MOODY'S (MCO): The Waver Analysis

🔓 FREE EDITION — Normally reserved for paid subscribers. Enjoy it, and consider upgrading below.

Waver Research drops deep-dive equity analyses every week. This one’s on us. If you want the full toolkit napkin math on 2-3 companies per month, our proprietary watchlist, and our portfolio framework.

become a paid subscriber. The price of one coffee per week.

Your future self will thank you.

0. THE STORY

The Genesis. Moody’s was founded in 1900 yes, before the Federal Reserve even existed by John Moody, who had a simple but powerful idea: what if someone just told you how risky a bond was before you bought it? That idea turned into a 125-year-old oligopoly. Today, Moody’s is one of only three credit rating agencies that the world’s financial system genuinely trusts (the others being S&P Global and Fitch). Every time a government, a bank, or a corporation wants to borrow money from the public bond markets, they almost always need a Moody’s stamp. That stamp costs money. And since there are only three players who can give it, the pricing power is extraordinary.

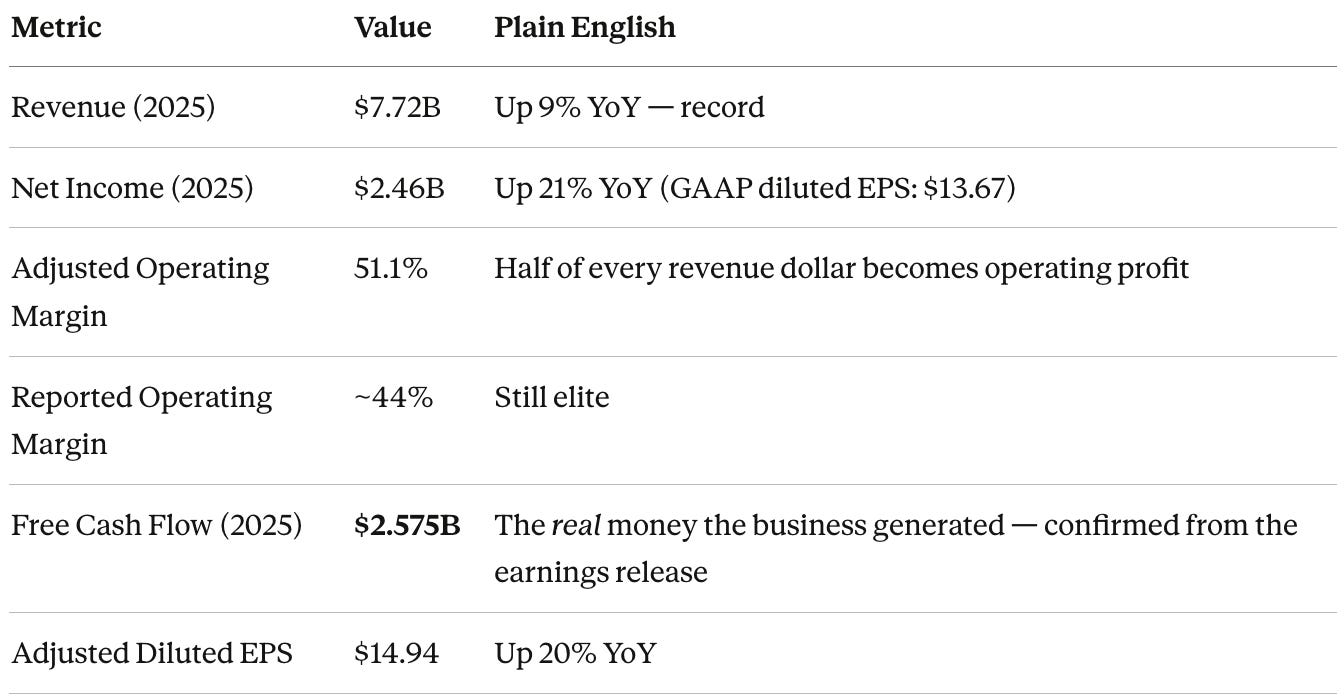

The Current Drama. Two days ago (February 18, 2026), Moody’s just dropped what management called “a record year” $7.7 billion in revenue, up 9%, with adjusted operating margins expanding to a stunning 51.1%. EPS grew 21%. But the stock is still sitting roughly 19% below its 52-week high. Why? The market has been spooked by AI disruption fears: could large language models eventually replace the need for professional credit analysts? It’s a legitimate question and it’s been dragging the entire data & analytics sector lower. The stock jumped ~6% on earnings day, but is still deeply in the doghouse compared to where it was.

Why This Matters. Moody’s just posted record results, beat estimates, raised guidance, and still trades below its historical average P/E. That’s the kind of setup that gets Waver Research attention. Let’s dig in.

1. THE MACHINE

The Simple Explanation

