Burford Capital (BUR) : Why I Never Touch This Stock

A great analysis can end with a hard pass. Here's exactly why Burford Capital, despite its genuine strengths fails my personal investing framework.

0. THE STORY

The Genesis. Two lawyers looked at the $400+ billion spent on litigation globally every year and spotted a broken market: companies with legitimate legal claims were either settling too cheap or walking away entirely because lawsuits are expensive and outcomes uncertain. Burford Capital, founded in 2009, essentially invented institutional litigation finance you have a strong legal claim but can’t afford the fight? We fund it, take the risk, and share the proceeds when you win.

The Current Drama. Burford just reported a weak FY2025, with revenue down 17% from record 2024 levels despite the underlying portfolio growing 20% and new commitments jumping 39%. The earnings drop was almost entirely accounting noise fair-value adjustments on ongoing cases not actual losses. Meanwhile, a $16 billion judgment against the Argentine government is sitting at the US Court of Appeals, where the panel has publicly signaled skepticism. The stock is down 45% from its 52-week high and trading below book value.

Why This Matters. The bull case on Burford is coherent, the moat is real, and the valuation looks cheap on paper. This analysis exists to work through all of it honestly and to explain why, at the end of a genuinely compelling story, the framework still says pass.

1. THE MACHINE

The Simple Explanation. Think of Burford as a venture capital firm for lawsuits. A corporation has a legitimate $500M breach-of-contract claim but paying lawyers for years is expensive and distracting. Burford writes the check covering all legal costs in exchange for a cut of the eventual settlement or judgment. They only win if the case wins. No interest income, no monthly payments. Pure risk-for-reward investing in the outcomes of commercial disputes. The twist: these returns are almost completely uncorrelated to the stock market. When the economy tanks, companies sue each other more, not less.

The Moat. Burford’s moat is real and has three layers. First, proprietary data: fifteen years of private case outcomes thousands of settlements that never become public is a genuine informational edge no competitor can replicate. Second, capital access: as the only NYSE-listed litigation finance firm, Burford can tap public debt markets at a scale and cost that private competitors like Longford or Therium simply cannot match their July 2025 $500M notes issuance at 7.5% is an option no private rival even has on the table. Third, relationships: they work with 90 of the world’s 100 largest law firms, a distribution network built over a decade that no new entrant can shortcut. These are genuine structural advantages. They’re just not enough, for reasons we’ll get to.

The ROIC Story. On concluded cases, Burford has historically generated 83–87% ROIC meaning they roughly double invested capital every two to three years on winning cases. Their annualized IRR across the portfolio has run at 27–30%. That is genuinely exceptional and puts them in the top tier of any asset class globally. The business is a compounder as long as it can keep redeploying capital at similar rates. The current portfolio stands at $3.9 billion in principal finance assets, growing 20% in FY2025. Even in a so-called “weak” year, the machine kept working. The problem isn’t the ROIC. It’s everything wrapped around it.

The Risks. Four risks, ranked by severity. First, a single US Appeals Court decision on the YPF case can impair 30–40% of market cap overnight a binary event entirely outside management’s control. Second, regulatory pressure from well-funded opponents is building simultaneously in the US, EU, and UK, targeting the very existence of third-party litigation finance. Third, interest coverage of 1.9x leaves almost no cushion in a business with inherently volatile annual cash flows. Fourth, fair-value accounting on an opaque portfolio creates persistent credibility questions a transparency problem that generates a structural valuation discount that may never fully close. Each of these risks gets its own filter below. None of them is theoretical.

2. THE NUMBERS

Current Valuation

Price (NYSE): ~$8.50

Market Cap: ~$1.9B

Enterprise Value: ~$3.3B (Market Cap + $2B debt − $621M cash)

Book Value per Share: ~$10.50 → stock trades at 0.80x book

Profitability Snapshot

Revenue (TTM): $466M down 17% from FY2024, despite portfolio growing 20%. This gap is the whole story.

