ASML's Q1 Shines: Raking in €7.7 Billion While Gearing Up for the AI Boom!

Semiconductor Superstar Posts Strong Results, Keeps Eyes on €30-€35 Billion 2025 Target

While the world buzzes about AI changing everything, the folks making the super-advanced machines that make AI chips possible are busy printing money – literally, in the case of ASML's lithography machines! ASML just dropped its Q1 2025 results, showing they're cruising right along in the fast lane of the booming semiconductor industry.

The Q1 Scorecard: Big Sales, Healthy Profits & Those Lumpy Bookings

Let's get straight to the juicy numbers from the official report. ASML pulled in a cool €7.7 billion in total net sales for the quarter. That breaks down into €5.7 billion from selling their shiny new systems and another €2.0 billion from keeping their already installed machines humming along (Installed Base Management).

Profit-wise, they weren't messing around either. Net income landed at a very respectable €2.4 billion (that's €6.00 per share!). Their Gross Margin hit 54.0%, and the Operating Margin was a strong 35.4%, showing they're running a tight ship while delivering cutting-edge tech.

Now, about those future orders (the "bookings") that caused some chatter: ASML locked down €3.9 billion in new system bookings in Q1. Yes, that's less than the prior quarter, but let's be real – orders for these incredibly complex, multi-million-euro machines can be notoriously lumpy. One quarter might be huge, the next a bit quieter. The key takeaway is that demand for the absolute leading edge remains, with €1.2 billion of those Q1 bookings specifically for their top-tier EUV systems.

And even with the quarterly bookings bouncing around, let's not forget the mountain of orders ASML is already sitting on! News reports pegged their total backlog at the end of Q1 at a massive around €35 billion. That's like having a huge pipeline stuffed with future deliveries already lined up, giving them a hefty safety cushion even when new orders have a quieter quarter. It shows just how much demand there is for their tech waiting to be fulfilled!

What's Selling & Where's it Going?