Imagine you’re lending money to a stranger. Before you hand over your cash, you want someone credible to tell you: “Is this person good for it? And if not, how bad could it get?” Moody’s is that credible someone, but for the entire global bond market. Every year, roughly $6.6 trillion in new debt gets issued around the world (bonds from companies, governments, banks). Most of those bond issuers need a Moody’s credit rating to access capital markets. The issuers pay Moody’s to get rated. That’s the ratings business (called MIS — Moody’s Investors Service). Then, separately, banks, insurers, and corporations pay Moody’s subscription fees to access data, analytics, and risk tools that’s the analytics business (called MA : Moody’s Analytics). One side is tied to bond market activity; the other is a predictable, recurring SaaS-like revenue stream. Together, they’re a beautiful flywheel.

The Moat : Why It’s Almost Impossible to Kill

This is where Moody’s gets genuinely special. Four layers of protection, stacked on top of each other:

1. Regulatory moat (the biggest one nobody talks about). The SEC has designated only a handful of firms as “Nationally Recognized Statistical Rating Organizations” (NRSROs). Moody’s is one of them. You can’t just wake up tomorrow and start competing with Moody’s regulators won’t let you. This is the equivalent of a government-issued license to print money. Globally, similar frameworks exist. The barriers to entry are not just financial they are legal and regulatory.

2. Network effects & trust accumulation. Credit ratings derive their value from trust. Moody’s has been building that trust for 125 years. Every pension fund, every sovereign wealth fund, every bank’s internal credit committee, they all reference Moody’s ratings. A new entrant can’t buy 125 years of credibility. Even after the 2008 financial crisis when Moody’s was famously criticized for handing out AAA ratings to toxic mortgage securities — the business model survived intact. That tells you everything about the stickiness of this oligopoly.