Net Income (TTM): ~$87M GAAP; treat as directional only given fair-value swings

Operating Margin: ~57% structurally high; litigation finance has near-zero cost of goods sold

Note on FCF: free cash flow is nearly meaningless here the company recognizes revenue only when multi-year cases conclude, making cash generation episodic by design

Valuation Metrics

P/E Ratio: ~22x almost useless; use price-to-book instead

Historical P/Book Range (5Y): Low 0.7x (COVID panic) High 3.2x (2021 peak) — Avg: ~1.4x

Earnings Yield: ~4.7% on GAAP earnings

vs 10Y US Treasury: ~4.3% → the stock offers essentially no premium over risk-free on reported earnings

vs S&P 500 Earnings Yield: ~4.0% → marginal premium, not enough for this risk profile

Interpretation: on reported earnings yield, Burford barely clears the risk-free rate. The bull case requires trusting that normalized earnings are 2–3x the reported figure which may be right, but demands confidence in fair-value marks that have been publicly questioned

Shareholder Returns

Dividend Yield: ~0.7% a rounding error

Buyback Yield: ~0% no material repurchase program

Total Shareholder Yield: ~0.7% this is purely a capital gains story; there is no income floor whatsoever

Quality Indicators

Debt/Equity: 55% up from 36% five years ago; the trend is the wrong direction

Interest Coverage: 1.9x dangerously thin for a business with volatile annual cash flows; one slow year for case conclusions could push this below 1.3x

3. THE NAPKIN MATH

A. Growth Driver

Portfolio growth rate: ~15–20% annually (management targeting double by 2030, currently on pace)

Revenue growth on normalized basis: ~12–15% (conservative — assumes some case timing drag persists)

Margin: already near-peak at 57%; minimal expansion room

Share count: stable, no buyback program

Total EPS Growth Estimate: ~12–15% annually (normalized)

B. Shareholder Yield

Dividend Yield: 0.7%

Buyback Yield: 0%

Total: ~0.7%

C. Valuation Impact

Current P/Book: 0.80x

Historical Average P/Book (5Y): ~1.4x

Bull assumption: reversion to 1.4x over 5 years: (1.4/0.8)^(1/5) − 1 = +12% per year boost

Base assumption: partial reversion to 1.1x: +6% per year boost

Bear assumption: stays at 0.80x (regulatory overhang + YPF uncertainty persist): 0% contribution

D. The Final Equation

The base case looks genuinely attractive versus the S&P 500’s historical ~10%. The bull case is outstanding. But the stress scenario Second Circuit reverses YPF, regulatory noise increases, one slow case year produces near-zero returns for five years. That wide distribution, anchored by a binary legal event you cannot model, is the core problem. You’re not buying a compounder at a discount. You’re buying a compounder with a lottery ticket stapled to it. The question is whether you wanted the lottery ticket.

4. MY PROPRIETARY INSIGHT

Insight #1 — The “How Many Things Need to Go Right” Test

Here’s the framework I apply to every stock, and the one that Burford fails most visibly. Before buying anything, ask: how many independent conditions need to hold simultaneously for me to earn my expected return?

For a clean compounder a dominant consumer brand with pricing power and no debt the answer is two or three. The category doesn’t get disrupted. Management executes. Valuation stays reasonable. Done.

