One Position Instead of Two: The Moat Upgrade

Why I swapped Kinsale and Apollo for Mastercard

A few weeks ago I made a portfolio decision that felt uncomfortable in the moment, which is usually a sign you’re doing something right. I closed two positions Kinsale Capital at a loss, and Apollo Global Management at a profit and put the proceeds into Mastercard. Let me explain why, because the logic matters more than the outcome.

Kinsale and APO are genuinely good businesses. Kinsale is a focused E&S insurance underwriter with a phenomenal track record; Apollo is one of the sharpest alternative asset managers on the planet. But both were being underwritten on the same basic assumption: 15–20% EPS CAGR over the next five years. And when I stress-tested that assumption, cracks appeared. Kinsale needs to avoid a bad underwriting cycle. Apollo needs credit markets to stay cooperative. These aren’t fatal flaws, they’re just the nature of businesses where the moat is more about execution than about structure.

On top of that, I already hold Brookfield Corporation which, if you squint, is playing a very similar game to Apollo: alternative assets, private credit, fee-earning AUM growth. Owning both was redundant. I was essentially doubling down on the same thesis, in the same sector, with correlated risk, without realizing it. That’s the kind of portfolio overlap that feels fine until the credit cycle turns and both positions move the same way at the same time.

So the question became: if I’m going to free up capital anyway, where does it go? And when I looked across the portfolio and asked where Mastercard fit by comparison, the answer was uncomfortable, I was taking on more execution risk and more sector concentration for the same expected return. Capital allocation isn’t just about picking good companies, it’s about ranking them. If you can own the global highway toll booth for roughly the same projected EPS growth as a regional insurer and a credit-cycle-dependent asset manager you’re already partially exposed to through BN, the honest move is to consolidate into the one with the near-indestructible structural advantage. Moat quality isn’t even in the same conversation, and over a 5-year hold, moat quality is basically everything.

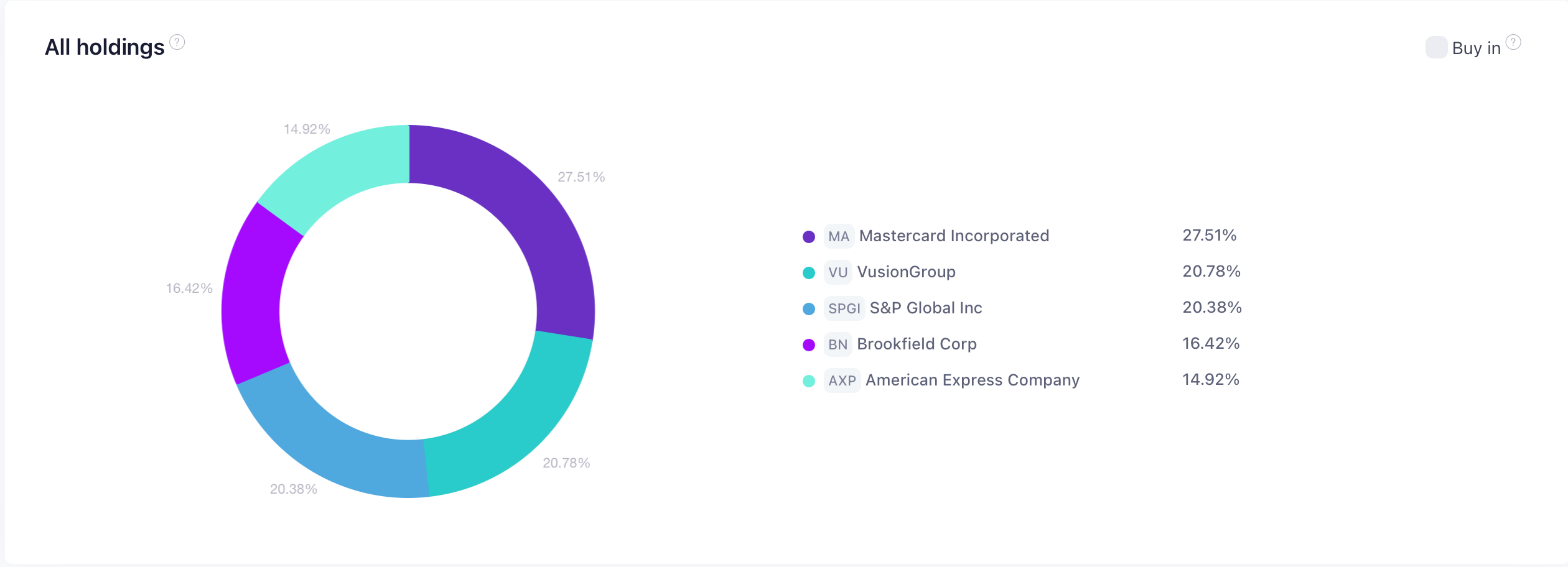

With Vusion exploding in the last weeks we’re stile behind, but Portfolio is behind the S&P 500 only by 3,4% since the beginning of the year compared to -8% at the previous update. I still believe we’re going to underperform this year, SPGI is consolidated the business and MA is a new add. Earnings season will be key here. I’m investing for the long term and I know some years I’m gonna underperform, and this is one of those years.

1. The Machine

You already know what Mastercard does, so I’ll skip the basics and go straight to the investment case.

The moat here is a three-headed animal network effects (accepted everywhere because everyone has one), switching costs (banks embedded in the rails don’t leave), and regulatory licensing (operating permissions in virtually every country on earth, which took 60 years to accumulate). None of those erode quickly. None of them can be replicated with capital alone.