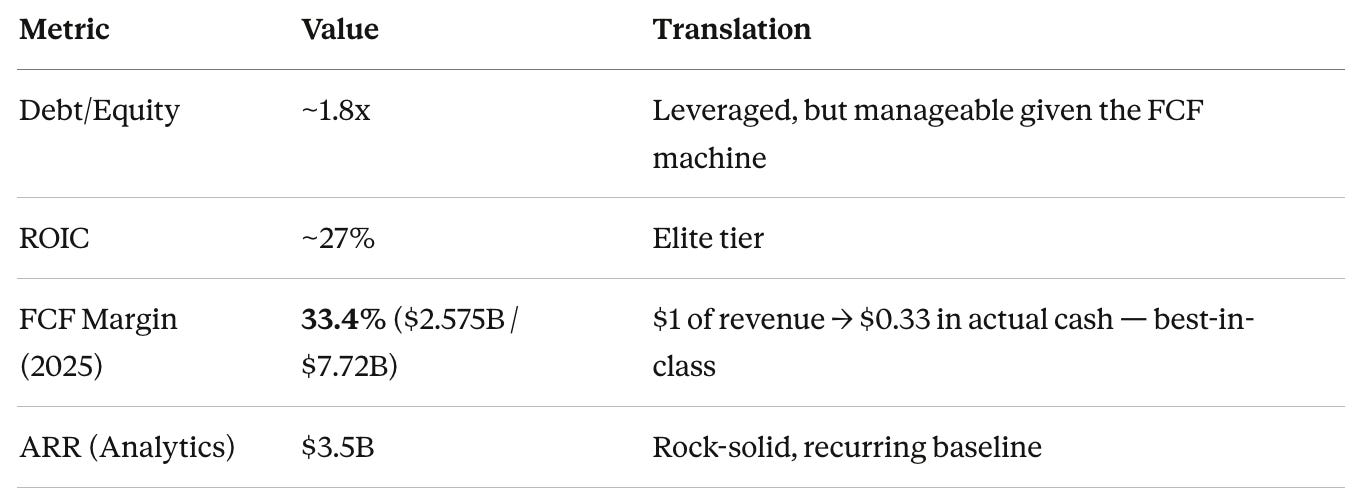

3. Switching costs on the Analytics side. Moody’s Analytics has embedded itself into the core workflows of financial institutions. Banks use their models for stress testing. Insurers use their risk tools for underwriting. Once those systems are integrated into internal processes and regulatory reporting, ripping them out is prohibitively expensive and operationally risky. Annual recurring revenue (ARR) hit $3.5 billion in 2025, with retention rates in the “low-to-mid 90s percent.” That is not customer loyalty. That is a golden cage.

4. Data flywheel. Moody’s has been collecting credit data on companies, bonds, and sovereigns for over a century. That dataset is proprietary, validated, and growing every day. It’s what makes their AI tools credible. In 2025, they rated $6.6 trillion in debt generating even more data. The more data they have, the better the models. The better the models, the stickier the customers. Rinse, repeat.

The ROIC Story : Is This a Compounder?

ROIC stands for Return on Invested Capital essentially, “for every dollar the business has deployed, how much profit does it generate?” Anything above 15% is excellent. Above 25% is elite.

Moody’s ROIC: ~27%. That’s elite. What’s even more impressive is the operating margin: 44% on a reported basis, and 51% on an adjusted basis. For context, most S&P 500 companies have operating margins around 12-15%. Moody’s is running at three to four times that level. This is what a true “capital-light” business looks like — once the brand and the regulatory status are established, every incremental dollar of revenue flows almost entirely to the bottom line. Moody’s doesn’t need billion-dollar factories or massive R&D budgets to grow. They mostly need smart people and servers.

The company is a hybrid: it compounds through the analytics business (reinvesting in data, AI, new products) and returns cash through the ratings business (buybacks and dividends). In 2026, management plans to return at least 90% of free cash flow to shareholders including $2 billion in buybacks and a 10% dividend increase. That’s a company firing on all cylinders.

The Risks — What Could Blow This Up?

AI disruption : the #1 fear right now. The market is legitimately worried that LLMs could automate credit analysis, reducing the need for Moody’s human analysts and eventually its data products. This fear is real but likely overstated for the ratings business you can’t replace a legally recognized credit rating with a ChatGPT output. For the analytics side, it cuts both ways: AI could commoditize some products, but Moody’s is using AI to build new, stickier products faster. Their customers who use AI-enabled solutions are retained at a 97% rate. They seem to be adapting, not disrupting.

Credit cycle risk. The MIS ratings segment is cyclical it depends on how much new debt is issued globally. In a recession, companies and governments borrow less, issuance drops, and Moody’s ratings revenue takes a hit. The 2008-2009 crisis saw revenue fall significantly. This is a real cyclical lever, though the growing Analytics segment provides a natural hedge.

Regulatory & reputational risk. Moody’s was at the center of the 2008 financial crisis controversy. Regulators globally are always watching. Any new scandal around ratings quality, ESG greenwashing certifications, or AI-driven tools could trigger congressional investigations or new rules limiting how ratings agencies operate or how much they can charge.

Concentration risk. Three agencies control essentially 100% of a critical global market. Regulators have historically debated whether this is healthy. The EU has periodically flirted with creating a European public ratings agency. If regulation ever forces the oligopoly open, the pricing power degrades fast.

