Apollo Made a 5x Return on This Stock in 3 Years. Wall Street Still Hasn't Figured It Out

Evertec runs the financial plumbing of 26 countries, holds a Federal Reserve mandate, survived Hurricane Maria without a hiccup and trades at 13x earnings. Here's what the market is missing.

0. The Story

In September 2010, Apollo Global Management one of the world’s most sophisticated private equity firms paid $570 million to buy a 51% stake in an obscure Puerto Rican technology subsidiary from Banco Popular. The deal valued the joint venture at $868 million , which seemed generous for a company that most people outside San Juan had never heard of. Three years later, Apollo took it public. By the time of the IPO, Apollo was sitting on a fivefold return on its $184 million investment having already extracted $160 million in dividends on top of it. That’s one of the cleanest private equity home runs of the last 20 years, executed entirely in a market Wall Street still ignores. The company was Evertec. And Wall Street still hasn’t figured out what Apollo figured out in 2010.

Here’s what’s happening right now: Evertec just reported Q4 2025 revenue of $244.8 million, up 13.1% year-over-year record numbers, clean beat, guidance above consensus and the stock has fallen 25% from its 52-week high anyway. The market is collectively worried about three things: single-client concentration risk from Banco Popular, leverage from an aggressive Brazil acquisition campaign, and the supposed threat of Pix (Brazil’s government payment system) eating Evertec’s lunch. Each of these concerns contains a kernel of truth wrapped in a thick layer of misunderstanding. The result is a fintech company growing at 10%+ annually trading at 13x earnings a valuation usually reserved for structurally declining businesses, not expanding ones.

Why analyze this now? Because the gap between what Evertec is actually building and what the stock price implies has rarely been this wide, and the Brazil chapter of this story is still in the first few pages.

1. The Machine

The Simple Explanation

Picture a small island economy where almost every financial transaction every debit card swipe, every ATM withdrawal, every government benefit payment, every merchant terminal tap flows through a single company’s pipes. That company collects a tiny fee on each one. The island has 3.2 million people and processes billions of transactions annually. Nobody can build a competing network because the incumbent has been there for 35 years, owns the infrastructure, has regulatory relationships with every bank on the island, and processes payments for the US Federal Reserve itself.

Now imagine that same company is quietly doing the same thing across 25 other countries in Latin America and the Caribbean and has just started buying the picks-and-shovels infrastructure companies that every Brazilian bank needs to function in the digital age.

That’s Evertec. It processes approximately 10 billion transactions annually across a network serving financial institutions, merchants, corporations, and government agencies. It doesn’t lend money, doesn’t hold deposits, doesn’t take credit risk. It just runs the pipes and collects the toll.

The Moat: Three Layers Most Analysts Only Count as One

The standard analyst write-up on Evertec describes its moat as “first-mover advantage in Puerto Rico.” That’s like describing Visa’s moat as “people use their cards a lot.” It’s true but misses the structural depth entirely. The moat has three distinct layers.

Layer one: Physical network monopoly. Evertec manages 80% of debit transactions and 70% of ATM transactions in Puerto Rico through the ATH network. ATH has 2,500 ATMs throughout Puerto Rico and facilitates payments in over 50,000 businesses. Building a competing network from zero would require negotiating access agreements with every bank on the island, installing competing infrastructure at thousands of merchant locations, obtaining the same regulatory certifications Evertec holds, and doing all of it while your competitor is already processing billions of transactions per year. The economics of displacing entrenched payment infrastructure don’t work which is exactly why nobody has tried in 35 years.

Layer two: Federal credentialing. Here’s the detail that doesn’t appear in any standard analyst note. Evertec manages all US government-subsidized payments in Puerto Rico SNAP, Social Security, federal benefits and is the designated processor for the Federal Reserve’s Caribbean cash operations. The Federal Reserve does not give this mandate to companies with weak infrastructure, operational risk, or uncertain regulatory standing. It’s a credential that functions as a permanent competitive moat, because no new entrant can realistically replicate the years of compliance documentation, audit history, and institutional trust that goes into earning it.