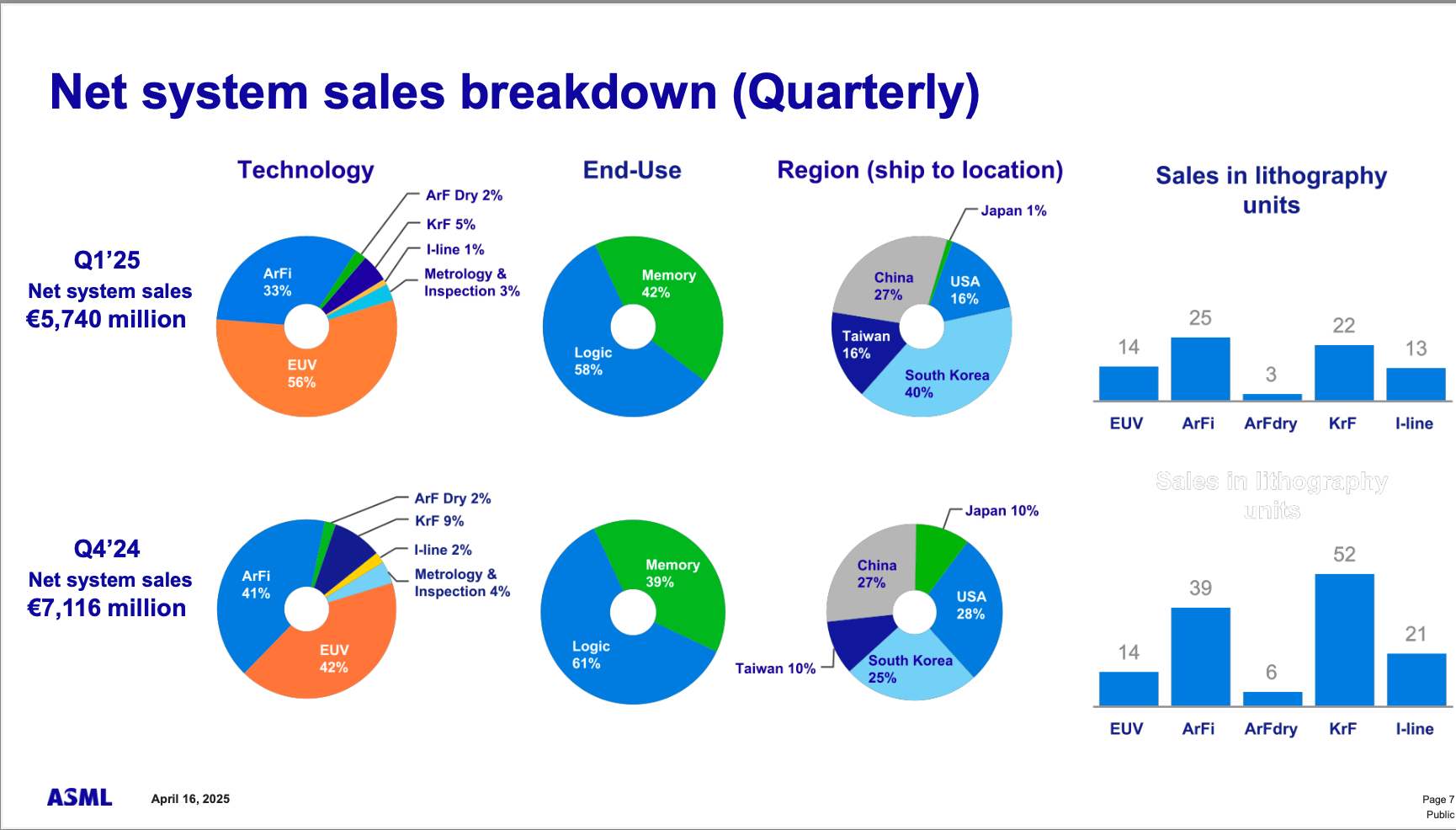

Digging into the system sales (€5.7 billion total), the star of the show continues to be Extreme Ultraviolet (EUV) lithography, making up 56% of the pie, followed by advanced immersion (ArFi) systems at 33%. This tech is essential for making the most powerful chips.

Who's buying? The demand is split between chipmakers focused on Logic (making brains for computers, phones, AI – 58% of system sales) and those focused on Memory (making storage – 42%). Geographically, the machines shipped out primarily to South Korea (40%), China (27%), the USA (16%), and Taiwan (16%) in Q1.

Looking Ahead: AI Fueling the Future & Navigating Global Shifts

ASML isn't planning on slowing down. Here's their outlook based on the presentation:

For Q2 2025: They expect net sales between €7.2 billion and €7.7 billion, with a gross margin between 50% and 53% (noting the wider margin range accounts for some tariff uncertainties).

For the Full Year 2025: ASML is sticking to its target of hitting total net sales somewhere between €30 billion and €35 billion, with a healthy gross margin between 51% and 53%.

Management commentary often highlights that the demand linked to Artificial Intelligence remains incredibly strong, acting as a major tailwind. They see the semiconductor industry roaring towards $1 trillion by 2030, largely fueled by AI needing ever more powerful and efficient chips. ASML firmly believes their advanced lithography tools are the key to enabling this future.

Interestingly, the shifting global landscape, with initiatives like the CHIPS acts in the US and Europe encouraging more regional semiconductor production, could actually create more demand for ASML's gear as new fabs are built out across different geographies. While geopolitical tensions and tariffs create uncertainty, the push for localized chip supply chains fundamentally relies on ASML's near-unique technology.