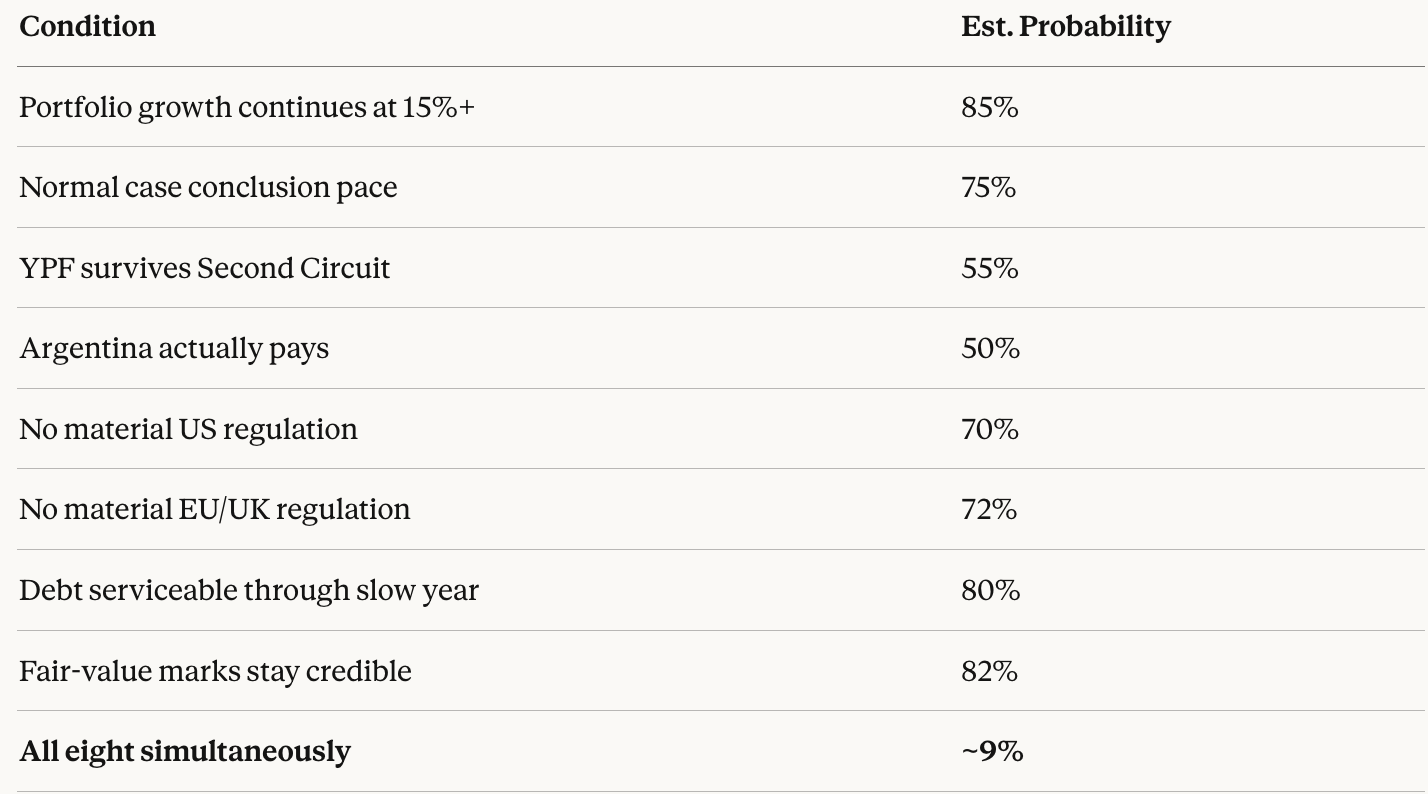

For Burford, count them: portfolio keeps growing at 15%+, case conclusions remain at a normal pace, YPF survives the Second Circuit appeal, Argentina actually pays if Burford wins, US Congress doesn’t pass restrictive legislation, EU and UK regulators don’t materially impair the TAM, debt remains serviceable through the next slow year, and fair-value marks maintain credibility with institutional investors. That’s eight conditions. Each individually plausible. Each partially outside management’s control.

Here’s the math most investors skip: if each condition has an 80% probability which is generous the probability of all eight holding simultaneously is 0.8⁸ = roughly 17%. The full bull case has about a one-in-six shot of fully materializing. This isn’t a reason to never own complex businesses. It’s a reason to demand a price that compensates for the complexity. And at 0.8x book, with the market already pricing in distress, there’s no additional discount left for the condition-stacking.

The insight to carry everywhere: the expected return of any investment isn’t just the upside scenario times its probability it’s all scenarios, probability-weighted, including the ones where three things go wrong in the same year. Burford is the kind of stock where that tail is fat, visible, and not fully compensated.

Filter #1: If I Can’t Model the Earnings, I Can’t Own the Stock

There’s a concept in investing called the “circle of competence” popularized by Buffett and Munger which most people interpret as industry knowledge. The deeper version is about predictability. Can you sketch out what this business will earn over the next three to five years with a defensible logic? Not perfectly. Roughly.