Layer three: The Hurricane Maria proof. This one is never discussed in equity research but it’s the most powerful evidence of Evertec’s infrastructure quality. When Hurricane Maria made landfall in Puerto Rico in September 2017 at Category 4 strength, it destroyed 100% of the island’s power grid, leaving every customer without electricity sometimes for nearly a year. Nearly every aspect of Puerto Rican commerce shut down. And yet, Evertec’s processing infrastructure demonstrated robust resilience, enabling rapid recovery during the large-scale outage, with ATH maintaining critical payment functionality even as the rest of the island’s infrastructure collapsed. When the worst natural disaster in Puerto Rico’s modern history couldn’t meaningfully disrupt your operations, you have built something genuinely durable. That’s not marketing that’s engineering.

The ATH Móvil sleeper: ATH Móvil Evertec’s peer-to-peer payment app — now has over 2 million users who can transfer money instantly using only a phone number. On an island of 3.2 million people, that’s extraordinary penetration. For context, getting Venmo to that kind of market share in the US took years and required billions of PayPal’s capital. Evertec built Puerto Rico’s Venmo as an extension of its existing network, essentially for free, and it now processes around 200 million transactions annually. This asset barely appears on anyone’s valuation model.

The ROIC Story: Two Businesses, One Price Tag

ROIC has declined from 27.68% in 2022 to roughly 10.33% in 2024 and at first glance that looks like a deteriorating business. It isn’t. It’s the signature of a company spending aggressively on future growth while the legacy business keeps compounding quietly in the background. The Puerto Rico and Caribbean segment still generates ROIC well north of 20% structurally high because the infrastructure is already built, the contracts are long-term, and incremental revenue requires almost no incremental capital. The ROIC compression is 100% attributable to Brazil, where Evertec has deployed several hundred million dollars across four acquisitions in three years PaySmart, Sinqia, Tecnobank, and Dimensa none of which have had time to fully contribute their earnings potential to the denominator.

The right framework is to think of Evertec as two companies bundled into one stock price: a mature Caribbean toll-road business at 20%+ ROIC, and an early-stage Brazilian fintech infrastructure play currently in investment mode. The market is pricing the combined entity as if the Brazil investment is worthless. That’s the opportunity.

The Hidden Tax Advantage Nobody Talks About

Here’s the insight that essentially never appears in retail coverage of Evertec. Puerto Rico’s Act 60 tax incentive framework allows eligible businesses to pay a corporate tax rate of only 4% compared to the US federal rate of 21% along with a 100% tax exemption on dividend distributions and 90% exemption on property taxes. Because Evertec is headquartered in San Juan and its core business qualifies under this framework, it operates with a structurally lower effective tax rate than virtually any mainland US fintech competitor. This tax shield doesn’t show up in revenue growth. It shows up silently in net margins and free cash flow conversion making Evertec’s earnings quality better than a simple margin comparison to US peers would suggest. When you’re comparing Evertec at 13x P/E to a US payment processor at 18x P/E, you’re comparing post-tax earnings on very different tax bases. Evertec’s 13x is even cheaper than it looks.

The Risks

Banco Popular concentration, honestly assessed: Popular remains Evertec’s largest client by a significant margin, and any strategic shift there a merger, internalization, aggressive renegotiation would be material. The contract runs through 2028. The honest risk mitigation is this: Popular has renewed and extended this relationship continuously for 35 years. The switching cost is enormous we’re talking months of parallel testing, regulatory filings, and operational risk during migration. And crucially, Popular still owns a meaningful equity stake in Evertec, which makes it structurally incentivized to keep the relationship healthy. A company doesn’t blow up the value of its own equity stake to win a processing cost negotiation.

Pix and the Brazil misread: Evertec faces competitive pressure from StoneCo and PagSeguro in Brazil’s consumer payments layer, and Pix adoption is driving down transaction fees in that segment. But Evertec’s Brazilian strategy is deliberately positioned one layer above the consumer payments war. Sinqia, Tecnobank, and Dimensa are B2B software companies selling core banking systems, fund administration platforms, and risk management tools to financial institutions not competing with Pix for consumer wallets. The companies that fear Pix are the ones processing consumer payments. Evertec is selling the software that banks use to manage their operations in a Pix-enabled world. That’s a subtle but crucial distinction that the market has consistently failed to make.