Sharing the Love (and Cash) with Shareholders

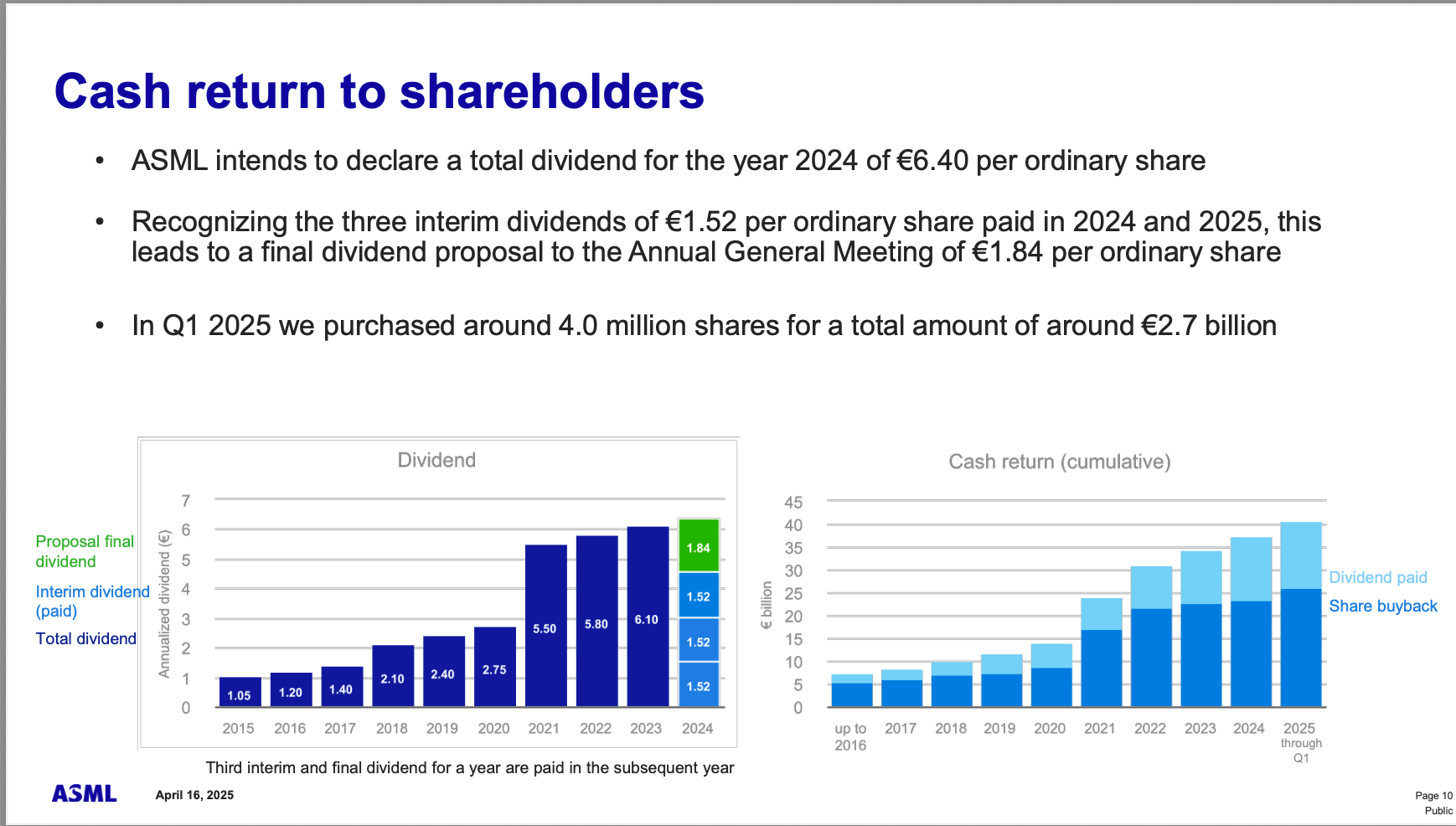

ASML is also keeping its shareholders happy. They bought back €2.7 billion worth of shares in Q1 alone. Plus, they're proposing a final dividend that brings the total payout for the 2024 financial year to €6.40 per share.

So, the takeaway? ASML had a strong start to 2025, is confidently navigating the path ahead, and remains absolutely central to the future of technology, especially with AI demanding ever-more powerful chips.

Annual General Meeting Recap

I’ve listened to it so you don’t have to, here’s the key ideas of this meeting :

Market and Outlook: AI is Our New Best Friend!

Hold onto your hats, because AI is blowing up the demand for the most sophisticated chips out there! This is fantastic news for ASML because building those tiny wonders means needing our super fancy machines – both the cutting-edge EUV ones and the trusty Deep UV workhorses.

The long-term forecast looks shinier than a polished wafer, with ASML still aiming for a massive €44 billion to €60 billion in revenue by 2030. Cha-ching!

Sure, there are a few storm clouds on the horizon (hello, geopolitics and tariffs!), adding a dash of uncertainty, but the core message is: the world needs more chips, and more chips mean more ASML!

For 2025, expect revenues somewhere between €30 billion and €35 billion. Not bad, right? And yes, AI is pretty much carrying the growth team on its shoulders this year.