What makes it special as a compounder is the asset-light model. No factories, no inventory, minimal physical infrastructure. Return on invested capital runs above 30–40%, and the company reinvests some of that at high rates into new geographies, fraud AI, and tokenization, then returns the rest through aggressive buybacks. It compounds and cannibalizes simultaneously a rare combination.

The risks worth taking seriously: regulatory pressure on interchange fees is structural and never fully goes away. The stablecoin question is real over a 10-year horizon, even if it’s noise over 5. And the CFO change, while internal, adds short-term uncertainty during a period when Mastercard is actively pivoting its capital allocation toward digital assets. None of these are thesis-breakers. All of them are worth monitoring.

2. The Numbers

Current Valuation

Price at time of writing is around $483

Profitability Snapshot

Revenue (TTM): ~$33.9B, growing ~16% year-over-year

Net income (TTM): ~$15.9B

Operating margin: ~58%, one of the highest in the S&P 500, and still slowly expanding

2026E EPS: $19.60 (consensus)

Valuation Metrics

P/E (on 2026E EPS): ~24.6x

Historical P/E range: Low ~24x (2016) - High ~55x (2020)

10Y avg ~37.5x

5Y avg ~36.5x

Those were in the low interest rates world, and I do not believe we’re going to see MA at 37x in the near/medium term.

Earnings yield: ~4.1% (= $19.60 / $483) : for the first time in a long time, this is actually competitive with what you’re comparing it to:

10Y US Treasury: ~4.4% → minimal premium for owning a business growing 15%+ annually. That gap should not exist.

S&P 500 earnings yield: ~4.1% → Mastercard is trading at essentially the same earnings yield as the broader index, despite being a structurally superior business with a higher growth rate. That’s the anomaly.

Shareholder Returns

In 2024, Mastercard returned $13.4B to shareholders, $11B in buybacks, $2.4B in dividends, against $14.8B in operating cash flows. Essentially the entire free cash flow handed back to owners.

Dividend yield: ~0.6%, Buyback yield: ~2.5%

Share count shrinks roughly 2% per year from buybacks, a silent EPS booster most people underweight.

3. The Napkin Math

A. EPS Growth

Revenue growth: ~13% annually (conservative vs. recent 16% prints)

Margin expansion: ~0.5% per year

Share count reduction: ~2% per year (buybacks)

Total EPS growth estimate: ~14–15% annually

B. Valuation Impact

Current forward P/E: ~24.6x | 10-year avg: ~37.5x | 5-year avg: ~36.5x

Scenario 1 : Partial reversion to 30x: (30/24.6)^(1/5) − 1 = +4.1% per year tailwind

Scenario 2 : Multiple stays flat: 0% impact

Scenario 3 : Compresses to 21x: (21/24.6)^(1/5) − 1 = −3% per year drag

D. The Final Equation

Bull case: 15% EPS growth + 0.6% dividend + 4% multiple expansion = ~20% annually

Base case: 15% EPS growth + 0.6% dividend = ~16% annually

Bear case: 12% EPS growth + 0.6% dividend − 3% multiple drag = ~10% annually

Even the bear case competes with the S&P 500’s historical 10% average. The base case is 8 points of annual outperformance. And this is the core of the Kinsale/Apollo swap logic made numerical: I’m targeting the same EPS growth I was underwriting in those two positions, but now with a structural moat that makes the bear case feel survivable and the base case feel genuinely attractive.

4. My Proprietary Insight

On a forward earnings basis, Mastercard is sitting in territory it has occupied only once in the past decade, 2016, right before a multi-year re-rating. The current 34% discount to its own 10-year average P/E is not explained by deteriorating fundamentals. Revenue is accelerating. Margins are expanding. Buybacks are running hot. What’s changed is the narrative, not the business.

The part of the narrative I think is most mispriced: the stablecoin threat is being used as a discount on a company that is actively building the stablecoin infrastructure itself. Mastercard has already announced plans to expand settlement capabilities to include stablecoin options for issuers and acquirers. This is not a Kodak moment, it’s more like Kodak deciding to invent the iPhone. The market is applying a disruption discount to the company most likely to be on the right side of the disruption.

The second hidden angle is the services revenue mix shift. Most of the market still prices Mastercard as a pure transaction volume business, volume times rate. But value-added services (fraud detection, analytics, tokenization, AI consulting) grew 22% year-over-year in Q1 2026, well ahead of the 16% overall revenue growth. As that mix increases, the multiple on the business should structurally expand, not compress, that revenue stream is stickier, less regulated, and less cyclical than raw interchange. The market hasn’t priced that transition yet, which means you’re getting a business getting better priced as if it’s getting worse.

5. My Take

Sleep Well at Night Score: 8/10

What Excites Me

The earnings yield at 4.1% now matches the S&P 500 and nearly matches Treasuries, for a business growing EPS at 15%+ annually. That math doesn’t stay broken for long.

The services mix shift is a free call option on multiple expansion that isn’t in the consensus story.

On a forward P/E basis this is the cheapest Mastercard has been in a decade, driven by noise rather than any fundamental deterioration.

What Worries Me

Regulatory risk on interchange fees is permanent. One bad EU ruling and the revenue model takes a structural haircut.

The CFO transition during a critical strategic pivot (stablecoins, digital assets, agentic commerce) is the kind of timing that creates execution risk even when the transition itself is well-managed.

If EPS growth disappoints, say slows to 8–10% due to macro headwinds, the earnings yield argument evaporates and there’s limited valuation support from dividends alone.