Leverage: With debt-to-equity at roughly 1.96x and interest coverage at 2.2x, there isn’t a lot of cushion. A bad year in Brazil integration delays, FX headwinds, client churn could create real pressure. This is the legitimate risk. It’s why the stock trades where it does. It’s also why the upside is as large as it is.

2. The Numbers

Current Valuation

Price: ~$29 | Market Cap: ~$1.85B | Enterprise Value: ~$2.8B

Profitability Snapshot

Revenue (FY2025): $931.8M (+10% YoY, +11.4% constant currency)

Net Income (TTM): ~$141.6M | EBITDA Margin: ~40%

Free Cash Flow (2025): ~$171.6M growing as Brazil integration matures

Latin America segment now approaching 40%+ of total revenue, up from ~30% in 2023

Valuation Metrics

P/E (TTM): ~13x | 5-Year Avg P/E: ~20.5x | 10-Year Avg P/E: ~20.3x

38% below 10-year historical average the deepest sustained discount since the 2022 trough

Earnings Yield: ~7.7% vs 10Y Treasury at ~4.18% → 3.5 percentage point premium for a 10%-growth fintech

vs S&P 500 Earnings Yield ~3.5% → Evertec offers more than double the yield of the broad market

Interpretation: A growing fintech, structurally protected by physical network monopoly and federal credentialing, with a hidden tax advantage, trading at more than double the earnings yield of the risk-free rate and the S&P 500. The market is pricing in significant bad news. The question is whether that bad news is coming.

Shareholder Returns

Dividend Yield: ~0.85% Quarterly: $0.05/share

Buyback Yield: ~2–3% (expanded $100M program authorized late 2024)

Total Shareholder Yield: ~3–4%

Quality Indicators

Debt/Equity: ~1.96x (elevated, manageable)

Interest Coverage: 2.2x (thin)

Piotroski F-Score: 7/9 (strong underlying financial health despite leverage concerns)

EBITDA Margin: ~40% rare for a company this size in this geography

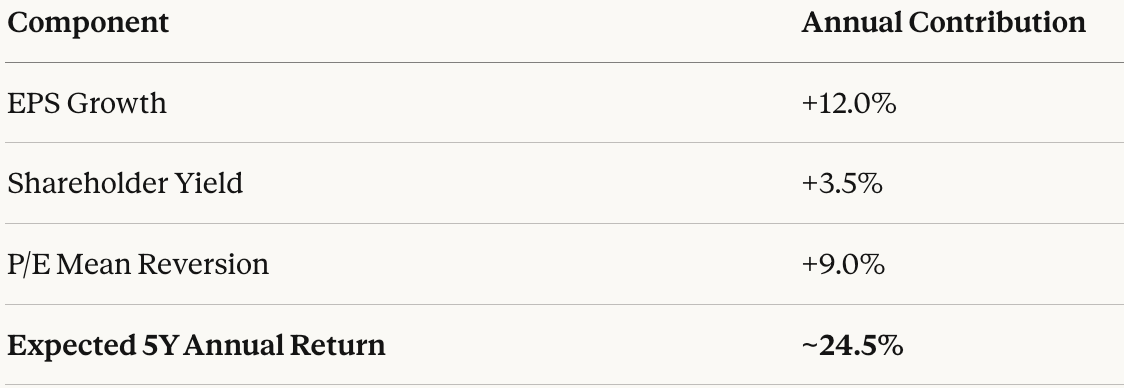

3. The Napkin Math

A. EPS Growth: ~12% annually

Revenue growing at 10–11% (guided). Brazil acquisitions fully consolidated add another leg. Share count reduction via $100M buyback program: ~2% annually.

Margin flat-to-slightly-up as integration costs normalize.

Conservative total EPS growth: ~12% per year.

B. Shareholder Yield: ~3.5%

Dividend ~0.85% + Buyback ~2.5–3% = ~3.5% total

C. Valuation Impact: +9% per year tailwind

(20/13)^(1/5) - 1 = +9.0% per year if P/E reverts to 10-year average.

Even partial reversion to 17x = +3.2% annually.

You don’t need full mean reversion to generate exceptional returns here.