Technology Updates: Behold Our Shiny Toys!

ASML isn't just sitting around; they're constantly upgrading their arsenal of chip-making magic:

Low NA EUV: Think of it as the already awesome tech just getting more awesome – faster, more precise, and cheaper per wafer. Like upgrading your sports car to the latest model!

High NA EUV: This is the next big thing! It's like a super-powered microscope that helps simplify those ridiculously tiny chip patterns. It promises cost savings and keeps ASML at the forefront of pushing physics to its limits. The first ones are already out the door!

Deep UV (DUV): Don't forget the workhorse! These machines still make a ton of chips. ASML is still pouring big bucks into DUV R&D, making them faster and better than ever, even tackling new areas like advanced packaging.

Multi-beam: This inspection tech is making great strides, helping customers check chips faster. It's finally getting its moment in the spotlight!

And to keep up with all this demand, ASML is building more factories and expanding like crazy all over the world – getting ready for the future chip party!

Capital Allocation: Making it Rain (Responsibly)!

Good news for shareholders! ASML is proposing a nice fat dividend of €6.40 per share for 2024 – a decent bump up from last year.

They've also been busy buying back their own shares, pouring €5 billion into that recently.

Shareholders gave the thumbs-up for ASML to have the flexibility to issue more shares if needed (like for buying other cool companies) and to continue buying back and cancelling shares in the future (up to 10% of the outstanding shares that’s HUGE). Keeping the financial options open!

Geopolitics and Competition: Navigating the Global Tango!

Tariffs: Ah, the dreaded 'T' word! The possibility of US tariffs adds complexity. ASML plans to pass on the direct cost (sorry, customers!), but the bigger worry is the indirect hit if tariffs slow down the whole global economy. They're also pointing out the irony that tariffs could make manufacturing more expensive in the US, not less, and are working to find ways around the hassle.

China Competition: Yes, China is definitely trying to develop its own chip tech, spurred on by restrictions. ASML acknowledges this but points out that building the entire complex ecosystem needed for advanced lithography is incredibly difficult and takes ages. So, while they're trying, ASML feels they still have a significant lead in the big leagues.

TSMC Reliance: ASML has a great relationship with the biggest chipmaker, TSMC, and their huge ramp-up in new tech will be a key driver. But ASML reassured everyone they work closely with all their major customers and their business isn't solely dependent on just one player.

DUV Rivals: Other companies are trying to muscle into the DUV market, but ASML is confident its continuous investment and proprietary tech give it a strong edge. Basically, they're saying, "We've got this!"

So, What's the Long-Term Story Here?

Alright, zooming out from the quarterly bumps and wiggles, ASML's Q1 performance basically reinforces the long-term picture. Sure, the €3.9 billion in bookings wasn't a record-smasher, but for a company selling machines worth hundreds of millions each, orders will always be lumpy. What matters is the trend, and the underlying demand driven by unstoppable forces like AI just isn't going away. ASML's tech is the non-negotiable ticket to that future.

They pulled in solid revenue (€7.7 billion) and showed excellent profitability (54% gross margin!), proving the business engine is humming nicely. Plus, that steady €2.0 billion from the Installed Base Management (keeping existing machines running) adds a lovely layer of predictability. Most importantly for the long view, management confidently stood by their ambitious 2025 goals (€30-€35 billion revenue) and even pointed towards those huge 2030 targets (€44-€60 billion!). When a company with this kind of technological moat talks confidently about the end of the decade, long-term investors tend to listen. Add in the continued share buybacks and dividends, and Q1 looks like another solid step on a very long, very promising road.

Love this? Level Up Your Investing!

Tuesdays (Free): Get market insights and tips delivered to your inbox.

Thursdays (Premium): Exclusive access to:

Earnings analysis

Portfolio insights

Bonus articles

Quarterly market reviews

Free copy of my book "Investing With Eagles".

Subscribe to Waver Premium for only 7.49$ per month for in-depth market knowledge and financial growth. that less than 2 Starbucks.

Disclaimer: Please remember, the thoughts expressed here are just opinions based on publicly available information like the Q1 2025 earnings report. This is not financial advice! Investing involves risks, and you should always do your own research and consider your personal financial situation before making any investment decisions. Talk to a qualified financial advisor if you need personalized advice.