of BAM shares were repurchased in Q1 alone, in the open market, during the market volatility.

At $44/share (approximate current price):

P/E on LTM DE before realizations: $44 / ($5.48B / 2.37B shares) = ~18x

P/E on total LTM DE: $44 / ($6.01B / 2.37B shares) = ~17x

Discount to blended intrinsic value: ~38%

FCF Yield (DE before realizations): $2.32/share ÷ $44 = 5,2%

FCF Yield (total DE): $2.54/share ÷ $44 =5,7%

The spread over 10-year Treasuries (~4.3%) remains over 100 basis points on a recurring basis, and over 150 basis points including realizations.

4. What Changed Since My Last Piece

The FY 2025 article used $44/share as the price. The stock has since sold off further, to ~$41 and came back to 44 now, ironically making the thesis more compelling since Earnings grew, not less. Let me be precise about what’s new:

What improved: Fee-related earnings growing faster (+18% LTM), insurance assets growing to $180 billion post-Just Group, BN/BNT combination announced (structural simplification = potential discount narrowing), $67 billion raised year-to-date already with a seventh PE fund in the works, management actively buying back shares at what they call a 40% discount.

What’s the same: The complexity discount is still there. Real estate distributions from BPG are softer. The stock hasn’t re-rated toward peers.

What’s slightly weaker: BAM’s share price declined ~16% in Q1 (from $52 to $44), reducing the blended intrinsic value per BN share from $68 to $66. This is mark-to-market noise on a publicly traded holding, not a deterioration in the underlying business.

5. The Structural Catalyst: BN + BNT Combination

This is the one genuinely new development worth examining carefully.

The proposed combination merges BN (the investment firm) with BNT (the Brookfield Wealth Solutions vehicle). The stated rationale: give the insurance business access to ~$145 billion of additional permanent capital sitting in BN’s balance sheet. This is the same logic that makes Berkshire Hathaway’s structure so powerful insurance float invested in a diversified pool of high-quality assets.

If approved at the July 16 shareholder meetings, the combined entity will trade under “BN” on NYSE and TSX. The company will also adopt US GAAP from Q1 2027, making it directly comparable to US-listed peers like Blackstone, KKR, and Apollo. That matters for valuation: if you’re running on different accounting standards, many institutional investors run you through a different (often lower-multiple) lens. Switching to US GAAP removes that friction.

Both changes simplification and US GAAP adoption are catalysts for multiple expansion that didn’t exist six months ago.

6. Risks (Still Real)

Nothing has changed structurally on the risk side, but a few deserve updated color:

Complexity discount: The BN/BNT combination and potential simplification of infrastructure/energy vehicles are explicitly designed to address this. Progress, but not resolved yet.

Real estate drag: BPG distributions were down significantly YoY ($642M LTM vs. $904M prior). Management characterizes this as timing and disposition-related, not fundamental deterioration 96% occupancy and improving lease economics support that view. But it’s worth watching.

Private credit sentiment: The shareholder letter addressed this directly. Market concerns about AI disruption of SaaS businesses have weighed on private credit broadly. Brookfield’s management explicitly states they have no material software exposure in their credit book, with the portfolio focused on real asset credit and opportunistic lending. Oaktree’s track record through cycles is the relevant benchmark here.

Capital deployment: $188 billion to deploy is a lot. Getting it wrong matters. The track record says they don’t $17 billion in Q1 asset sales, substantially all at or above carrying values, is reassuring but it’s a genuine risk at this scale.

7. The Updated Verdict

The Q1 2026 results don’t change the thesis they reinforce it.

The asset management business is growing faster than peers on a fee earnings basis. The insurance business just scaled to $180 billion with the Just Group acquisition. Operating businesses are stable. Management is aggressively repurchasing shares at a 40% discount. And for the first time, there are concrete structural catalysts (BN/BNT combination, US GAAP adoption) that could close some of the discount.

At $44/share, you’re paying:

~17x recurring earnings (peers at 22–25x)

~38% discount to blended intrinsic value ($66.37)

5.2% yield on recurring DE alone

The five-year return math is essentially unchanged from my prior piece: 12–15% DE growth + 0.6% dividend yield + ~2% buyback yield + potential multiple expansion from structural simplification = 15–18% CAGR scenario if things go right.

If you owned it at $47 per my last piece: the thesis is intact, the price is better, and you now have two concrete catalysts you didn’t have before. Add on weakness.

If you’re new: this is one of the more compelling setups in large-cap financials right now. The complexity that keeps most investors away is a feature, not a bug it’s precisely why the discount exists. The business itself is not complicated. It collects fees, earns spreads on insurance float, and owns world-class real assets. It does all three simultaneously, at scale, with a 30-year track record.

The Portfolio Update

Here is a look at my complete portfolio. As an investor, I am extremely concentrated by design.

I’ll be the first to admit it: I have significantly underperformed the S&P 500 since the start of 2026 (lagging 5%). Our two flagship holdings, Kinsale Capital and VusionGroup, have been absolutely torn apart by the market recently.

With this latest update, Brookfield now moves into the #3 spot in the portfolio by value. It sits just behind S&P Global (SPGI) which is my most recently added position and VusionGroup, a line where I continue to accumulate more and more shares with Kinsale and Apollo.

I am staying the course. I know the fundamental power of these companies and their long-term potential. I’d much rather be patient with high-quality businesses I understand than reckless by chasing the latest “trend” stocks trading at 35x earnings.

As always i’m updating the PDF, this time with a special offer, the report is a full equity deep-dive on Brookfield Corporation, updated with Q1 2026 results. It covers the investment thesis, a plain-English breakdown of how the Brookfield ecosystem works insurance float, asset management fees, and direct asset ownership and the key financial data: segment earnings, peer valuation comparisons, and scenario analysis from bull to stress case.