D. The Final Equation

Bear case: Popular renegotiates aggressively in 2028, Brazil integration stalls, P/E stays at 13x permanently. Even then: 12% EPS growth + 3.5% yield = ~15.5% annually. That’s still 5+ percentage points above the S&P 500, on a business with 0.56 beta. The downside scenario here still beats the market. That’s rare.

4. My Proprietary Insight

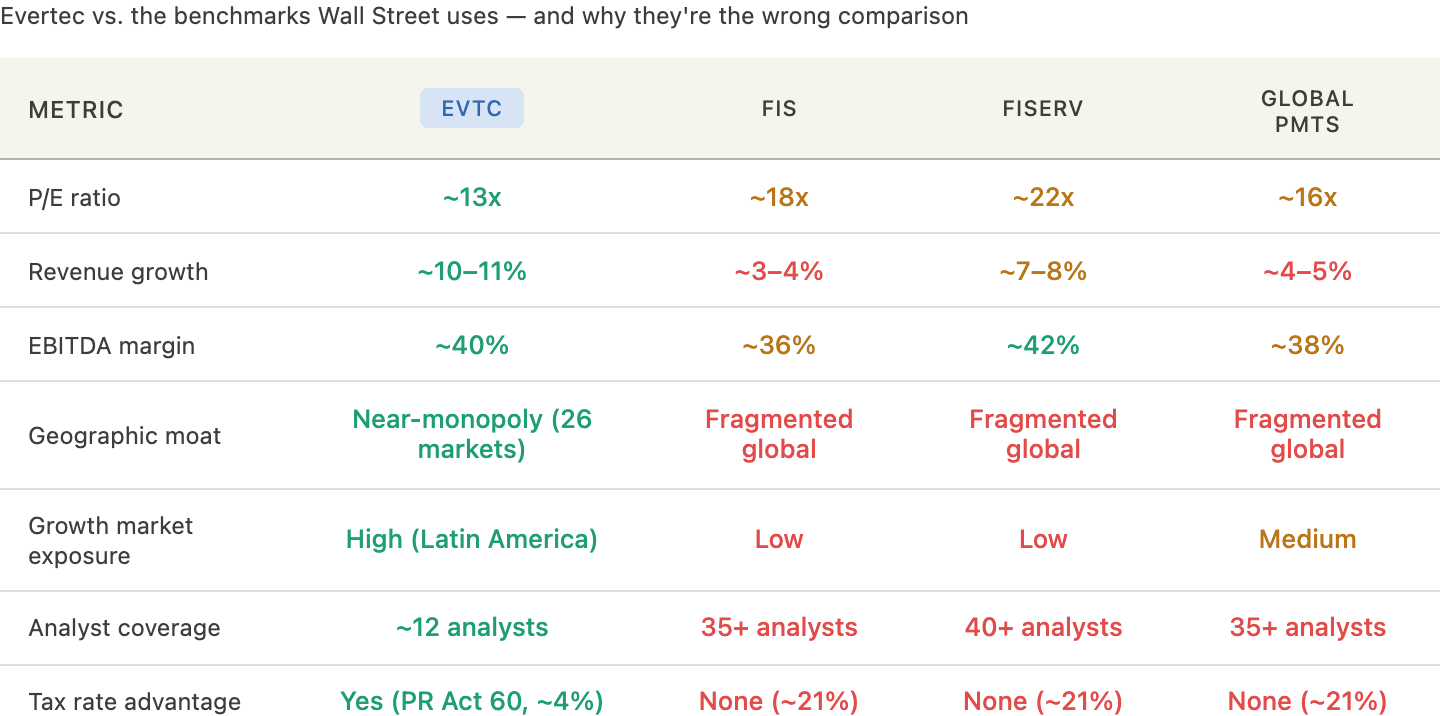

The Comparison Nobody Makes

Every analyst benchmarks Evertec against Fiserv, FIS, or Global Payments mature US processors with single-digit growth, heavy debt, and no geographic upside. That’s the wrong peer group. The right comparison is to what these businesses looked like 15–20 years ago, when they were still growing into infrastructure monopolies in underpenetrated markets. Or better yet, compare Evertec to what Nubank looked like before the market understood Brazil’s digital finance opportunity except Evertec is profitable, generates real free cash flow, and trades at a fraction of the multiple Nubank commanded at its peak.