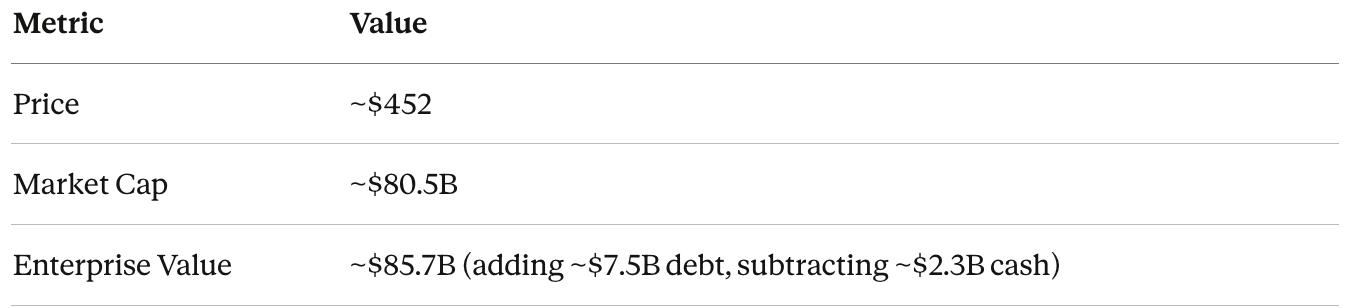

2. THE NUMBERS

Current Valuation

Profitability Snapshot

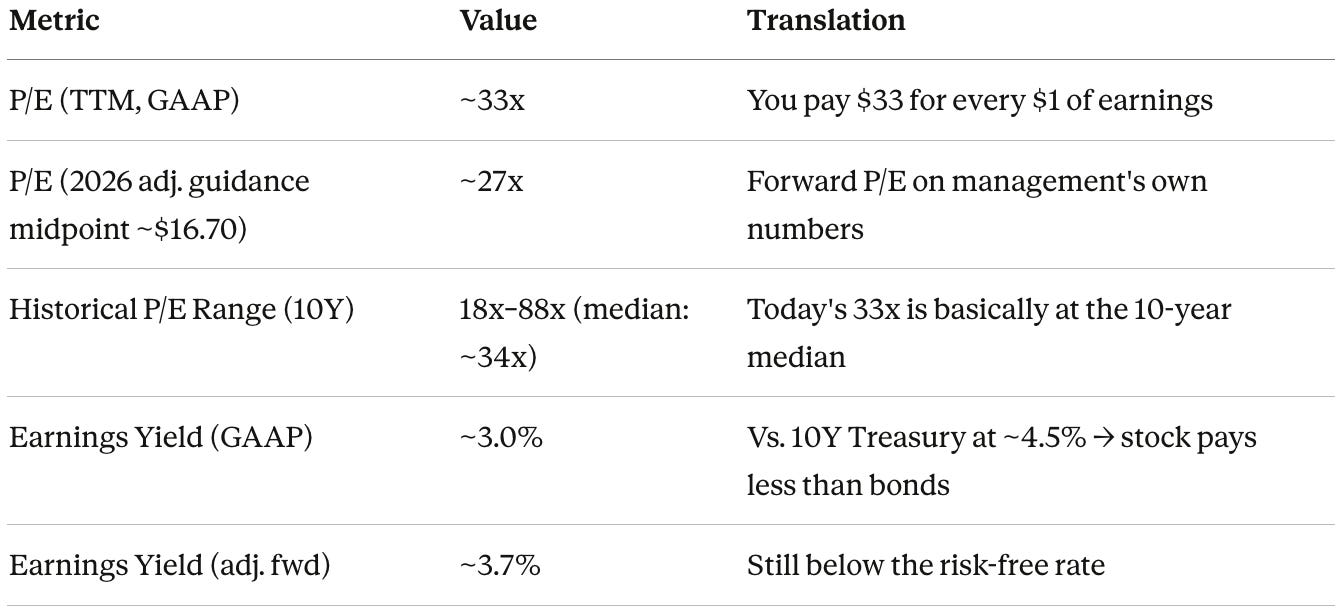

Valuation Metrics

Shareholder Returns

Quality Indicators

3. THE NAPKIN MATH

The Waver 5-Year Forward Return Projection

A. Growth Driver (EPS)

Using management’s own 2026 guidance as a starting point ($16.40–$17.00, ~12% growth at midpoint), and applying a conservative 10% EPS growth annually for years 2–5 (slight deceleration from recent 20%+ growth, accounting for the cyclicality):

Revenue Growth: ~8–9%/year

Margin Expansion: +150 bps per year (management guiding this explicitly)

Total EPS Growth Estimate: ~9% per year (conservative, organic only)

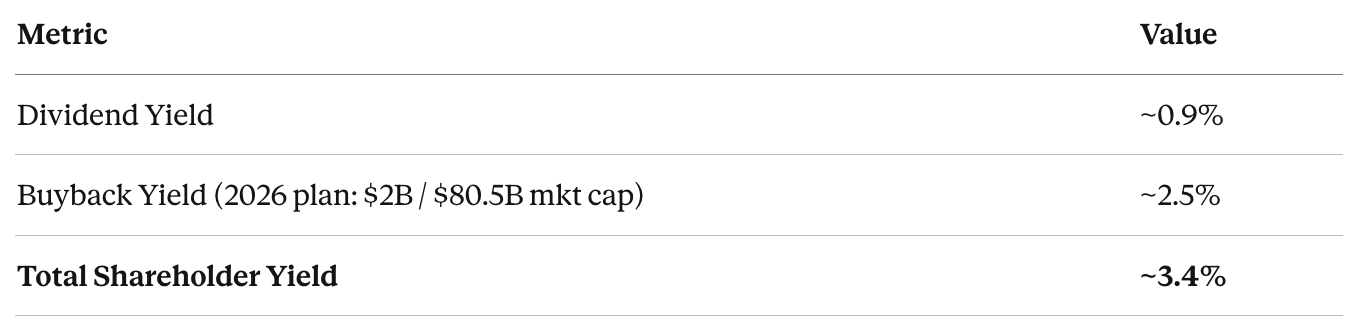

B. Shareholder Yield

Dividend Yield: ~0.9%

Buyback Yield: ~2.5% ($2B plan / $80.5B mkt cap)

Total Yield: ~3.4%

C. Valuation Impact (Multiple)

Current P/E: ~33x

10-Year Historical Median P/E: ~34x

Assessment: Trading at median. No significant drag or boost expected. ~0% annual multiple impact.

This is actually a key insight: unlike growth stocks trading at 50-60x where valuation compression is a death sentence for returns, Moody’s current multiple is essentially “priced fair” vs. its own history.

D. The Final Equation

The napkin math says Moody’s at ~$450 offers a reasonable low-teens annual return over 5 years assuming no major macro blow-up and that the business continues compounding as it has. Not a screaming bargain, but genuinely attractive for a quality compounder.

And keep in mind that this is with conservative EPS growth of 10%, management target 12% at midpoint for 2026, therefore you’re looking for 14-16%

4. MY PROPRIETARY INSIGHT

The Thing Nobody Is Talking About: The Stablecoin Play

Everyone is debating whether AI will kill Moody’s. Meanwhile, Moody’s just quietly positioned itself as the de facto ratings agency for digital finance.

In December 2025, Moody’s issued a request for comment on a cross-sector stablecoin rating methodology essentially, they want to be the agency that tells the world how safe a stablecoin is. CEO Fauber said management believes stablecoins could reach $400 billion in total value by end-2026 and $2 trillion by 2028. If Moody’s becomes the trusted credibility layer for digital assets the same way they are for traditional bonds that’s an entirely new market appearing from nothing.