With Burford, that’s structurally impossible. Revenue is driven entirely by when lawsuits conclude. A single large case can represent $200–300M of revenue in any given year. Whether it shows up in 2025 or 2027 is not something management controls, analysts can model, or the company itself can guide on.

The accounting makes it worse. Burford marks its unresolved case portfolio to fair value every quarter up or down based on internal assessments of litigation progress. This means reported earnings contain large swings driven entirely by opinion, specifically the opinion of people whose compensation depends on those marks being favorable. This isn’t fraud. It’s the required accounting treatment for this asset class. But it means the income statement tells you almost nothing about actual cash generation in any given period.

The mental model worth keeping: Burford’s income statement is like a restaurant that only recognizes revenue when customers decide to pay their bill and customers can legally delay for years. The kitchen is busy. The food was served. But reported revenue depends entirely on when diners reach for their wallets. Revenue fell 17% in FY2025 while the underlying portfolio grew 20%. The business got better. The earnings got worse. That gap is not an anomaly it’s the permanent operating condition of this company. And when I can’t model the earnings, I can’t know if I’m getting a fair price. I’m guessing.

Filter #2: Binary Events Are Not Risks. They’re a Different Asset Class.

Every investment has risks. I’m not talking about risks. I’m talking about something more specific: a situation where a single external decision one management cannot influence, that you cannot hedge, and that resolves in binary fashion can permanently impair 30–50% of value overnight.

The YPF case is the textbook example. In 2012, Argentina nationalized YPF from Spanish energy giant Repsol. Minority shareholders sued, won a $16 billion judgment in US federal court, and Burford holds a large share of that claim. The US Court of Appeals panel has signaled they may reverse. If they do, Burford’s most valuable asset goes from “impaired but potentially enormous” to “gone.”

And even in a win scenario, you’re collecting from Argentina a sovereign government that has defaulted on its debt nine times, the most of any country on earth, and has been actively resisting this specific judgment for over a decade. Collection proceedings are running in eight jurisdictions simultaneously. Each one is its own binary event. Winning in one court doesn’t mean you see a dollar in the next five years.

The smart bull says: “strip YPF out and value the core business at 0.8x book.” Analytically reasonable. But the market cannot strip out YPF every news update moves the stock, pollutes the shareholder base with event-driven speculators rather than long-term holders, and distracts management from running the core portfolio. The moment you buy Burford, you’ve implicitly taken a position on Argentine sovereign law.

The question to ask yourself honestly: is that a bet you’ve actively chosen to make, or one you’ve accidentally inherited?

Filter #3: When Your Business Model Has a Political Target on Its Back

Every business operates within a regulatory environment. Most of the time, it’s stable background noise. But some businesses have motivated, well-funded opponents actively working to restrict them and litigation finance is the clearest example in public markets today.

Who loses money when Burford wins? Large corporations, their insurers, and defense-side law firms. These are some of the best-resourced lobbying interests in the United States and Europe. Their argument to legislators frames litigation finance as “lawsuit factories” and “foreign interference in US courts.” Some of this is legitimate. Most of it is motivated reasoning from parties who’d prefer plaintiffs to remain underfunded.

What matters for investors is the trajectory. In 2024 and 2025, the US Senate Judiciary Committee held hearings specifically on litigation finance disclosure requirements. The EU debated rules that could cap funder returns relative to claimants. The UK Law Commission recommended stronger oversight. Australia one of the most developed litigation finance markets globally already tightened its framework in ways that materially hurt Omni Bridgeway’s returns.

None of this has hit Burford yet. But the investing principle worth internalizing: regulatory risk is almost never priced until it’s too late to avoid. The market ignores it for years, then overweights it catastrophically when it arrives. And Burford, as the largest, most visible, most profitable target in the space, is the name that headlines will use the day anything passes. I don’t need to predict that regulation will happen. I just need to recognize it’s a real, growing, structurally motivated risk one being pushed by genuinely powerful opponents that currently is not reflected in a stock already pricing in operational distress.