The table is damning in the best way. Evertec grows 2–3x faster than its supposed peers, operates in markets with structurally higher growth runways, has a geographic moat that Fiserv and FIS can only dream of, benefits from a ~4% corporate tax rate versus their ~21%, and trades at the lowest P/E of the group despite being the highest-growth name. The only thing Evertec doesn’t have is analyst coverage which is precisely why the mispricing exists and precisely why retail investors who do the work have an edge here.

The P/E History: Reading the Pattern

The chart reveals a clear historical pattern. Every time EVTC has traded significantly below its 10-year average P/E of 20x, it has subsequently re-rated sharply. The 2022 trough at ~10x P/E was the most extreme example from there, the stock more than doubled within 18 months as the market remembered the business was still compounding. The current 13x isn’t quite as extreme as 2022, but the setup is structurally similar: fear-driven compression below historical norms on a business whose fundamentals are actually getting better, not worse. The market has done this before. It corrected before. The question is your patience for when.

The Brazil Optionality: The Napkin Math Nobody Is Running

Every analyst is modeling Brazil as an integration cost center a drag on margins and ROIC while Evertec digests four acquisitions. Almost nobody is modeling what Brazil looks like in 2027 when the integration is complete and the revenue is fully consolidated. Let me do it here.

Sinqia alone contributed an estimated $80–100M in annualized revenue post-close. Tecnobank and Dimensa together add another $120–150M at run rate. Total Brazil segment revenue by end-2027: conservatively $280–320M, up from essentially zero in 2022. If Brazil achieves EBITDA margins of 35% consistent with Evertec’s Caribbean business that’s ~$100M in incremental EBITDA from a segment that cost roughly $400–500M to build. A 5x EBITDA multiple on that conservative for a B2B financial software business in a 30% CAGR market implies $500M in value creation from Brazil alone. Against a current total enterprise value of $2.8B. The Brazil bet, if it works, is worth a meaningful chunk of the current entire market cap.

5. My Take

Sleep Well at Night Score: 6/10

The business quality score is 7 recurring revenue, infrastructure monopoly, federal credentialing, structural tax advantage, Hurricane Maria-proof resilience, and a Brazil expansion backed by best-in-class assets. The leverage keeps it from hitting 8. The price score at 13x earnings with three simultaneous return drivers (growth, yield, multiple expansion) is about as compelling as mid-cap fintech gets. I lose 1 points on the Popular concentration risk which is real, never goes away, and is 2028 in everyone’s calendar.

What Excites Me

The Puerto Rico business is one of the most durable infrastructure monopolies in fintech validated by Hurricane Maria, credentialed by the Federal Reserve, and structurally protected by 35 years of compounding switching costs. It’s a cash machine that requires almost no reinvestment to sustain, which frees up capital to fund the Brazil bet.

Brazil is being built the right way through the back door, at the B2B software layer, away from the Pix and Nubank competition and the assets Evertec has acquired (Sinqia built with B3 and TOTVS, Dimensa from institutional founders) have the kind of pedigree that doesn’t come cheap or often. By the time the market properly prices in a $300M+ Brazil revenue base, the stock will look very different from here.

The tax structure is a permanent, structural earnings advantage that almost nobody models correctly. A 4% corporate rate versus 21% is not a footnote it’s a meaningful, persistent boost to free cash flow conversion that makes Evertec’s 13x earnings even cheaper than the headline number suggests.

What Worries Me

The Banco Popular clock is ticking toward 2028. Renegotiation dynamics are unpredictable, and the mere uncertainty around the outcome will create stock volatility as the date approaches, even if the relationship renews on reasonable terms.

Four simultaneous integrations in Brazil different tech stacks, different cultures, different client bases is genuinely difficult. Evertec’s management team has never attempted anything at this operational scale. Execution risk is real and underappreciated.

Brazilian Real exposure cuts two ways. A strong USD environment compresses reported revenue from Brazil precisely when Evertec needs those numbers to prove the thesis to a skeptical market.