Think about it: every institutional investor who wants to hold stablecoins, every corporate treasury, every bank getting into digital assets they will need a Moody’s-equivalent opinion before they deploy capital. The regulatory framework is still being built, and Moody’s is actively shaping it. This is the same playbook they ran in 1900 when they pioneered bond ratings for railroad companies. They’re running it again for the next financial infrastructure cycle.

This is not priced in. Most analyst reports don’t mention it. It’s the kind of optionality that doesn’t show up in a DCF model but it’s exactly the type of option that 10-baggers are made of.

The “AI Fear” Is Backwards

The market’s AI fear is that LLMs will eliminate the need for credit analysis. But here’s the contrarian take: AI needs trusted data to function. Banks, insurers, and regulators won’t plug raw web data into their credit models. They need structured, validated, legally-recognized data which is exactly what Moody’s has been building for 125 years. AI doesn’t kill Moody’s. AI amplifies Moody’s. Their data becomes the training ground for financial AI tools, not the thing getting disrupted.

Evidence: Customers using Moody’s AI-enabled solutions are retained at a 97% rate and are growing at twice the pace of regular accounts. That’s a company winning the AI transition, not losing it.

Historical Pattern: When MCO Dips Below 35x P/E

Over the past 10 years, the three prior instances when MCO traded meaningfully below its median P/E of ~34x (2016, 2018-2019, 2022), the stock delivered 40–60% returns over the subsequent 18–24 months as earnings caught up and sentiment recovered. We’re back in similar territory today trading at ~33x, below the 10-year median, after a ~19% drawdown. History rhymes; it doesn’t guarantee.

5. MY TAKE

😴 Sleep Score: 8/10

This is a Berkshire Hathaway-quality business (literally Berkshire owned Moody’s for years after the financial crisis and made a killing). The combination of regulatory moat, recurring revenue, and elite margins makes this one of the more defensible businesses on the planet. The only thing keeping it from a 9 or 10 is the debt load and the cyclicality of the ratings business.

🐂 What Excites Me

The moat is legally enforced. You can’t build a competitor to Moody’s without the SEC blessing you. That’s rare.

The analytics business is a stealth SaaS compounder. 97% ARR, double-digit recurring revenue growth, expanding margins — and most people still think of Moody’s as a “bond ratings” company from the 1980s.

The stablecoin optionality is essentially free. It’s not priced in, most analysts ignore it, and the TAM is enormous if digital assets go mainstream.

🐻 What Worries Me

The debt load is real. $7.5B in debt vs. $2.3B in cash. If rates stay high and a credit cycle downturn hits simultaneously, this gets uncomfortable fast.

The 2008 ghost. Moody’s was burned once by being too close to the products they rate. Private credit is exploding right now (+60% in MIS revenue in 2025). If the private credit bubble bursts, the reputational and financial damage could be significant.

AI commoditization of analytics is a slow bleed risk. It probably won’t kill the business, but over 5–10 years, some subscription revenue could erode if AI tools become genuinely good enough to replicate parts of what Moody’s Analytics does.

The One-Liner

“The world’s financial infrastructure needs a credit referee and there are only three licensed to do the job. This one is trading at median historical valuations, firing on all cylinders, and quietly building the future of risk assessment while everyone argues about AI. Not cheap, but rare quality at a fair price.”

🔒 Enjoying This?

This deep-dive is normally paid-subscriber only content at Waver Capital. You got lucky — we made this one free.

Every week, paid subscribers get:

2–3 full Waver Analyses like this one (with proprietary insights, napkin math, and the takes nobody else is writing)

Our live watchlist — the 15 names we’re tracking with price triggers

Monthly portfolio framework updates — how we’re sizing positions in different macro environments

Direct access to ask questions on any analysis

The price? Less than one coffee per week.

If you learned something today — about Moody’s, about how to think about a regulatory moat, about the stablecoin angle nobody’s pricing in — then you know what the paid content looks like.

→ Upgrade to Paid — Join the Waver Community

See you next week. 👋