Filter #4: Unpredictable Cash Flows Plus Thin Debt Coverage Is a Specific Kind of Trap

Interest coverage of 1.9x means for every dollar Burford owes in interest, they generate about $1.90 in operating profit. That sounds adequate until you remember earnings are violently unpredictable year-to-year by design. In a year where fewer cases conclude another “FY2025 type” year and operating income drops 30%, coverage dips below 1.3x. That’s when lenders ask uncomfortable questions and management shifts from offense to defense.

The debt trend makes this worse: total borrowings above $2 billion after the July 2025 $500M notes at 7.5%, with debt-to-equity climbing from 36% to 55% over five years. The company is borrowing to fund its case portfolio paying 7.5% continuously on capital that earns 83% ROIC episodically, only when cases conclude. The spread looks enormous on paper. In practice, you’re paying for the capital every quarter; you’re receiving the return unpredictably over three to five year periods.

The mental model: leverage is a multiplier, not a strategy. It multiplies the returns of a good business in good times. It multiplies the problems in bad ones. Unlike a bank, Burford has no regulatory backstop, no central bank window. If sentiment turns and they need liquidity fast, the options are expensive. The compounders worth owning don’t need to borrow to grow. They grow, then use the cash to fund the next phase. Burford is doing it in the other order and the trend is accelerating.

Filter #5: The Muddy Waters Scar and What It Really Tells You

In 2019, Muddy Waters published a 30-page report accusing Burford of misleading investors on ROIC metrics, related-party transactions, and accounting practices. The stock fell 50% in two days. Burford refuted the allegations vigorously. The core fraud claims were never proven. The stock recovered. Most investors today treat this as a closed chapter proof that the short was wrong and that patient holders were rewarded.

That’s one lesson. Here’s the one that gets missed. A sophisticated, well-resourced analyst with no prior position looked at Burford’s public disclosures documents management controls entirely and concluded they were designed to mislead. Whether that conclusion was right or wrong, it tells you something about the ambiguity of those disclosures. When smart, motivated people read your filings and still reach catastrophically wrong interpretations, you have a transparency problem regardless of intent.

Transparency problems create permanent valuation discounts in a specific way: not because investors expect fraud, but because uncertainty about what the numbers actually mean requires a margin of safety that clean businesses don’t need. Burford’s 5-year average P/Book is ~1.4x; pre-Muddy Waters it regularly traded above 2x. Part of that compression is permanent baked into how institutional investors discount the credibility risk on fair-value marks they cannot independently verify. That discount doesn’t close through operational performance alone. It closes through transparency improvements that, five years later, are still incomplete.

Life is short. There are businesses where I read the annual report and feel smarter. I’d rather own those.

5. MY TAKE

Sleep Well at Night Score: 5.5 / 10

Real moat, real track record, genuinely cheap relative to history. But the earnings unpredictability, the Argentine binary event, the regulatory trajectory, the thin debt cushion, and the lingering transparency discount combine into a specific kind of anxiety not “the business is deteriorating” anxiety, but “I cannot control the outcome” anxiety. That’s actually worse. At least deteriorating businesses give you something to analyze.

What Excites Me

0.80x book on a business generating 83% ROIC on concluded cases is objectively cheap versus any reasonable historical benchmark

Portfolio growing 20% annually while the stock sits near multi-year lows is a disconnect that eventually closes the question is just when and through what catalyst

YPF is a genuine free option priced near zero by the market if enforcement proceeds in even one major jurisdiction, the upside is transformative relative to the current share price

What Worries Me

The stress scenario : YPF reversal, one more slow year for case conclusions, and any regulatory headline produces near-zero returns for five years, and all three of those things could easily converge in the same 12-month window

Debt-to-equity trending up while interest coverage trends down, in a business that structurally cannot predict its own cash flow, is a combination that looks fine right up until it doesn’t

The transparency discount from 2019 may be permanent rather than temporary, which caps the multiple re-expansion that every bull scenario depends on as its primary return driver

The One-Liner

“World-class litigation machine trading at a genuine discount but when I count how many things need to go right simultaneously, I realize I’m not buying a compounder at a bargain. I’m buying a compounder with a lottery ticket stapled to it, priced as if the lottery ticket is already worthless. Maybe it is. But I never wanted to own the lottery ticket in the first place.”